In my earlier blog, we explored the effect of size on active large-cap equity funds’ performance. We ranked all long-only active large-cap equity funds by their size at the beginning of the observation period and divided them into quartiles, with the first quartile being the largest and the fourth being the smallest. We found that, in general, the largest ones tended to lead by returns, volatilities, survival rates, and the ability to outperform the benchmark.

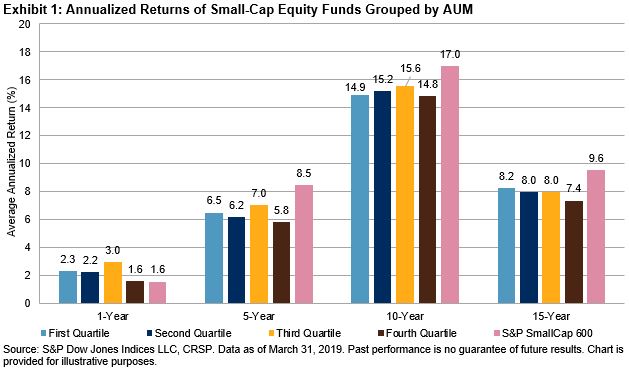

In this blog, we performed a similar analysis of the small-cap funds. Our study shows the diminished advantage of larger funds in this space. Small-cap funds of all quartiles underperformed the S&P SmallCap 600® across mid- and long-term investment horizons.

During the test period ending in March 2019, the S&P SmallCap 600 lagged three out of four quartiles of small-cap funds over the past year, but outperformed all quartiles across the mid- and long-term investment horizons (see Exhibit 1). Unlike the large-cap funds, the largest small-cap funds did not always generate higher annualized returns than their peers. In the past 15 years, annualized returns in the first, second, and third quartiles were quite similar.

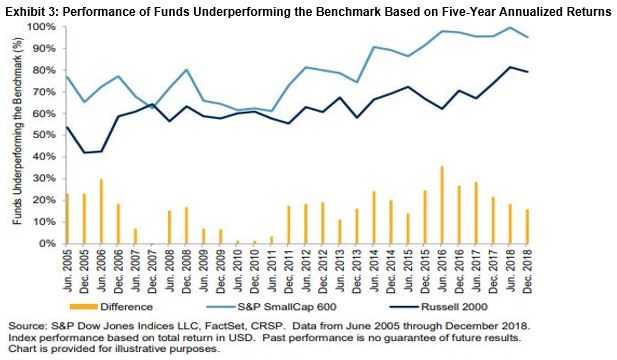

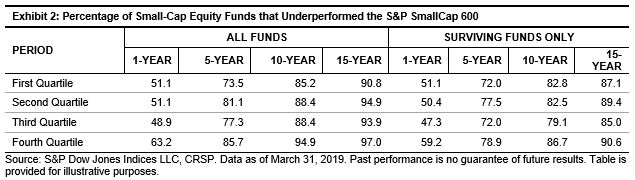

Not surprisingly, the majority of small-cap funds in all quartiles underperformed the S&P SmallCap 600 over the mid- to long-term investment horizons. If we assume that all “dead” funds underperformed the benchmark, then more than 90% of each group underperformed the benchmark over the past 15 years, and the largest funds had the lowest underperformance percentage among the four groups. However, if we account only for funds that survived the testing periods, then the third quartile funds had the lowest percentage of underperformance compared with the S&P SmallCap 600 (see Exhibit 2).

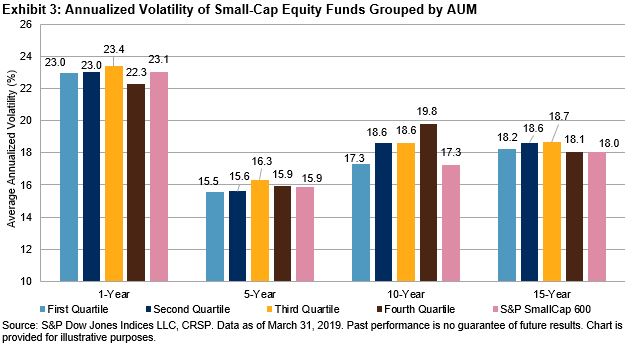

Furthermore, the S&P SmallCap 600 generated similar or lower volatilities compared with active small-cap funds over all time periods analyzed (see Exhibit 3).

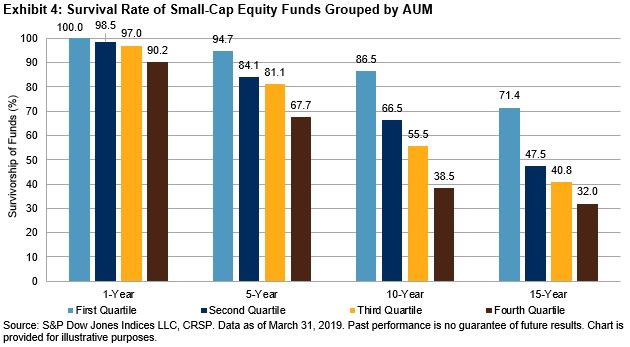

Interestingly, our analyses show that the larger funds had a significantly higher survival rate than their smaller peers, especially over longer horizons (see Exhibit 4). Only 41% of the third quartile funds that existed at the beginning of the 15-year study period survived the entire period, compared with a survival rate of 71% for the larger funds over the same period.

Our study shows that the relatively simple and transparent S&P SmallCap 600, a beta exposure to the U.S. small-cap space, outperformed the majority of small-cap funds (on a return and risk-adjusted basis), regardless of AUM over the long term.

The posts on this blog are opinions, not advice. Please read our Disclaimers.