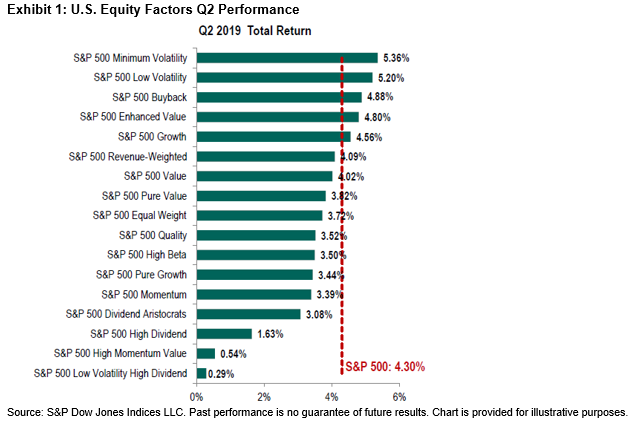

The performance of U.S. equity factors during Q2 was lackluster, with most underperforming the S&P 500, as seen in Exhibit 1. While Minimum Volatility and Low Volatility were notable exceptions, Value, Quality, High Beta, and Momentum all lagged the benchmark – in large part because of their tilt toward smaller companies. Since most factor indices are not cap-weighted, their out- or under-performance tends to parallel that of the equal-weighted 500.

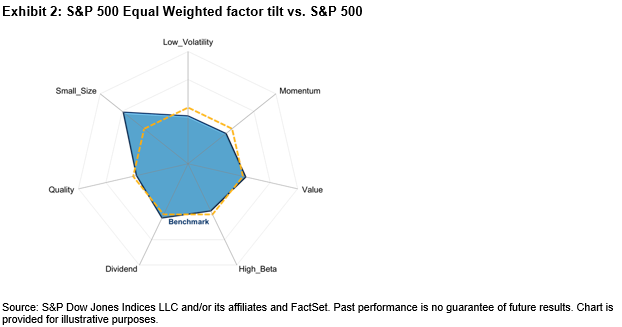

Equal Weight is a particularly good illustration of the small-size effect, since it holds the same stocks as the cap-weighted S&P 500. Exhibit 2’s factor exposure chart makes Equal Weight’s small cap tilt clear. Given the outperformance of larger-cap stocks during the quarter, Equal Weight performance was understandably disadvantaged.

Equal Weight is a particularly good illustration of the small-size effect, since it holds the same stocks as the cap-weighted S&P 500. Exhibit 2’s factor exposure chart makes Equal Weight’s small cap tilt clear. Given the outperformance of larger-cap stocks during the quarter, Equal Weight performance was understandably disadvantaged.

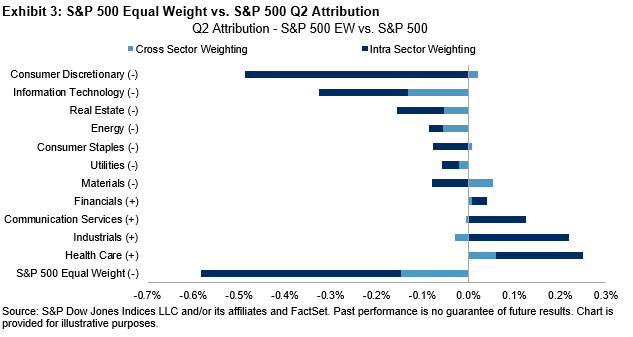

Exhibit 3 demonstrates that larger-cap stocks dominated within most sectors of the S&P 500, with a particularly noticeable effect in the Consumer Discretionary and Info Tech sectors. Seven out of eleven equal weight sectors underperformed their cap-weighted counterparts.

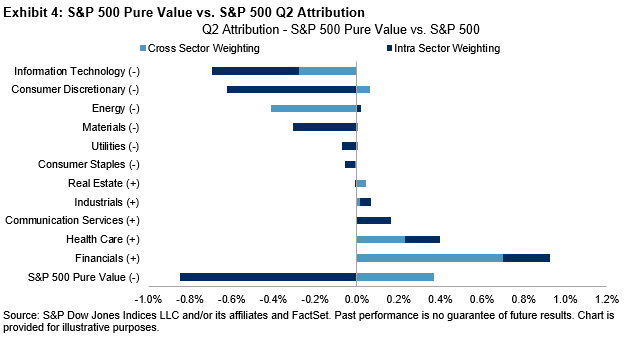

The S&P 500 Pure Value Index provides a less direct example of the impact of large-cap performance. The key driver of Pure Value’s underperformance last quarter was stock selection, again primarily in the Info Tech and Consumer Discretionary sectors.

Active managers are not immune to these effects. Our SPIVA database shows that active management tends to be particularly challenged in periods when the largest stocks outperform, and when Low Volatility outperforms. If I were a betting woman, I would not bet on active manager outperformance when our next SPIVA report appears.

The posts on this blog are opinions, not advice. Please read our Disclaimers.