S&P Dow Jones Indices produces a semi-annual report comparing the performance of active managers to their target indices or benchmarks. The report is referred to as the SPIVA Scorecard (SPIVA standing for S&P Indices Versus Active Managers). So, what does the SPIVA Scorecard tell us about performance? As illustrated in the table above, for any regional equity class and over any timeframe, it tells us that the overwhelming majority of Canadian active managers fail to beat their benchmarks.

This underperformance can be attributed to two main factors: 1) information efficiency and 2) high portfolio management fees. Historically, “stock pickers” were often able to beat their target indices. This was accomplished through rigorous analysis of privileged financial information and interviews with senior management. However, he advent of the Internet and new regulations with respect to selective disclosure has levelled the playing field. Today critical corporate information is readily available to all investors without privilege and at little expense. As a result, market pricing has become “efficient”. There is very little that an active manager can determine about the investment prospects for a large cap stock that the market doesn’t already know. At the same time, active managers typically charge investment management fees in the 1% range. Portfolio turnover is often 50% to 100% or more, in any given year, further raising investment costs and eating into overall portfolio returns.

The end result, as illustrated in the performance data, is that active management of large cap liquid equities is no longer effective.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

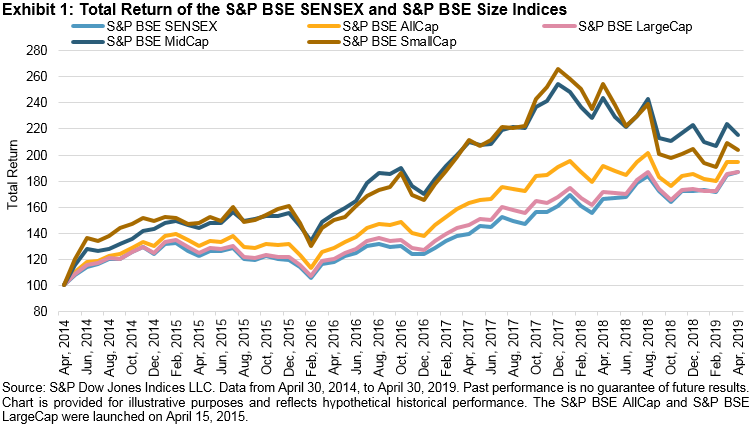

Exhibit 2 provides the five-year absolute returns of the S&P BSE AllCap Series. Among the sub-sector indices in the S&P BSE AllCap, the

Exhibit 2 provides the five-year absolute returns of the S&P BSE AllCap Series. Among the sub-sector indices in the S&P BSE AllCap, the