In general, it is a positive sign when a company buy back shares. This means the company believes its stock is undervalued and is confident about its future earnings. In recent years, buybacks have become increasingly popular. With a record number of companies buying back shares, how are these companies are faring?

A company can choose to return value to shareholders in a number of ways: it can pay out cash dividends, reinvest in the business, buyback shares, or a combination of these.[1] Traditionally, paying out dividends has been the dominant method to return a company’s excess cash to investors, and dividend income returns have contributed to over one-third of the monthly total return of the S&P 500 from 1928 to 2016.[2] In a share repurchase, a company reduces its shares outstanding through an open-market buyback or tender offer.

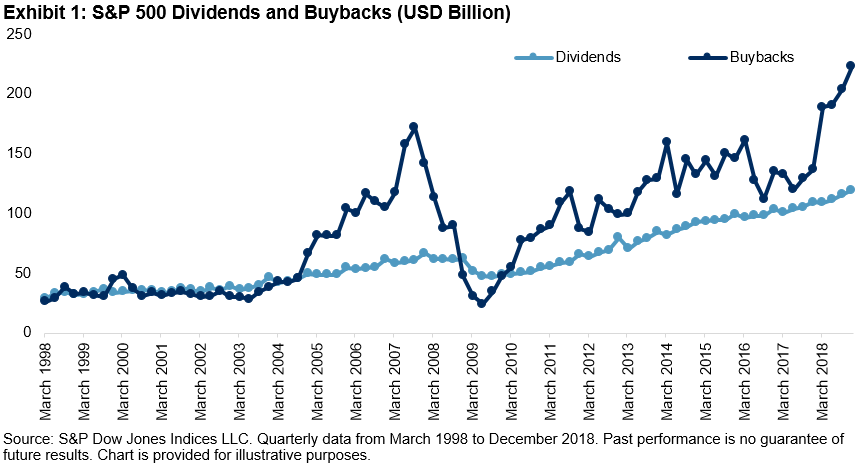

Exhibit 1 charts the aggregate amount of dividends and repurchases of S&P 500 companies since 1998. While cash dividends show a steady increase over time, the amount of shares repurchased has been volatile. The amount of buybacks jumped significantly right before the 2008 global financial crisis and dropped drastically in 2009. Since 2010, the amount of buybacks has continuously grown and exceeded the amount of dividend distributions.

The buyback momentum has continued into 2019, even after a record USD 806 billion[3] buyback in 2018, a 56% increase from the previous year. As shown in Exhibit 2, two decades ago, fewer than half of S&P 500 companies purchased shares back. The participation rate stood at around 80% as of Dec. 31, 2018.

Since its inception in January 1994, the S&P 500 Buyback Index returned 13.29% annually, compared with gains of 10.31% and 8.96% from the S&P 500 High Dividend Index and S&P 500, respectively. One of the key reasons for the outperformance is that buying shares back decreases the company’s shares outstanding, which helps improve earnings-per-share (EPS) and eventually propels stock prices higher.

[1] Zeng, “Examining Share Repurchasing and the S&P Buyback Indices in the U.S. Market” (April 2016)

[2] Li and Soe, “Incorporating Free Cash Flow Yield in Dividend Analysis” (November 2017)

[3] “S&P 500 Q4 2018 Buybacks Set 4th Consecutive Quarterly Record at $223 Billion,” S&P Dow Jones Indices

The posts on this blog are opinions, not advice. Please read our Disclaimers.