2018 produced negative absolute returns across a number of asset classes, particularly international stocks. A broad benchmark of stocks traded outside of the U.S., the S&P Global ex-U.S. BMI (US Dollar) Gross Total Return Index, lost 14.18% of its value. Nevertheless, many investments kept pace with the change in cost of securing future retirement income, because an upward shift of real rates decreased the present value of future inflation-adjusted cash flows. For instance, the constant maturity 10-Year Treasury Inflation-Indexed Security Rate,[1] published by the St. Louis Fed, almost doubled from 0.54% in January 2017 to 1.02% on Dec. 1, 2018.

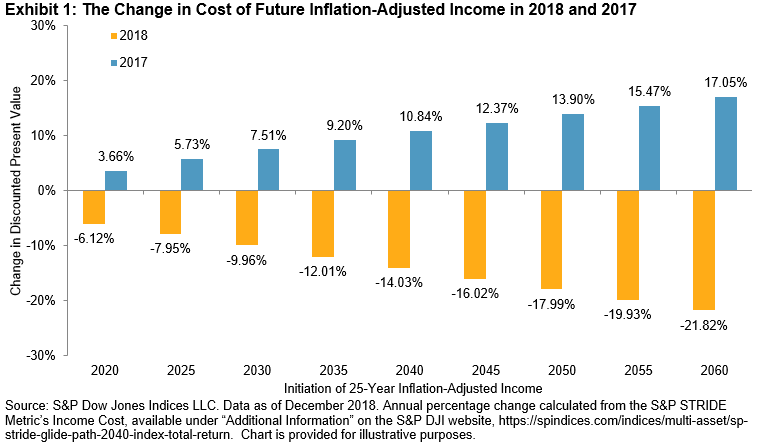

Exhibit 1 shows the change in present value, for 2017 and 2018, of 25-year inflation-adjusted cash flows that begin paying in the respective future years on the chart’s horizontal axis. For example, savers planning to retire around 2030 saw the cost of providing themselves 25 years of inflation-adjusted income decrease by 9.96% in 2018 after an increase of 7.51% in 2017.

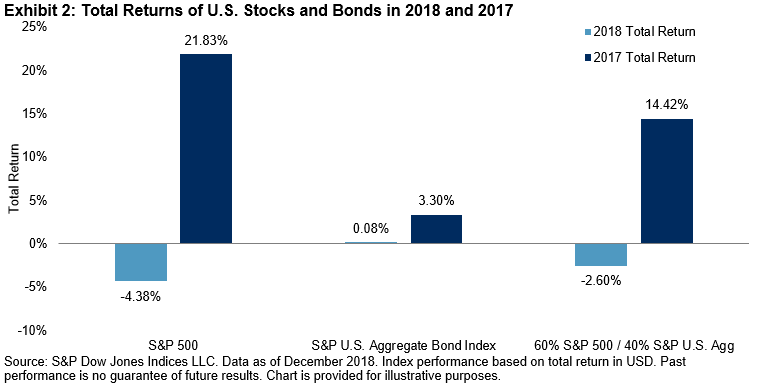

Exhibit 2 shows the total returns of U.S. stocks and bonds, as measured by the S&P 500® and the S&P U.S. Aggregate Bond Index, as well as a hypothetical 60/40 mix of the two, for 2017 and 2018.

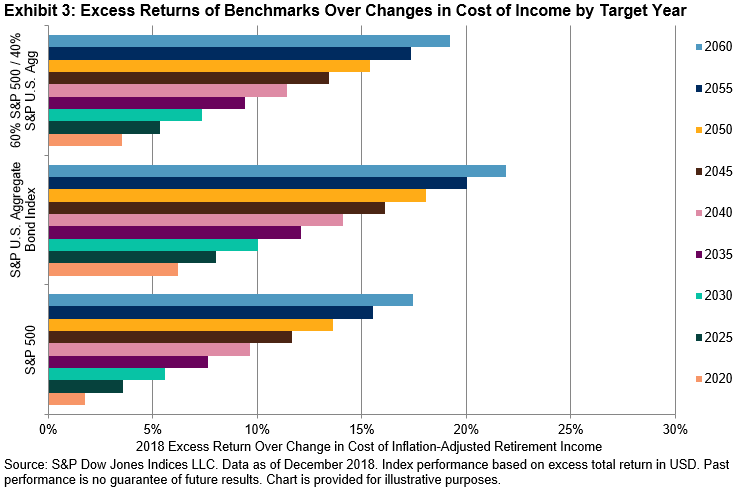

Exhibit 3 displays excess total returns of the benchmarks from Exhibit 2 over the decrease in the cost of income for each respective year (from 2020 to 2060). Despite negative and near-zero absolute returns for U.S. stocks and bonds, respectively, both outpaced the change in cost of future income for all of the target years, as did the 60/40 stocks/bonds mix.

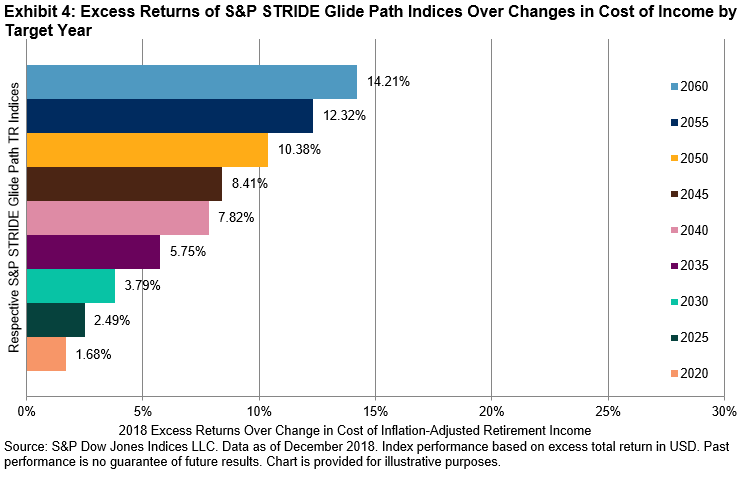

Finally, Exhibit 4 shows excess returns of specific S&P STRIDE Indices over the decrease in cost of future income for the same target years.

The S&P STRIDE Indices also outpaced the decrease in cost of future income for all target years from 2020 to 2060. The magnitude of their excess returns over the decrease of income cost was generally not as strong as it was for U.S. stocks and bonds. However, these indices are designed to adjust to changes of income cost more reliably than stocks or bonds. One of the characteristics of the S&P STRIDE Index Series methodology[2] is that the index weight of near-dated S&P STRIDE Indices is heavily allocated to a mix of U.S. Treasury Inflation-Protected Securities matching the duration of retirement income for the respective target year.

If income risk is not managed, the question of whether investment returns will keep pace with changes in income cost is unpredictable, because the relationship between the value of assets and the value of a retirement income liability is essentially random. 2018 provided an example of negative absolute returns outpacing a decrease in the cost of income, so investors saving for retirement may not be as bad off as they feel when they open their year-end 401(k) statements. It may not be immediately apparent, but in income terms, the 2018 scenario is better than a situation wherein positive absolute returns fail to keep pace with increases of income cost. In such a scenario, investors may feel wealthier without considering that their wealth buys less income. Of course, the most detrimental scenario is when negative absolute returns combine with rising income cost, in which case one loses ground in terms of both wealth and income, which may be the strongest argument for managing income risk as retirement draws closer.

[1] See https://fred.stlouisfed.org/series/FII10.

[2] https://spindices.com/documents/methodologies/methodology-sp-stride-index-series.pdf

The posts on this blog are opinions, not advice. Please read our Disclaimers.