“Change is the only constant,” as quoted by Heraclitus, a Greek philosopher.

The recent assembly election results have reiterated this. We saw a leadership change at the Reserve Bank of India (RBI), with Mr. Shaktikanta Das’s appointment as the new RBI Governor, following Mr. Urjit Patel’s resignation.

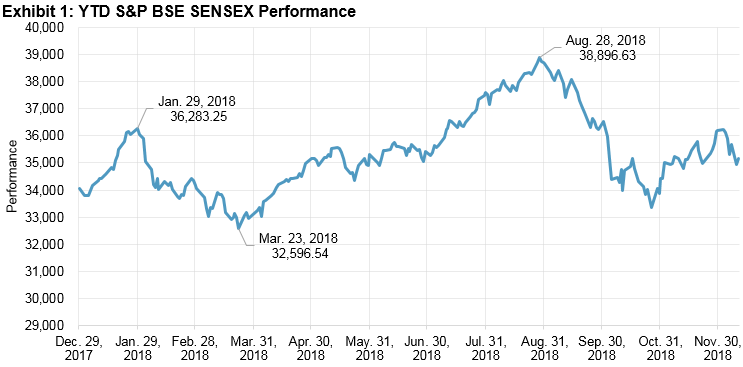

The financial markets have also had their fair share of ups and downs. In 2018, India’s equity market witnessed a low when the S&P BSE SENSEX dropped to 32,596 (price return index level as of March 23, 2018), but also saw a high of 38,896 (price return index level as of Aug. 28, 2018)—a fluctuation of 6,300 points and a 19% variation over the year. However, this year the index reached record highs compared with the past 10 years. The S&P BSE SENSEX first crossed the 10,000 mark on Dec. 18, 2008, the 20,000 mark on Sept. 21, 2010, and finally the 30,000 mark on April 26, 2017. The fixed income market was no exception, with the 10-year Government Bond yields crossing 8% multiple times in September and October 2018. There has a been an ongoing discussion on the broadening of the Indian debt market, which faces challenges in terms of liquidity, innovation, investor awareness, and participation.

Other changes introduced by the Securities and Exchange Board of India (SEBI) were style and size definitions for mutual funds, as well as consolidation of mutual fund schemes to a single offering in each style category in order to create a standardization for the market and its investors. SEBI also advised mutual funds to adopt total return indices (TRI) to benchmark their schemes, effective as of Feb. 1, 2018. This would enable investors to compare the appropriate index with the scheme’s performance.

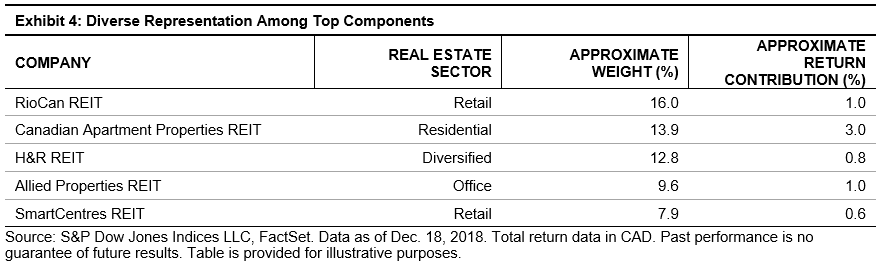

With the constantly shifting investment landscape, some changes have been significant. The endless discussion around the active vs. passive debate has also progressed. More and more market participants have aligned with the fact that a passive investment strategy can be part of the overall investment goal achievement. A core satellite strategy easily encompasses both active and passive styles. The SPIVA® India Mid-Year 2018 results revealed how large-cap funds in India have been under performing the benchmark, the S&P BSE 100. The index outperformed the fund category by over 87% in the 1-year period, 78% in the 3-year period, 48% in the 5-year period, and 62% in the 10-year period. Active fund managers have been waking up to the fact that large-cap passive investing is a strategy potentially worth evaluating.

| Exhibit 2: Percentage of Funds Outperformed by the Index | |||||

| FUND CATEGORY | COMPARISON INDEX | 1-YEAR (%) | 3-YEAR (%) | 5-YEAR (%) | 10-YEAR (%) |

| Indian Equity Large-Cap | S&P BSE 100 | 87.88 | 78.35 | 48.08 | 62.77 |

| Indian Equity-Linked Savings Scheme | S&P BSE 200 | 83.72 | 61.54 | 27.78 | 43.33 |

| Indian Equity Mid-/Small-Cap | S&P BSE 400 MidSmallCap Index | 62.22 | 78.26 | 53.03 | 50.67 |

| Indian Government Bond | S&P BSE India Government Bond Index | 82.93 | 75.47 | 82.35 | 94.92 |

| Indian Composite Bond | S&P BSE India Bond Index | 30.00 | 60.42 | 68.70 | 95.45 |

Source: S&P Dow Jones Indices LLC, Morningstar, and Association of Mutual Funds in India. Data as of June 30, 2018. Past performance is no guarantee of future results. Table is provided for illustrative purposes and reflects hypothetical historical performance. The S&P BSE 400 MidSmallCap Index was launched on Nov. 30, 2017. The S&P BSE India Government Bond Index was launched on Dec. 31, 2013. The S&P BSE India Bond Index was launched on March 12, 2014. .

Furthermore, government bodies like the Employee Provident Fund Organization (EPFO) and the Department of Investment and Public Asset Management (DIPAM) have supported the passive style of investing with the promotion of exchange-traded funds (ETFs). EPFO’s allocation to equity ETFs stood at 15% of its investible surplus, which is over INR 40,000 crores as of September 2018. Furthermore, the EPFO has been developing software that will allow them to credit the ETFs to subscriber accounts, thereby empowering subscribers for further transaction. DIPAM, on the other hand, used the ETF vehicle successively to liquidate holdings in public sector undertakings. In 2018, they had follow on offers for the ETFs, the S&P BSE BHARAT 22 ETF and the CPSE ETF, both of which were oversubscribed. Their new initiative for a debt ETF could be a strong innovation to promote passive style of investing in the fixed income space.

Passive investing is now getting more emphasis, and as index-based investing offers diversification, transparency, and liquidity, there are positive signals that with growing investor education and awareness, India could witness more growth in the days to come.

References:

- Categorization and Rationalization of Mutual Fund Schemes, SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2017/114, Oct. 6, 2017.

- Benchmarking of Scheme’s performance to Total Return Index, SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2018/04, Jan. 4, 2018.

- September 30 Economic times Wealth