Factor investing is growing rapidly — not only are more investors adopting factor strategies, but as investors gain experience, they increase their use of them. This is one of the key findings from our recent Global Factor Investing Study, which is based on face-to-face interviews and discussions with more than 300 institutional and wholesale factor investors around the world — including financial advisors, pension funds, private banks and insurance companies.

Investors are adopting more factor strategies, but still in small doses

Factors are measurable characteristics of a security that help explain its performance. Our study found that while an asset owner often commences their factor journey with a single strategy, it is uncommon for them to stop there. The institutional and wholesale investors surveyed in the study have gone on to implement from two to four factor strategies on average.

However, factor allocations generally represent a small proportion of the asset classes they are being applied to. In the vast majority of cases (looking at equities and fixed income), allocations to factor strategies remain in the 0% to 20% range. This means that even for factor adopters, most still have over 80% of their equity and fixed income allocations in traditional active and/or market-cap-weighted passive strategies.

For those institutional investors who described themselves as “sophisticated” factor users, this segment reported nearly double the average allocation to factor strategies than the less sophisticated segment, at nearly 20%. This trend also applies to wholesale investors, where the more sophisticated users reported average factor allocations of 15%.

Which factor is the most used?

Our study found that Value continues to be the most commonly utilized style factor in portfolios and is particularly ubiquitous in institutional portfolios — which is notable given the extended underperformance of equity value strategies in recent years. Other key style factors include Low Volatility, Momentum, Size and Quality.

Respondents noted that they tend to start their factor journey with equities, and look to extend into fixed income and multi-asset applications.

Single or multi-factor?

When it comes to applying a single or multi-factor approach, our study found that equity single factors are the most common approach, closely followed by equity multi-factor. Some distance behind are multi-asset approaches, followed by single- and multi-factor fixed income.

The reasons behind these choices are relatively clear and rational.

- For institutions, single factor approaches are driven by the desire to reduce or minimize complexity and to keep costs low. This is particularly relevant for newer factor investors and smaller institutions with limited internal resources.

- Institutions favoring multi-factor approaches have different motivations — control of risk, factor tilting and enhancement of performance were cited by respondents as much more important than costs. Multi-factor strategies tend to be deployed by larger investors that have significant scale and lower cost ratios.

- For wholesale investors, the drivers are very similar, with lower costs cited as an even stronger driver for single factor usage.

Learn more about how institutions and wholesale investors are using factor strategies.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

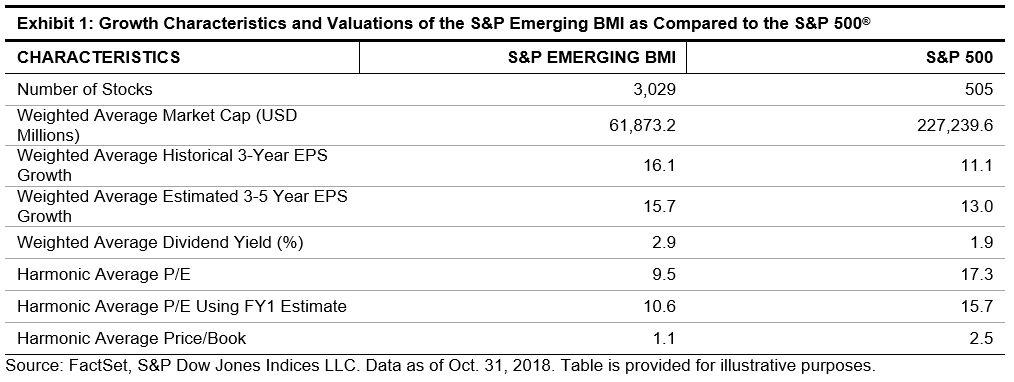

Low volatility’s success was not unique to the U.S. Exhibits 3 and 4 show that similar trends occurred globally, particularly in the emerging markets and Asia, regions that have experienced turmoil for most of this year. The

Low volatility’s success was not unique to the U.S. Exhibits 3 and 4 show that similar trends occurred globally, particularly in the emerging markets and Asia, regions that have experienced turmoil for most of this year. The