In this blog, we estimate the impact of survivorship bias on the performance of active equity funds in Brazil compared with the benchmark, the S&P Brazil BMI. We do so by replicating the outperformance report from the SPIVA® Year-End 2017 Latin America Scorecard, while removing all the liquidated and merged funds. We noted in a prior blog that as a group, liquidated and merged funds in Brazil underperformed the benchmark by a wider margin than the overall SPIVA active fund universe in Brazil. Consequently, including only surviving funds in the research universe, instead of including all funds that were active at the start of the performance measurement periods, should result in an upward bias in outperformance, which we will demonstrate in this blog.

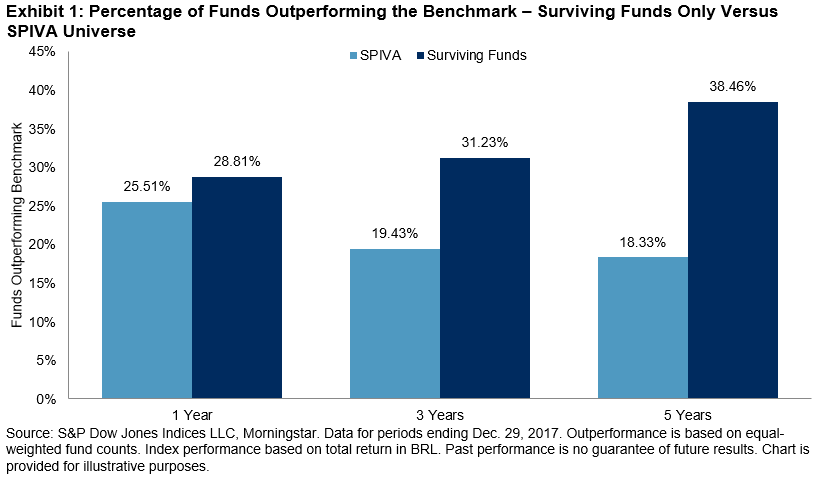

Exhibit 1 shows the percentage of funds in the Brazil Equity Funds category that outperformed the benchmark for one-, three-, and five-year periods as of year-end 2017. Two groups of funds were formed; the first group was the universe used in the SPIVA scorecard and the second group included SPIVA universe-eligible funds after removing the liquidated and merged funds.

We observed that surviving funds outperformed the entire fund universe for all three lookback periods. Additionally, the difference in outperformance figures between the two groups increased as the time horizon increased. While the percentage of funds outperforming the benchmark for the one-year period was not significantly different, for the five-year period 38% of surviving funds outperformed the benchmark, compared with just 18% for the SPIVA universe. This highlights the importance of correcting for survivorship bias, as the success of funds in the category looked materially different when only the surviving funds were included in the analysis.

The posts on this blog are opinions, not advice. Please read our Disclaimers.