Following similar studies performed by S&P Dow Jones Indices on active funds in the U.S. and Australia, we introduce the Persistence Scorecard to the Latin America region. The two aforementioned studies have demonstrated that top-performing active funds have little chance of repeating that success in subsequent years. To determine if similar conclusions can be made in Latin America, we examined active funds in Brazil, Chile, and Mexico.

The Persistence Scorecard: Latin America Year-End 2017 presented two key statistics. First, the performance persistence of top-performing active funds that remained in the top-quartile or top-half rankings over consecutive three- and five-year periods was measured. Second, transition matrices showed the movements of funds between quartiles and halves over two non-overlapping, three-year periods. The transition matrices also tracked the percentage of funds that later were merged or liquidated during the study period.

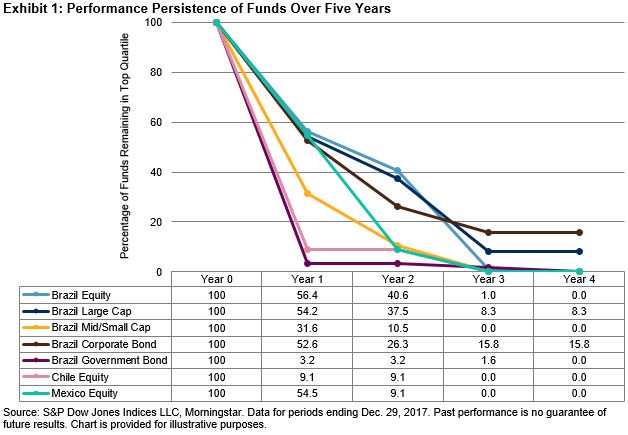

Exhibit 1 measures the performance persistence of the top quartile of funds based on performance in 2013 (Year 0). The performance of these funds was compared with the respective universe for each of the next four years to determine if they were able to sustain top performance.

Across all categories, few funds were able to maintain top-quartile status over the five-year horizon. After just one year, the most successful category was Brazil Equity, in which 56% of funds stayed in the top quartile. While this was the most successful category, it also meant that nearly half of the funds that were top performers in 2013 were unable to maintain their performance after just one year. By year three, several categories had zero remaining funds in the top quartile, and by year four, five of the seven categories had zero remaining funds. These results showed that regardless of fund category, active managers were unable to persistently produce top results.

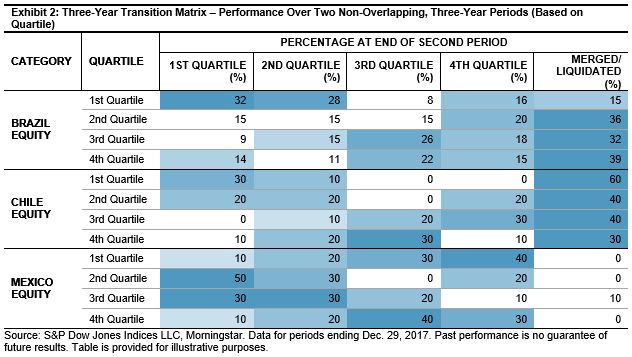

In Exhibit 2, we separated each country’s equity category into quartiles based on an initial three-year performance period (2012-2014). The performance of the subsequent three-year period (2015-2017) was then measured for each fund to obtain two non-overlapping periods of performance. Looking at these two periods, we used a transition matrix to show the movements between quartiles from the first period to the second period.

In Brazil, 60% of the funds that were in the first quartile for the first period ended up in the first or second quartile in the second period. For the second through fourth quartiles in the first period, more funds ended up merging with another fund or liquidating than sitting in one of the four quartiles (darker shades of blue signify higher frequency). In Chile, more funds shut down than resided in any of the four quartiles by the end of the second period. For the first quartile in the first period, funds that survived remained top performers in the second period, but the overall majority of funds (60%) ended up no longer being in existence. No clear trend was observed in Mexico. More funds in the top quartile in the first period transitioned to the bottom quartiles in the second period than remained in the first quartile or moved to the middle quartiles. Funds in the second and third quartiles generally moved up to the first quartile in the second period, while most funds in the fourth quartile continued to show poor performance. In essence, the results in Mexico were a coin flip.

The initial scorecard for Latin America echoed results found in the other regions—the vast majority of top performing funds were not able to deliver top performance in future years.

To see the full results, the scorecard can be found here.

The posts on this blog are opinions, not advice. Please read our Disclaimers.