As of Dec. 31, 2017, the year-over-year change in inflation for Mexico registered at 6.77%, a figure that raised concerns within the pension fund industry.

One of the key risks facing retirees is the erosion of purchasing power of investment returns due to high inflation. Developing economies, such as Mexico, are more susceptible to rising inflation levels than developed nations. In this blog, we examine if traditional retirement indices available in Mexico can provide a degree of inflation protection. With that in mind, we compare the year-over-year change in the inflation level observed in Mexico to the returns of S&P/BMV Mexico Target Risk portfolios that were constructed based on risk tolerance level.

The S&P/BMV Mexico Target Risk Index Series was launched on Nov. 1, 2016. This series comprises four multi-asset-class indices, each corresponding to a particular risk level. These indices are intended to represent stock-bond allocations across a risk spectrum from conservative to aggressive, while considering the investment constraints of local pension funds, as prescribed by the Comisión Nacional del Sistema de Ahorro para el Retiro (CONSAR), the pension system regulator in Mexico.

We used information publicly available on the Instituto Nacional de Estadística y Geografía (INEGI) website for the monthly historical series of the National Consumer Price Index (CPI)[1] from Dec. 31, 2008, which is the first value date of the S&P/BMV Mexico Target Risk Conservative Index, S&P/BMV Mexico Target Risk Moderate Index, S&P/BMV Mexico Target Risk Growth Index, and S&P/BMV Mexico Target Risk Aggressive Index.

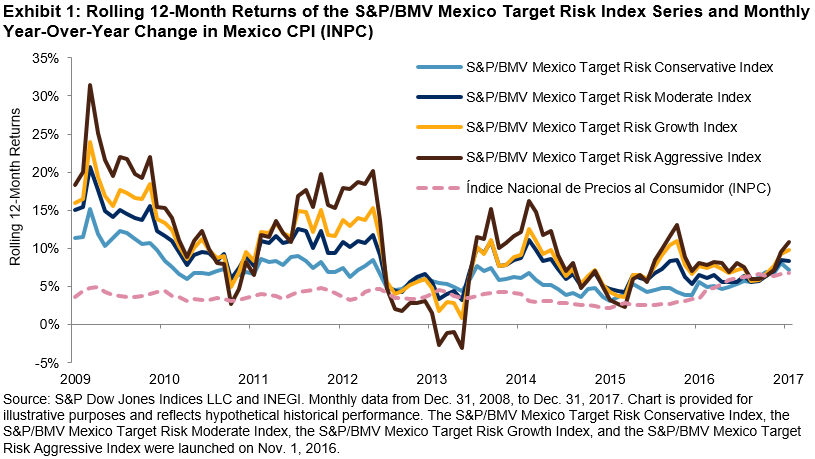

Looking at the rolling 12-month returns and monthly year-over-year change in the Mexico CPI (Índice Nacional de Precios al Consumidor—INPC) in Exhibit 1, we note that all the indices had returns higher than the inflation rate, except in 2013. In 2013, the S&P BMV Mexico Target Risk Aggressive Index, posted returns lower than the inflation rate. This is due to the fact that long-term Mexican fixed income was negatively affected by the U.S. Federal Reserve announcement that it would begin reducing its quantitative easing program. Long-term fixed income represents 62% of the total fixed income allocation in the aggressive strategy. It is worth remembering that the aggressive portfolio is oriented toward younger workers with an investment horizon of greater than or equal to 29 years.

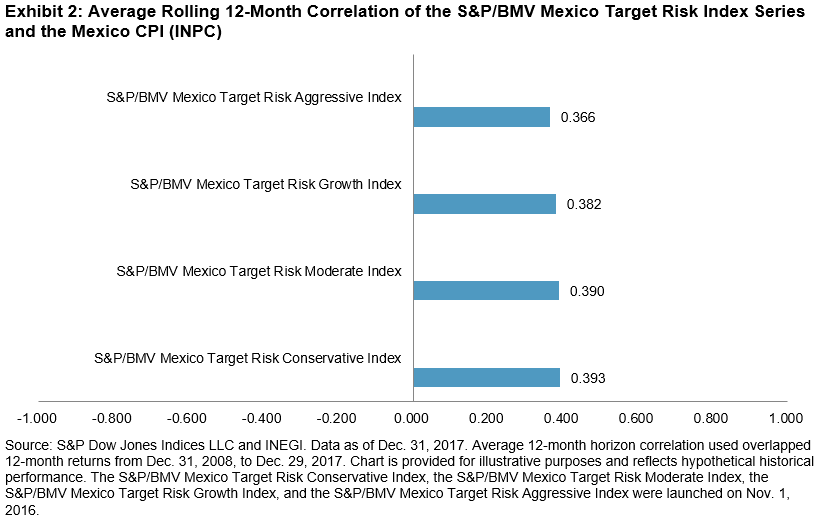

Different types of assets have different behaviors against inflation. Target risk strategies have varying degrees of allocation to inflation-linked bonds, nominal bonds, corporate bonds, and local and global equity in order to achieve specific investment outcomes. The goal of the S&P/BMV Mexico Target Risk Conservative Index is capital preservation and its 55% allocation to inflation-linked bonds is a testament to the positive correlation against inflation during the nine-year period (see Exhibit 2). The S&P/BMV Mexico Target Risk Moderate Index, S&P/BMV Mexico Target Risk Growth Index, and S&P/BMV Mexico Target Risk Aggressive Index present slightly lower correlation, implying a similar degree of inflation resistance, on average.

The S&P/BMV Mexico Target Risk Index Series is aligned with the age ranges applicable for each Sociedad de Inversión para las Afores (Siefore) by construction, as described in our paper “Benchmarking Lifecycle Investment Strategies: Introducing the S&P/BMV Mexico Target Risk Indices.” Furthermore, the index series has shown that it can potentially generate returns that are greater than inflation, thereby preserving buying power of retiree income.

[1] Instituto Nacional de Estadística y Geografía, consultation date: Jan. 9, 2018, 10:32:37. http://www.inegi.org.mx/sistemas/IndicePrecios/Cuadro.aspx?nc=CA55&T=%C3%8Dndices%20de%20Precios%20al%20Consumidor&ST=%C3%8Dndice%20Nacio

The posts on this blog are opinions, not advice. Please read our Disclaimers.