There are two major types of dividend strategies:

- Dividend growers: those targeting stocks that consistently grow their dividends over time

- High dividend yielders: those focusing on stocks that pay a high dividend yield

In our paper “A Case for Dividend Growth Strategies,” we compared dividend growth strategies to high-dividend-yielding strategies and concluded that dividend growers, which tend to be higher quality companies, have generally shown greater resilience in unsteady markets and could address concerns about dividend stocks in a rising-rate environment, to some extent.

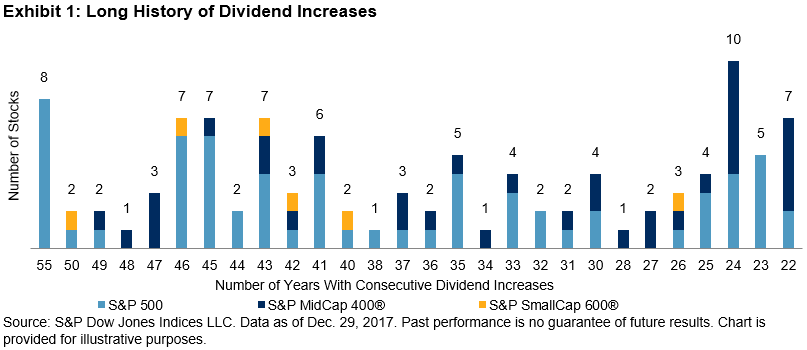

Take the dividend growth strategy built on the U.S. large-, mid-, and small-cap segments for example. The S&P High Yield Dividend Aristocrats® is designed to track a basket of stocks from the S&P Composite 1500® that have consistently increased their dividends every year for at least 20 years.

While the hurdle for index inclusion is 20 straight years of increasing dividends, the index average is 35.9 years. Additionally, there are eight constituents with over 55 consecutive years of dividend increases. This impressive consistency suggests a certain amount of financial strength and discipline, which may provide some downside protection in turbulent markets (see Exhibit 1).

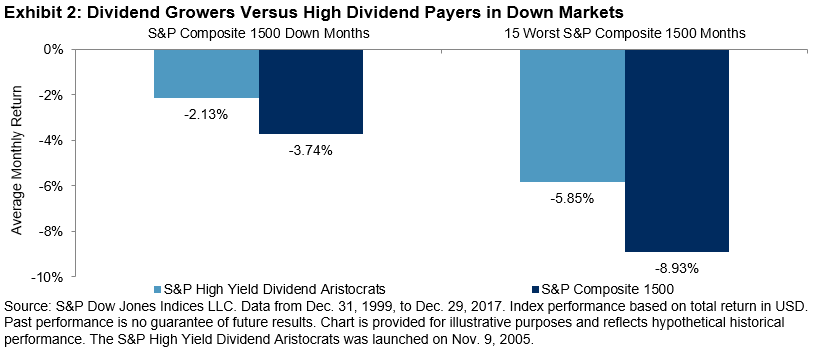

Historical performance shows that the index provided some downside protection during bearish markets. Looking at the period from Dec. 31, 1999, to Dec. 29, 2017, when the market (as represented by the S&P Composite 1500) was down, the S&P High Yield Dividend Aristocrats outperformed the S&P Composite 1500 by an average of 161 bps per month. When we focused on the 15 worst-performing months for the S&P Composite 1500 during the same period, the protection provided by the S&P High Yield Dividend Aristocrats appeared prominent. Its monthly outperformance was 308 bps against the S&P Composite 1500 (see Exhibit 2).

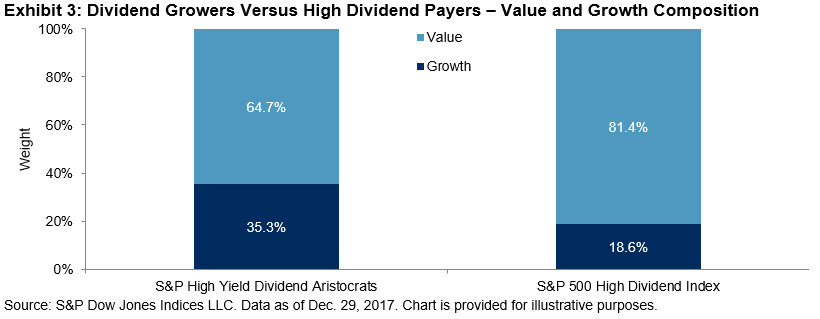

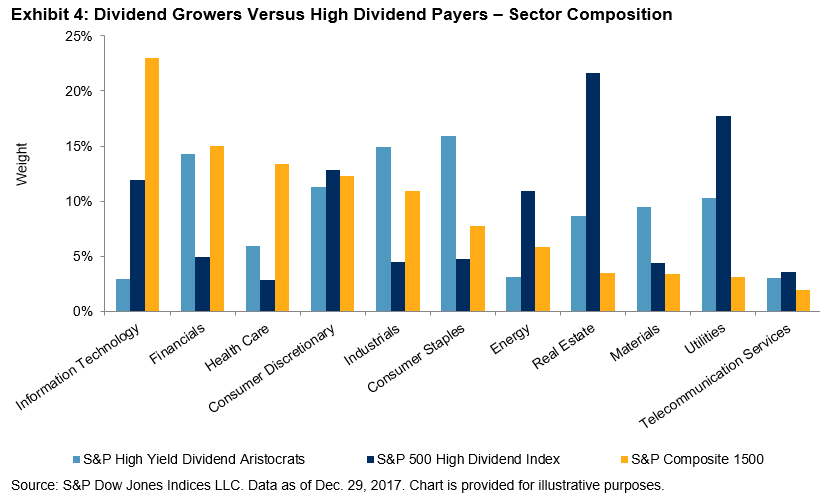

Two other important characteristics of the index are more sector diversification and less value bias compared with the high dividend yielders. As a result, as markets shift from a value to a growth regime, the performance of the dividend growers would suffer less. These characteristics could potentially address the concerns surrounding the performance of high dividend payers in a rising-rate environment. Exhibits 3 and 4 illustrate the value and growth composition as well as sector composition of the S&P High Yield Dividend Aristocrats versus the S&P 500® High Dividend Index—a high-dividend strategy built on the S&P 500.