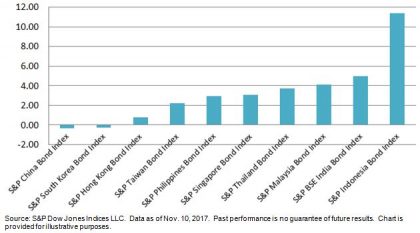

China’s lackluster performance has made it the worst-performing country in the Pan Asian bond market this year. While China has been among the top three outperforming regions in the past few years, it has significantly lagged its peers in 2017. Indonesia, as represented by the S&P Indonesia Bond Index, rose 12.6% YTD as of Nov. 10, 2017, while India (represented by the S&P BSE India Bond Index) gained 4.8% in the same period (see Exhibit 1).

The widening access that Bond Connect announced in July brought positive momentum to the market and helped recover the losses from May. However, onshore bonds are still in the negative territory compared with this time in 2016.

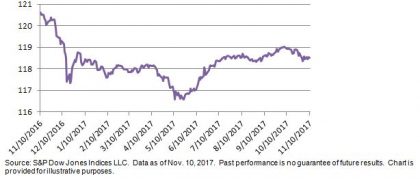

In fact, sell-offs in China onshore bonds continued to make to the headlines as the deleveraging campaign and liquidity concern lingered. As represented by the S&P China Bond Index, the one-year total return was down 1.75% (see Exhibit 2).

The S&P China Government Bond Index dropped 2.35% during the same period, underperforming the S&P China Corporate Bond Index. According to the S&P China Bond Index, government bonds represented 68% of the overall market. There are reports that market participants are switching to short-term bank debts, as they tend to offer better yields and liquidity.

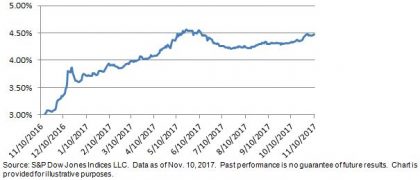

Despite its performance, China bond yield is attractive, considering its relatively short duration. As of Nov. 10, 2017, the yield-to-worst of the S&P China Bond Index was 4.5%, which widened 150 bps over the 12-month period, with a modified duration of 3.86.

Exhibit 1: Total Return of the S&P Pan Asia Bond Indices in 2017

Exhibit 2: Total Return of the S&P China Bond Index

Exhibit 3: Yield-to-Worst of the S&P China Bond Index