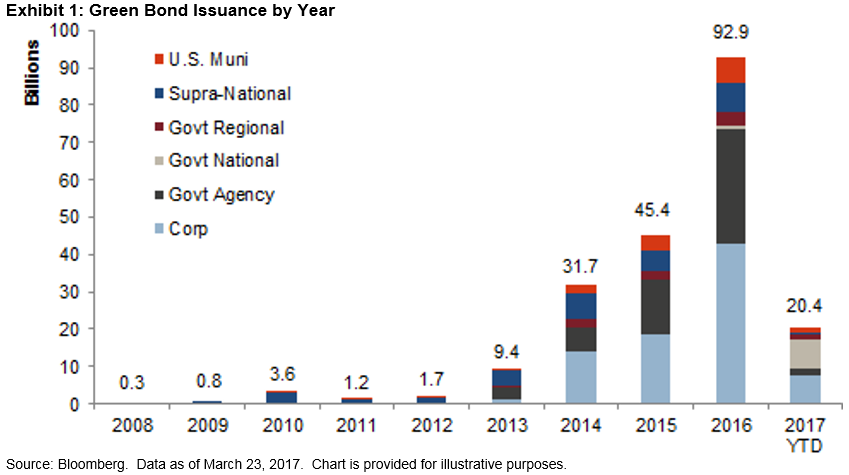

Over the recent weeks, there has been much debate about the notable increase of issuance in the fledgling green bond market. Indeed, green bond issuance ramped up significantly in 2016, and the accelerated pace is expected to continue this year. Total issuance of bonds labeled as green in 2016 amounted to USD 92.9 billion, nearly doubling the size of the green bond market from the previous year (see Exhibit 1).

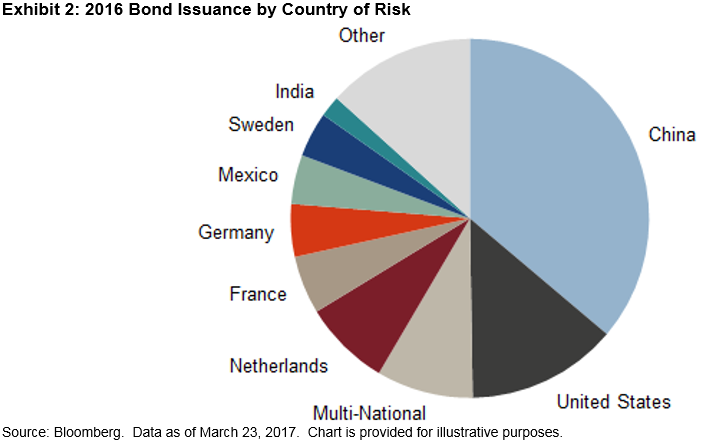

Chinese issuance accounted for the lion’s share of total issuance in 2016. In October 2015, Agricultural Bank of China was the first Chinese entity to issue green bonds. These three bonds were issued in the eurobond market, totaling about USD 1 billion. In 2016, issuance by entities domiciled (country of risk) in China grew to USD 33.6 billion, or about 36% of the total supply for that year (see Exhibit 2).

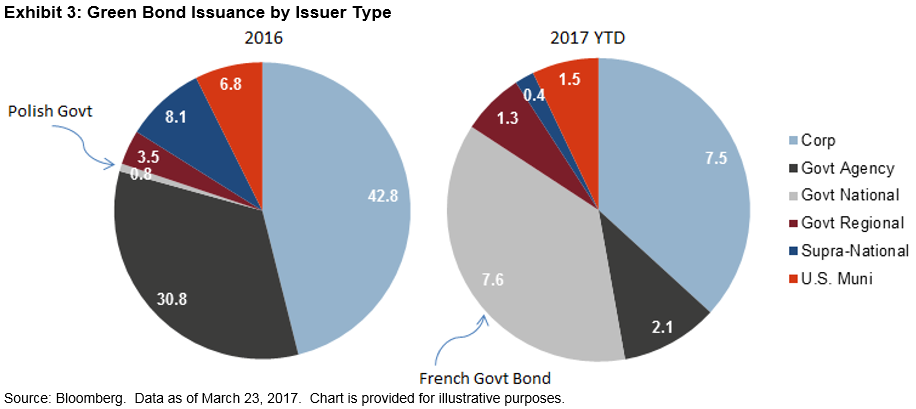

In 2016, the green bond market diversified by issuer type and country of domicile. In addition to the introduction to the market of Chinese issuance in CNY and USD, government-related authorities in Costa Rica, Finland, and Mauritius issued the first green bonds in their respective countries, and the Republic of Poland issued the first National Treasury green bond. The French National Treasury followed suit in January 2017, issuing USD 7.6 billion, the largest green bond issuance on record. The inaugural green bond from Argentina (USD) was issued just a month ago by La Rioja Province.

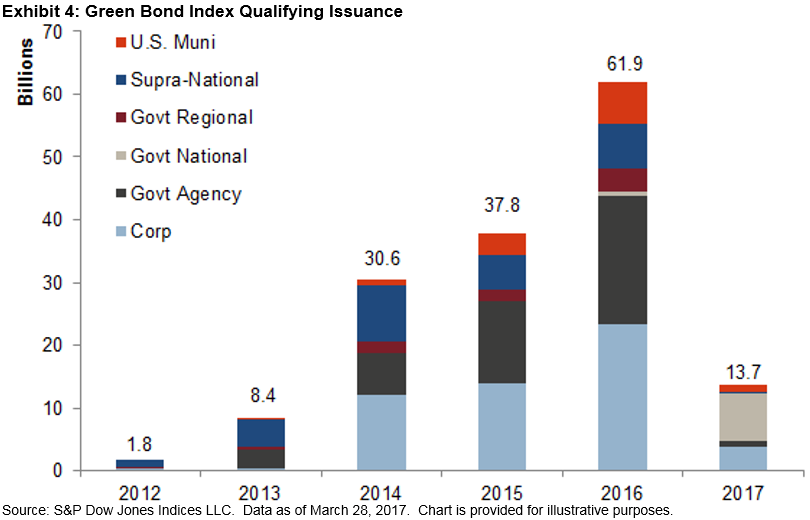

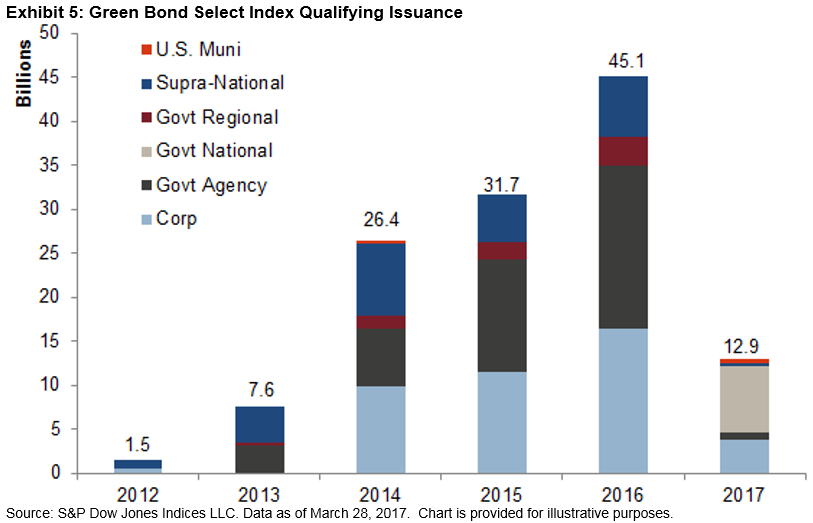

The S&P Green Bond Index is designed to track the green bond market and is composed of CBI-aligned green bonds that satisfy price availability requirements for our fixed income indices. The S&P Green Bond Index has grown in tandem with the green bond market and covers about 75% of the issuance. The S&P Green Bond Select Index is a subindex that is subject to additional selection criteria; it includes fewer than 200 of the 1,760 bonds in the S&P Green Bond Index, while covering more than 80% of the market value.

Market analysts expect issuance to continue to ramp up in 2017. Climate Bond Initiative estimates that CBI-aligned green bond issuance (a subset of all green-labeled bonds) will increase to USD 150 billion for 2017, 85% more than the USD 81 billion of CBI-aligned green bonds issued in 2016.[1]

[1] https://www.climatebonds.net/

The posts on this blog are opinions, not advice. Please read our Disclaimers.