Recently, investment professionals have paid increasing attention to the impact of carbon-intensive businesses on financial returns. Stricter regulation and increased certainty of higher carbon pricing have made this a mainstream concern. S&P Global Ratings’ announcement of a green assessment of debt finance in September 2016 is one notable example of this trend.

Water scarcity, as a risk to business, may be less well understood, but it is arguably the nearer-term threat. With a global population that has risen from 3 billion in 1960 to over 7.3 billion today, demand for fresh water is becoming greater than its practicable supply. The likely result will be increasing costs.

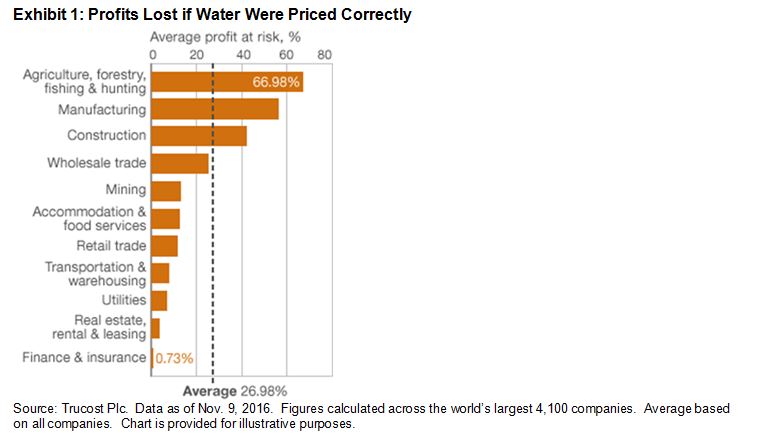

If water were priced to reflect this scarcity, Trucost’s analysis suggests that company profits would fall by nearly 27%, on average—with certain sectors significantly more exposed (see Exhibit 1).

Some companies already understand the risks and are acting to address them. The Spanish energy company Iberdrola carefully assesses its own use of water and that of its suppliers. Iberdrola details all of its supply chain’s water-related risks from a likelihood, financial-impact, and geographic-location perspective. Unfortunately, most companies do not pursue this level of risk management, so market participants may need to take the initiative to make sure they are not “hung out to dry,” so to speak. That may mean encouraging the companies they invest in to measure and disclose relevant water risks.

A number of larger and more sophisticated market participants are already doing this. A typical approach is to focus on certain sectors, identify material issues, and analyze company reporting on these risks, along with mitigation strategies. Trucost recently completed such an exercise for 120 global utility companies. The study found that the majority (approximately 55%) were not addressing water-related risks in a meaningful way. Only 5% of the companies provided robust reporting on how water risks are managed within their operations and along their supply chain. About 20% of the companies did have targets to reduce water consumption and usage intensity or increase water recycling. However, many of the targets did not specify a base year or even a target year.

For those market participants not yet looking at water risk, how should they begin to consider it alongside other risk management considerations?

The first step could be to create a water footprint of equity holdings to identify water-intensive companies, based on either direct use or supply chains. The second step would be to encourage these companies to report adequately on their water dependency and ability to manage associated risks. Ceres, a U.S.-based coalition of market participants, has produced “Aqua Gauge,” which is a framework for assessing corporate management of water risk.

There is significant legislation already, such as the EU Water Directive, and much more is on the way that seeks to bring about adequate water pricing as an incentive for the sustainable use of water resources. Market participants that consider water risk may encourage better company performance, better financial returns, and a better environment in which to enjoy them.

The posts on this blog are opinions, not advice. Please read our Disclaimers.