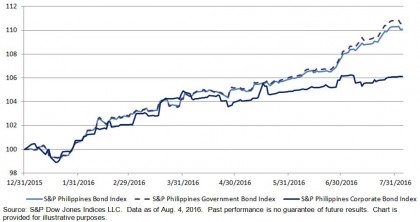

On Aug. 4, 2016, the Bank of England cut its benchmark rate by 25 bps to a low of 0.25%. This move, coupled with its announcement of a GBP 70 billion expansion of quantitative easing, with GBP 10 billion committed for the purchase of investment-grade corporate bonds, is furthering the positive performance of these asset classes. Quantitative easing is an asset-buying program that is meant to keep rates low to stimulate the economy.

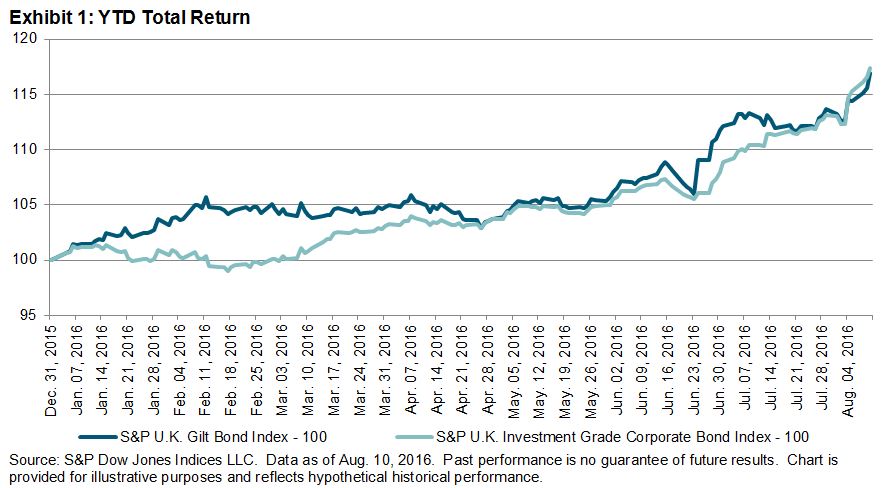

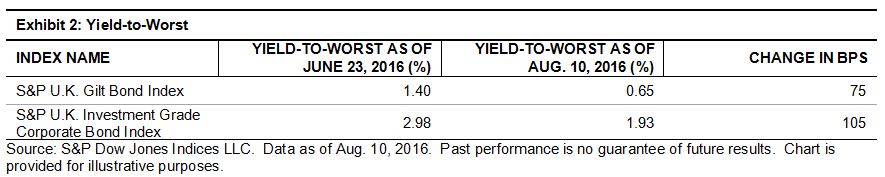

The S&P U.K. Gilt Bond Index had returned 16.93% YTD as of Aug. 10, 2016, while the S&P U.K. Investment Grade Corporate Bond Index came in at 17.32%. Both of these asset classes continue to rally. Since the vote for the Brexit on June 23, 2016, a rally based on flight to quality was largely expected for the U.K. gilt market, but the U.K. investment-grade corporate bond market has also has seen significant tightening of yields, despite concerns that a Brexit would negatively affect U.K. corporations. Since the Brexit vote, the S&P U.K. Gilt Bond Index has tightened 75 bps and the S&P U.K. Investment Grade Corporate Bond Index has tightened 105 bps.

The question remains as to how much lower yields can go and how the Brexit will actually unfold. Brexit impacts on the U.K. economy are starting to come in, with U.K. manufacturing output for Q2 2016 reversing its positive momentum and experiencing a sharp decline.