Publicly traded property stocks provide exposure to real estate, an illiquid asset class, without sacrificing the liquidity benefits of listed equities. Also, property stocks typically offer higher yields than the broad equity market, they may serve as an effective inflation hedging tool, and they may help diversify a portfolio due to their generally low correlations to stocks and bonds.

S&P Dow Jones Indices and NZX Limited jointly launched the S&P/NZX Real Estate Select in October 2015 to serve as an investable benchmark for real estate companies listed on the NZX. The index is designed to track the largest, most liquid property companies included in the S&P/NZX All Index. To reduce single-stock concentration, the index employs a semiannual stock cap of 17.5%.

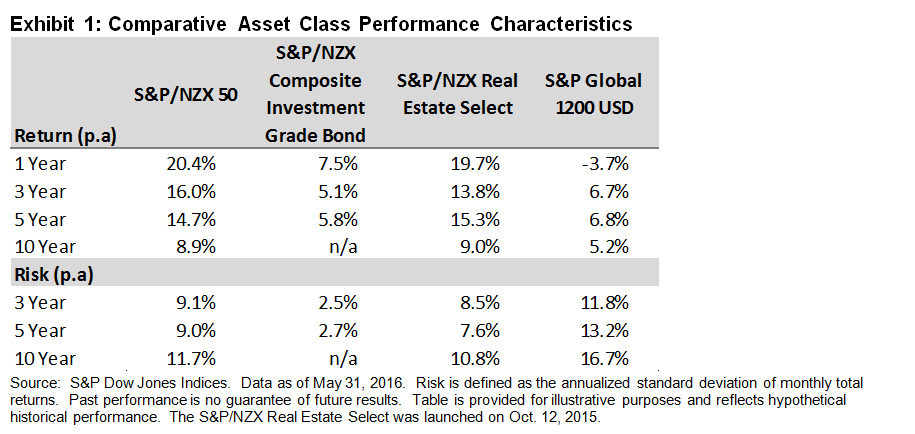

As depicted in Exhibit 1, total returns of New Zealand equities, as measured by the S&P/NZX 50, and property stocks, as measured by the S&P/NZX Real Estate Select, have been relatively similar over the longer term, while volatility has been modestly lower for property stocks. This is somewhat surprising given that global property stocks tend to have meaningfully higher volatility than the broader global equity market. As expected, investment-grade bond returns have been more modest, but they have been much less volatile compared to both equities and property stocks.

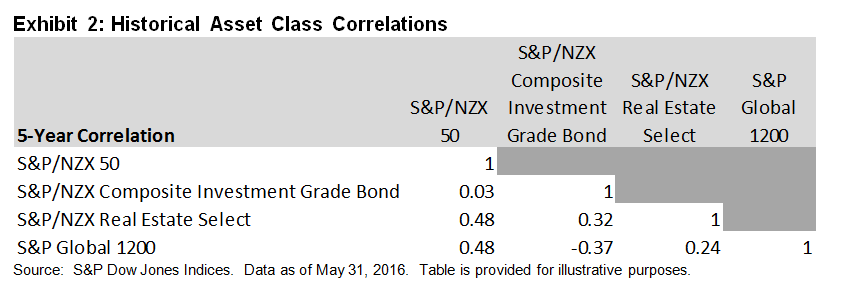

As shown in Exhibit 2, the S&P/NZX Real Estate Select has historically had relatively low correlations to both the S&P/NZX 50 and S&P/NZX Composite Investment Grade Bond Index. In fact, the correlation of 0.48 between New Zealand equities and New Zealand property stocks is equivalent to the correlation between New Zealand and global equities.

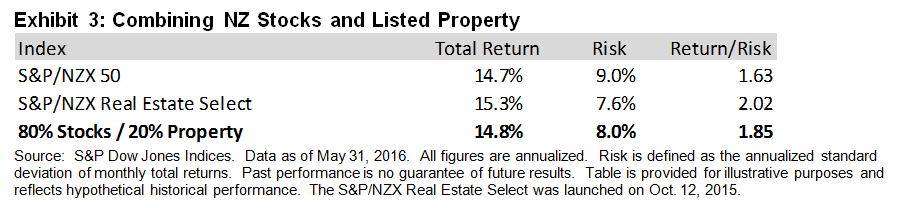

Exhibits 3 and 4 illustrate the potential diversification benefits of adding a listed property allocation to a stylized equity or equity/bond portfolio over the past five years. For example, a hypothetical 80%/20% combination of the S&P/NZX 50 and S&P/NZX Real Estate Select resulted in a meaningful reduction in volatility compared to a 100% position in the S&P/NZX 50. This was driven both by the lower risk profile of the S&P/NZX Real Estate Select as well as the relatively low correlation between the indices.

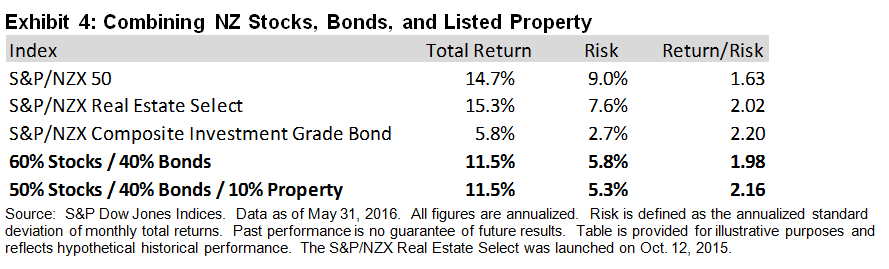

Similarly, adding a 10% listed property allocation to the equity portion of a 60% S&P/NZX 50 and 40% S&P/NZX Composite Investment Grade Bond Index portfolio resulted in a further reduction in volatility and higher risk-adjusted return over the trailing five-year period.

The posts on this blog are opinions, not advice. Please read our Disclaimers.