The world’s equity markets have encountered a rocky introduction to 2016; including the worst ever start for the Dow Jones Industrial Average (against a record that stretches back to 1897) and steep falls across developed and emerging markets. Equity markets are down more or less everywhere, and in many cases materially so.

What difference does a week make?

Does the performance in the first seven days of the year matter to investors who intend to hold through to year-end? One would suppose not especially: there are 51 weeks to go, we have covered less than 2% of the year and – in the abstract –the first week’s performance should have only a tiny (although certainly non-zero) influence on the whole year’s return. Yet, history suggests the opposite. Some weeks were more important than others, and the performance in first week of the year was particularly indicative of the year’s returns.

How important is the first week?

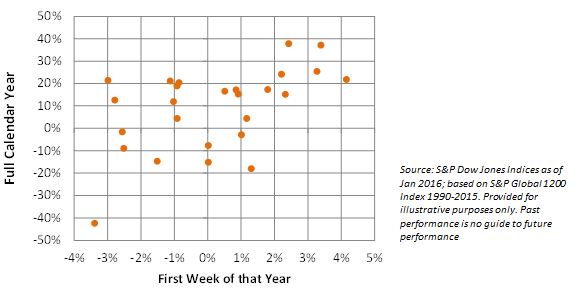

Taking the international blue-chip S&P Global 1200 and its performance over the past 25 years as our object of study (similar results may be obtained with the S&P 500), it is clear that there is a strong historical relationship between the performance during the first week of the year and the overall year’s return, with a positive correlation of 0.41.  Not all weeks are equally important

Not all weeks are equally important

Some weeks seem to be more important than others, or even provide an entirely opposite relationship to that expected; the third week in May, for example, seems to be negatively related to performance throughout the remainder of the year. (Support, perhaps, for notion that one should “sell in May and go away”.)

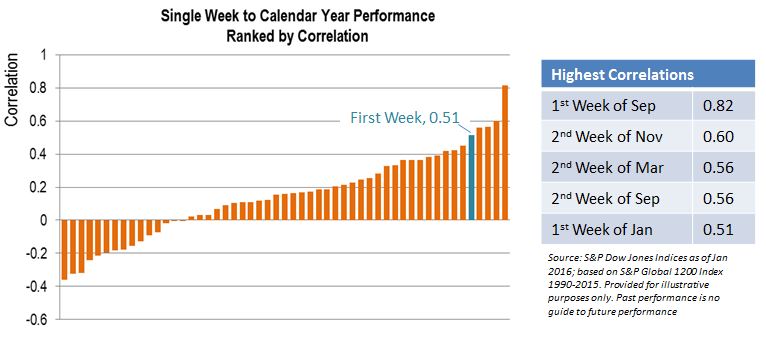

Which is the most important week?

Perhaps thanks to the return of investors from their holidays and the frequent location of elections during the period, the first week of September appears to be the most influential week for returns. This is followed by the second weeks of November and March, then the second week of September. The first week of the year appears in fifth place – still pretty influential, but far from the most important.

Conclusions

Historically speaking, years that have started badly have more frequently ended badly – and to a greater extent than might be supposed, given the expected impact of a single week’s performance. However, those who wish to divine the market’s yearly performance from that of a single week might be better off waiting until September.

The posts on this blog are opinions, not advice. Please read our Disclaimers.