Over the past few years, corporations have taken advantage of the low interest rate environment and have thereby increased the size of the corporate bond market considerably. Many of these bonds, however, are subject to the effects of rising interest rates. In fact, anticipation of this change in interest rates alone has already started to shake parts of the market.

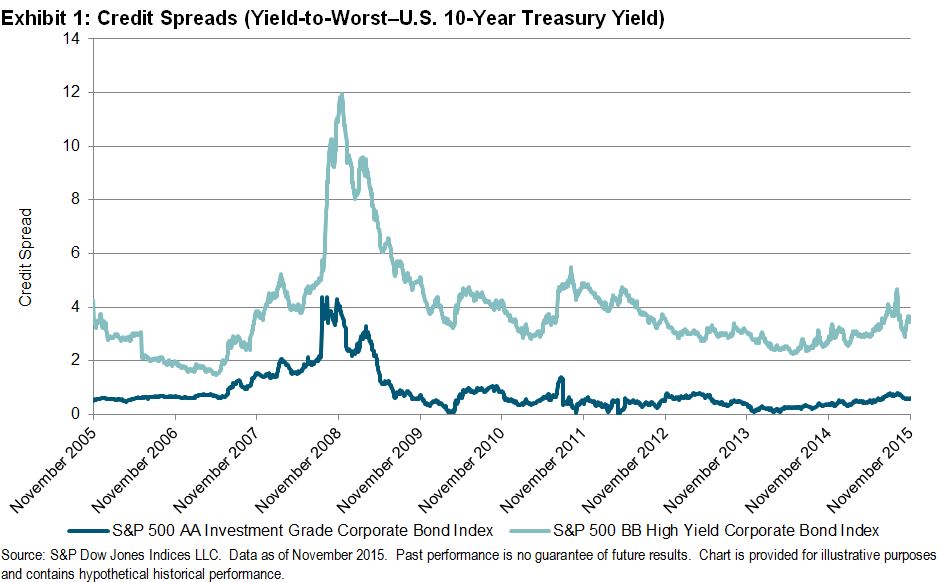

Credit spreads—the difference between the yield on a corporate bond and the yield on a treasury security of similar maturity—can be viewed as a reflection of the risk of default. Typically, wide corporate credit spreads indicate a riskier lending environment, as bondholders generally will only take on a greater risk of default in exchange for a greater yield. As the economy grows and companies’ financial health improves, credits spreads tend to narrow.

In examining the subparts of the S&P 500® Bond Index, we can take a deeper look at how credit spreads have changed for AA- and BB-rated corporate bonds issued by constituents of the S&P 500. Until recently, credit spreads had been narrowing to unusually tight levels over the past several years; low interest rates had starved fixed income investors from the yields available in years past. However, in recent months, there has been a widening of credit spreads in spite of low rates. In 2014, AA spreads ranged from 0.09% to 0.43%, while BB spreads ranged from 2.26% to 3.37%. In 2015, AA spreads ranged from 0.30% to 0.81%, while BB spreads ranged from 2.55% to 4.67%. Tight spreads meant that bonds cost more and yielded less. So, with the prospect of a greater payoff, this low-rate environment has become increasingly attractive to investors. The demand for incremental yield has started to outweigh the traditional risk/return model in the corporate bond market, as investors have begun taking on a relatively high amount of risk for a relatively low amount of incremental yield.