The end of last year saw Canada’s CPI move up from the October level of 0.7 to a 1.2 for December. Since then it has stepped up in 2014 peaking at 2.4 in June before trending back down to September’s 2.0. In light of this, the October report of 2.4 came as a surprise to the markets. The economy may be running faster than the central bank originally thought.

Inflation has exceeded the 2% target rate set by the central bank for 5 of the 10 months reported this year. Given the broad nature and speed of the price increases, market participants are contemplating the timing of a central bank rate increase. Higher interest rates slow inflation because the action reduces the amount of money in circulation.

The Bank of Canada feels confident that low interest rates are needed and that inflation is not a threat at this time. Although reassuring, this would be something global and local investors with investments in Canada will be watching closely in the near future. To date, the S&P Canada Sovereign Inflation-Linked Bond Index has returned 0.45% month-to-date and 13.9% year-to-date. The index’s real yield is a 0.45% while its yield with an inflation assumption is 2.51%. The largest year-to-date return since 2004 was the end of 2011’s return of 17.75% when CPI levels rose from 2.3 to 3.7 during the course of the year. For the 10-year period, the index has returned 5.99%.

Source: S&P Dow Jones Indices, data as of November 21, 2014

The posts on this blog are opinions, not advice. Please read our Disclaimers.

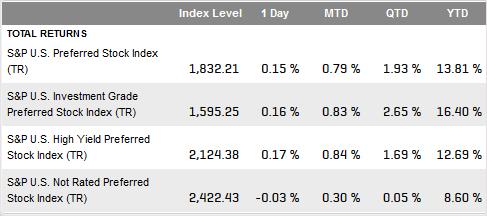

Like Preferreds, the difference in yield between the

Like Preferreds, the difference in yield between the