Investors – both stock investors and commodities traders – are having a bad week as oil prices fall lower and lower and the stock market follows close behind. (see chart 1) In all markets there are buyers and sellers and in the energy market most people (and most equity investors) are buyers. Cheap energy, especially cheap natural gas, is a boon to the US economy. Why is oil plunging? Where are the benefits?

Short term factors are behind the current oil price slide: signs of a deeper economic slowdown in Europe and the possibility of a German recession. Added to this are rumors that Saudi Arabia may have lowered prices to maintain its market share plus black market oil sales from some fields in Iraq controlled by ISIS and similar groups.

Larger longer run developments matter more: increased oil and shale oil production in the US and the US natural gas boom. US oil production has surged, oil imports are collapsing, and cheap natural gas is replacing both coal and oil in electric power generation. Cheap US coal is finding growing export markets in Europe, further lowering global energy prices. Results cited by the IMF in their just-published World Economic Outlook include rising US manufacturing exports, a smaller US trade deficit and increasing US competitiveness versus Europe and Asia. While oil price are sending stocks down today, the stage is being set for lower expenses and rising company profits in the near future.

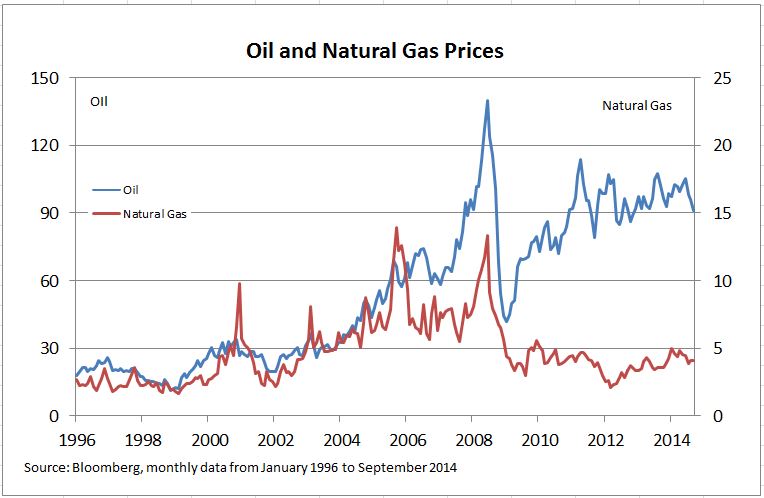

One measure of the impact of increased gas production can be seen in the second chart which shows the prices of oil and natural gas. Gas is priced per million BTU (a measure of energy) and oil is priced per barrel. A barrel of crude oil contains about six million BTU, so the price of oil should be six times the price of gas. The chart shows oil and gas prices with axes scaled 6:1. If oil and gas were both traded freely the two lines on the chart would coincide. However, exporting gas is very expensive, so rapidly growing US gas supplies tend to stay home, keeping gas prices low. On top of that, gas is generally cleaner and requires equipment to use.

To be fair, not all of the stock market gloom should be blamed on energy. Weak demand in Europe, politics in the Middle East and a bull market that is overdue for some corrective angst are all part of the picture.

The posts on this blog are opinions, not advice. Please read our Disclaimers.