The S&P 500 is maintained by a committee of market professionals. We publish a detailed methodology document which includes guidelines for selecting stocks and other changes to the index. Unlike many other S&P Dow Jones Indices and the majority of indices offered by other index providers, there are no rigid or absolute rules for the S&P 500; the Index Committee have some discretion in selecting stocks or responding to market events.

People ask why we have a committee when other index providers manage with a rule book. Larry Swedroe, writing on ETF.COM, unearthed an old argument that having the Index Committee means that the S&P 500 is actively managed; he concluded that this isn’t a problem. Some years ago Bill Miller, then a well-known Legg Mason portfolio manager with a stellar record of beating the market, noted that the S&P 500’s track record of being very hard to beat suggested that active management can succeed and that the Index Committee were actually good active managers.

The Index Committee’s mission in maintaining the S&P 500 is to represent the US equity market with a focus on the large cap segment. The Committee is not trying to pick stocks to beat the market. Rather, we use guidelines for stock selection – size, liquidity, minimum float, profitability and balance with respect to the market – to assure that the index is an accurate picture of the stock market.

If the only requirements for maintaining an index were getting the numbers right each day, a fixed rule book would suffice. But when the market doesn’t play by the rules, a rigid rule book won’t work. The Index Committee meets on a regular schedule and monitors the index and market developments. When guidelines or rules need to be reviewed, the Committee members understand the issues make needed changes. More importantly, when the unexpected happens, the Index Committee can respond quickly. Of course, the rules in a rules-based index can be re-written (and sometimes are). But who will re-write the rules? Are there rule-makers ready to act or does someone need to form a committee?

Looking back to the financial crisis and the weeks surrounding the collapse of Lehman Brothers was one of those unexpected moments. Shortly after Lehman filed for bankruptcy, the news broke that the US Treasury was bailing out AIG, one of the world’s largest insurance companies. Suddenly the Treasury owned over 90% of the company. The S&P 500 guidelines require that any company in the index have a public float of at least 50%. Under the rules, the index would have removed AIG. In those scary moments, dropping AIG would have sent the markets tumbling yet again. Given market conditions and investor fears, the Index Committee quietly set the 50% float rule aside. No trading was required. Fast forward a few years, the Treasury sold its shares back to the company and the 50% float rule was okay.

There are also other, less dramatic, cases. Last Spring’s stock split and issue of non-voting stock by Google resulted in changes to the S&P 500. That event showed that a Committee that continuously monitors the market is essential. When the Google action was announced, S&P DJI announced adjustments to the S&P 500 based on the index rules. Even though there was extensive news coverage of Google’s actions, major investors and index funds didn’t focus on how much trading what would be required until the schedule was published. Then some ETF issuers raised concerns. The Index Committee re-opened discussions, requested and received comments from many major investors and revised the treatment of Google’s split and the index rules. All this was possible only because the Committee understood the issues and was able to respond quickly. As to rules based indices — some of them mimicked the action taken by S&P DJI’s Index Committee.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

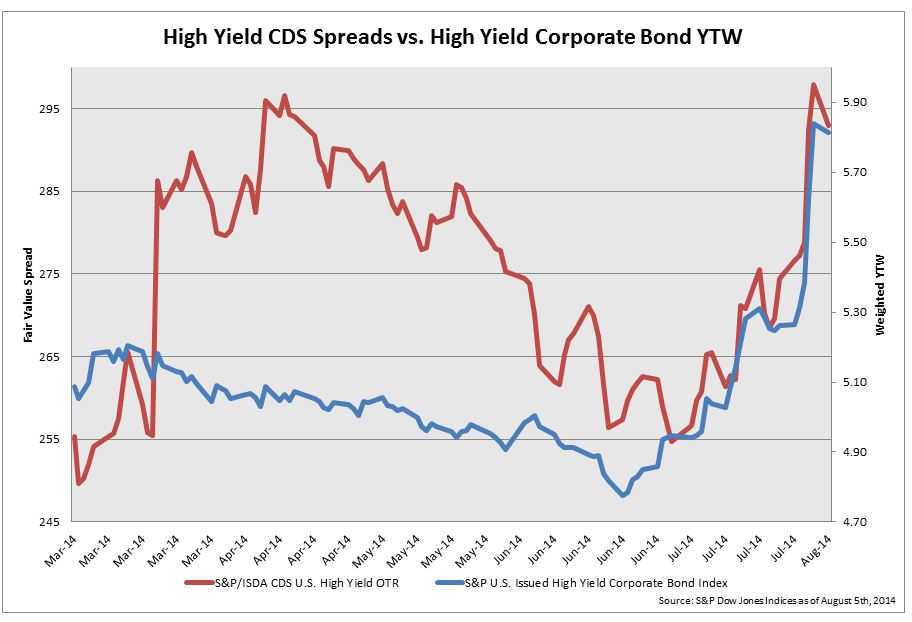

The divergence between CDS spreads and actual high yield bond yields show that the bond market has not followed CDS spreads movements due to the appetite for yield supporting the high yield market and pushing bond yields down. Argentina’s default caused bond yields to move more in line with the direction of CDS.

The divergence between CDS spreads and actual high yield bond yields show that the bond market has not followed CDS spreads movements due to the appetite for yield supporting the high yield market and pushing bond yields down. Argentina’s default caused bond yields to move more in line with the direction of CDS.