Many political analysts wrote about coalition politics in India with a deep rooted perception that it is here to stay forever. A stable central government with a single party majority is now a reality!! This has rightly been referred to as the beginning of a new era for India with a significant shift from complicated coalition politics.

During the first few days of living in this new era, I have been interacting with students, business community, CXOs of different industries, young professionals in early years of career and retired elders in the society – the common point of discussion was the election outcome, moving on then to different areas of expectations from the new government under the dynamic leadership of Mr. Narendra Modi.

The excitement, euphoria and now expectations can be seen and felt everywhere. There will be no magic wand which can make changes overnight.

One of the tailwinds for the new government would be India’s current demographic profile and its potential to supplement our transition as a global economic leader. However with increased longevity, the large young workforce of today will live longer and need much more support in the future which could pose some severe socio-economic challenges in the years ahead. India currently does not have a universal social security system similar to some of the developed nations and hence it is important to have a personal long term plan to ensure old-age financial security in the future.

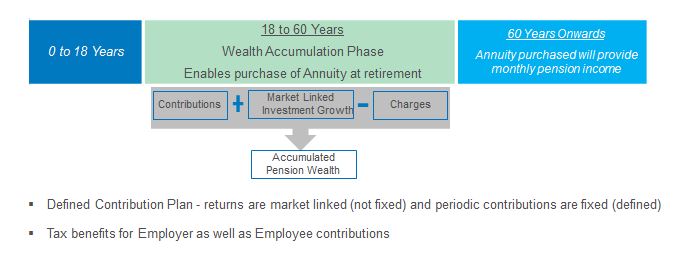

Pension schemes which are structured keeping in mind the retail individual and one of the lowest cost pension products in the world.It starts with a one-time process followed by regular investments with the option of taking a part of the corpus as lump sum amount and the balance in form of monthly income at retirement. It is often said that “Financial Planning in India = Tax Planning” . Some specific pension schemes meet this criteria by offering a special tax deduction for salaried employees over and above the usual deduction for investments of Rs. 100,000, for an amount up to 10% of Basic Salary without any monetary cap.

Monthly contributions ensure discipline of systematic investing. With the auto-choice option, allocation can be made amongst equity, corporate bonds and government bonds dynamically based on age profile.

Whether it is personal financial planning or strategic navigation of the government, the key is to have a steady focus on achieving long term goals. Making this point about long term focus, Mr. Modi said in his first speech at BJP’s Parliamentary Party meeting after elections that “…when we meet in 2019, I will give you and my countrymen a report card…”. A long term focus may, perhaps, augur well for many when it comes to taking stock of their future financial security.

The posts on this blog are opinions, not advice. Please read our Disclaimers.