The notion of an investment in equity of a public sector undertaking may appear to be a very stable investment with long term growth opportunity especially in developing countries like India. However if we explore the performance of the S&P BSE PSU with S&P BSE SENSEX in a five year horizon, the picture turns out to be a little different. S&P BSE PSU represents approximately 20% by full market capitalization of S&P BSE 500.

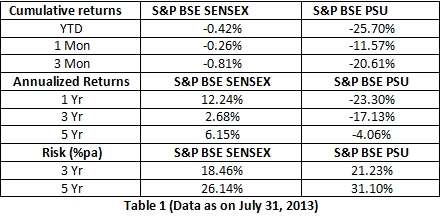

As on July 31, 2013 there is a huge gap between the year to date cumulative returns given by S&P BSE SENSEX (-0.42%) and S&P BSE PSU (-25.70%). On analyzing the returns for a five year period, S&P BSE SENSEX has given an annualized return of 6.15% whereas S&P BSE PSU has given -4.06%. The risk percentage per annum has also remained low in S&P BSE SENSEX as compared to S&P BSE PSU. Table 1 below summarizes the statistics of both the indices for a period of five year ending July 31, 2013.

S&P BSE SENSEX also consists of six PSU stocks out of which five have given negative annualized returns as on July 31, 2013.

Based on the above, we can conclude that most of the PSU’s have not been able to outperform the market.

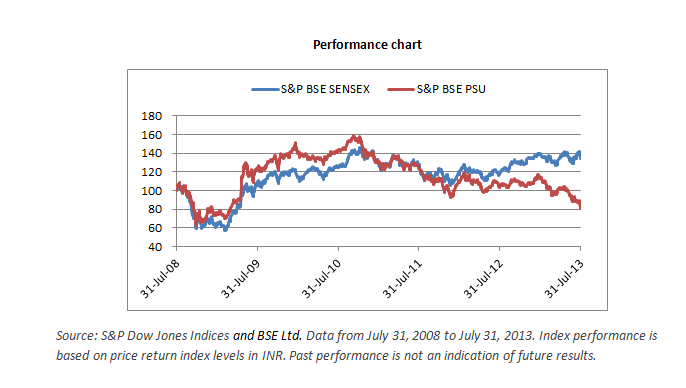

The posts on this blog are opinions, not advice. Please read our Disclaimers.Source: S&P Dow Jones Indices and BSE Ltd. Data from July 31, 2008 to July 31, 2013. Index performance is based on price return index levels in INR. Past performance is not an indication of future results.

S&P Dow Jones Indices is an independent third party provider of investable indices. We do not sponsor, endorse, sell or promote any investment fund or other vehicle that is offered by third parties. The views and opinions of any third party contributor are his/her own and may not necessarily represent the views or opinions of S&P Dow Jones Indices or any of its affiliates.