U.S. Treasury Bonds:

Treasury notes and bond as measured by the S&P/BGCantor US Treasury Bond Index started the year in negative territory, finally getting their head above water on a consistent basis around the beginning of April. The positive returns did not last long as they slipped into negative territory on May 13th and have remained at a loss since the 17th. The current year-to-date return of this index is -0.69%.

U.S. Corporate Bonds & Senior Loans:

Investment grade bonds as measured by the S&P U.S. Issued Investment Grade Corporate Bond Index have not performed any better than Treasuries. The yield of the corporate index widened by 40 basis points since the beginning of the month to a current 2.87%. The month-to-date return of this index currently stands at -0.75% while its year-to-date return turned negative on the 28th of May and is currently -1.41%.

The year-to-date return of the S&P U.S. Issued High Yield Corporate Bond Index has dwindled from its May 9th high of 5.43% to a current level of 2.25%. Similarly, the S&P/LSTA U.S. Leveraged Loan 100 Index, which measures the performance of below investment grade loan facilities, has gone from a May 22nd year-to-date high of 3.32% to a 2.5%. Senior loan’s lower return volatility to interest rate movements is apparent as high yield bonds have dropped 60 basis points from their highs, while senior loans have only given up 25 basis points. Up to this point, loans are outperforming high yield with a 2.5% year-to-date total return.

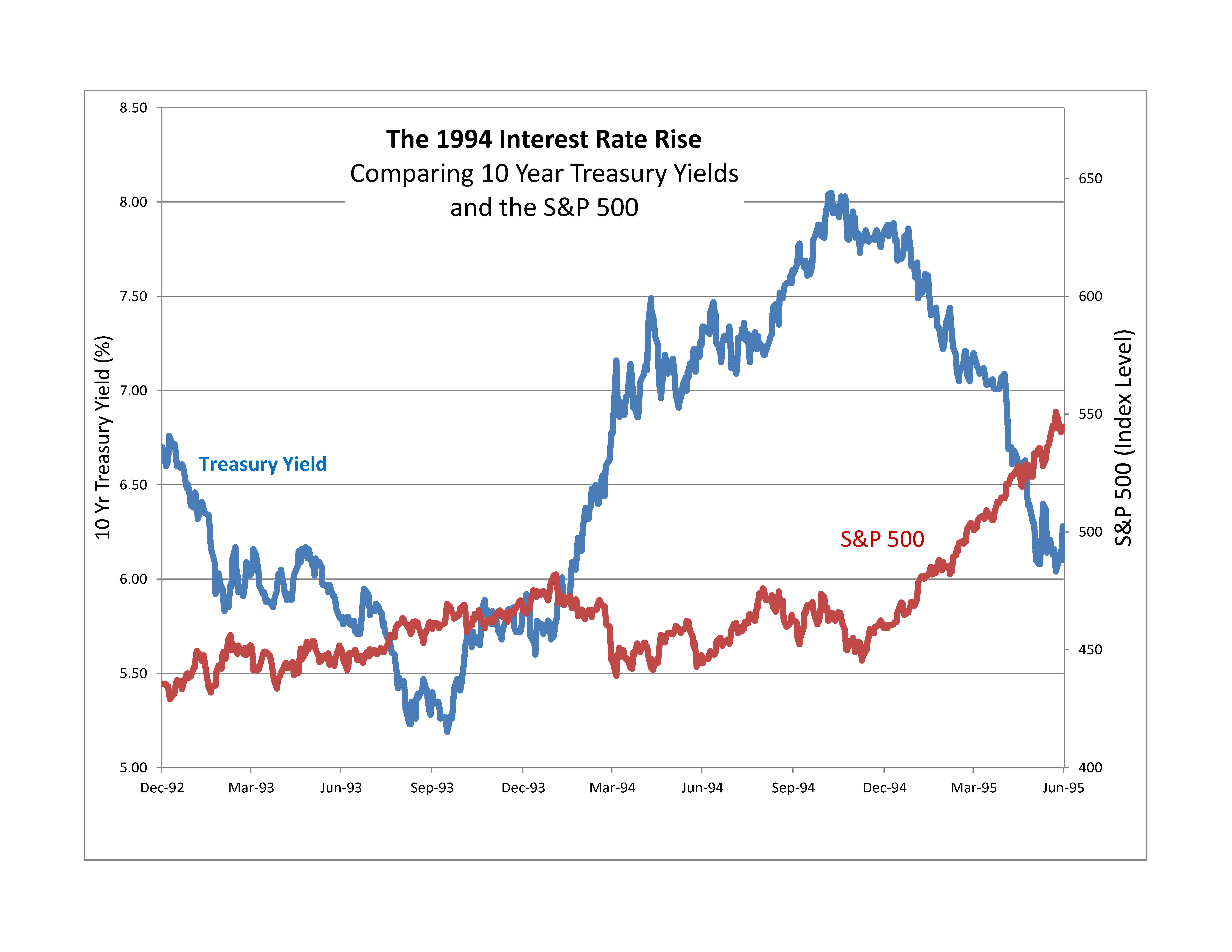

Source: S&P Dow Jones Indices LLC and/or its affiliates. Data as of Jun. 13, 2013. Past performance of the Index is not an indication of future results. Please refer to the methodology paper for the Index, available at www.spdji.com or www.spindices.com for more details about the index, including the manner in which it is rebalanced, the timing of such rebalancing, criteria for additions and deletions, as well as all index calculations. It is not possible to invest directly in an Index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.