One of the striking things about May’s U.S. equity performance was that although the market continued the strength it had shown between January through April, it was strong in a different way. http://us.spindices.com/documents/commentary/dashboard-us-20130531.pdf

For example, the best-performing sector in the first four months of the year was Utilities (up 19.74%); in May the Utilities sector declined -9.06%. At the other end of the spectrum, one of the worst-performing sectors earlier in the year was Technology (up only 5.54% while the S&P 500 was rising 12.74%). In May, Technology was among the best performers (up 4.55% versus 2.34% for to market as a whole). Not surprisingly, this shift away from more defensive sectors caused strategies like low volatility and high dividends, which had been stellar performers between January and April, to lag considerably in May.

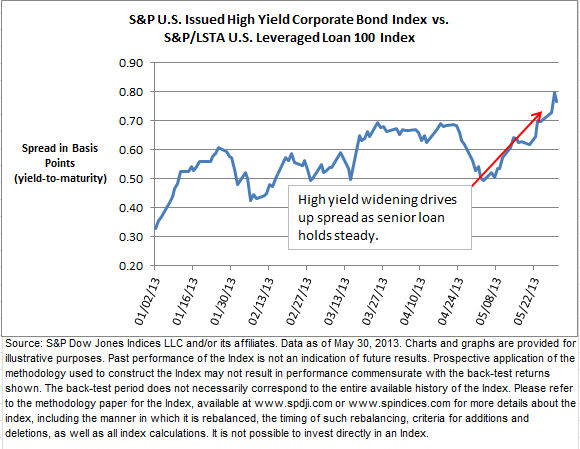

One obvious contributor to the rotation in equity sector performance was an equally notable shift in the bond market. At the long end of the curve, yields rose by more than 40 basis points in May. The S&P/BGCantor 20+ Year US Treasury Index, which had risen modestly in the first four months of the year, declined -6.71% in May (its worst decline since April 2009).

It’s not hard to make the case (e.g., see http://online.wsj.com/article/SB10001424127887324423904578520970034006496.html) that as bond yields rose in May, higher-yielding equity sectors such as Utilities became less attractive to income seekers, leading to their underperformance. But what happens now? If bond rates continue to rise, how likely is it that the equity market will continue its recent strength? And if equities weaken, is it possible that the lead might shift to defensive sectors once again?

The posts on this blog are opinions, not advice. Please read our Disclaimers.