Chairman Ben Bernanke has tried to be cautious in scripting a message to the markets, but recent communications out of the Federal Reserve have been mixed. With seven members of the Board representing 12 districts and past members all speaking to the press, the message can get convoluted at times. The planning and timing to pare down the central bank’s bond buying program is at the heart of the issue.

Richard Fisher, president of the Dallas Federal Reserve Bank, has been quoted as saying that the reason the country hasn’t seen more job growth is due to fiscal policy. He has been vocal about reducing stimulus purchases of Treasuries and mortgage-backed bonds, pointing to recent positive news on the recovering housing market.

Joining in the conversation is Philadelphia Fed president Charles Plosser, who also supports a gradual slowdown in bond buying.

Given such aggressive conversation by highly placed individuals, the market took heed as the yield on the S&P/BGCantor 7-10 Year U.S. Treasury Bond Index moved 45 basis points wider, from a recent low of 1.35% on May 1st to its current level of 1.80%.

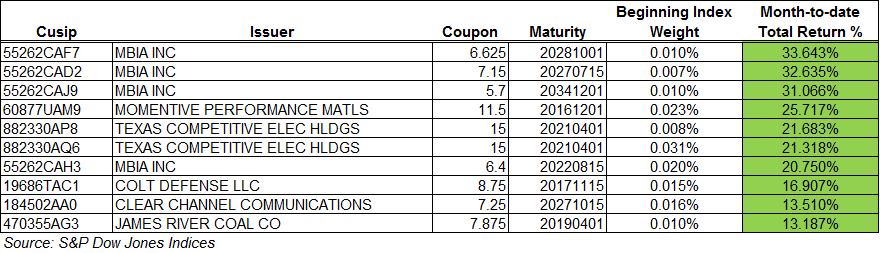

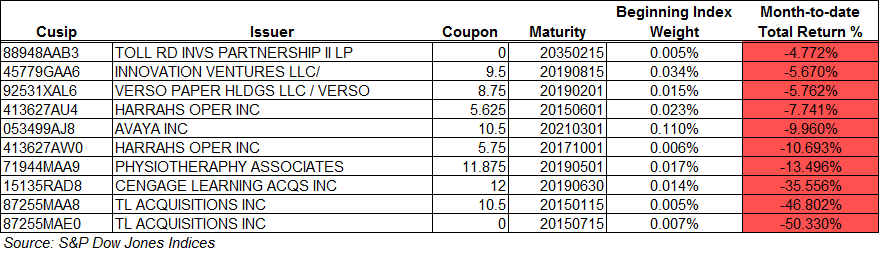

The rising interest rates also affect credit as the S&P U.S. Issued Investment Grade Corporate Bond Index returns a -1.98% month-to-date return and a -0.39% year-to-date. High Yield’s month-to-date return is presently negative at a -0.44%, while for the year it is returning a 4.05% as measured by the S&P U.S. Issued High Yield Corporate Bond Index.

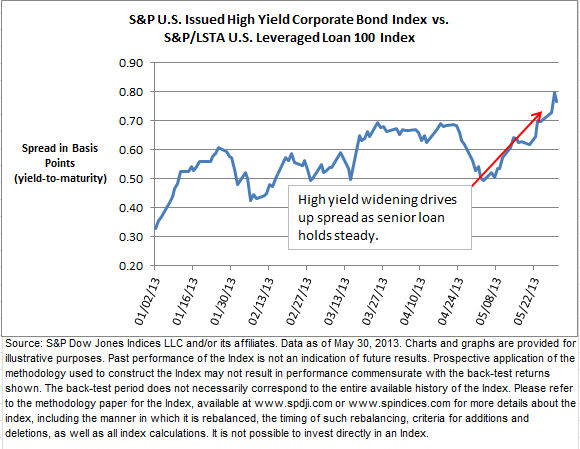

Senior Loans have held steady returning 0.19% to date and 2.93% for the year. The spread between the yield-to-maturity of the senior loan and high yield indices has widened since its start-of-the-year level of 33 basis points to its current level of 77 basis points. Though both the S&P/LSTA U.S. Leveraged Loan 100 Index and the S&P U.S. Issued High Yield Corporate Bond Index have seen their yields trend downward from the start of the year, loans have experienced more downward movement dropping 75 bps, while high yield only moved 31 bps. The S&P U.S. Issued High Yield Corporate Bond Index had held its relatively loftier rates until recently. Since May 8th, the yield on the index has increased from a 5.54% to 5.84%. The S&P/LSTA U.S. Leveraged Loan 100 Index yield stepped up a week and a half later, rising on May 23rd by 10 bps from 4.98% to 5.08%.

The higher volatility reaction to rising rates for high yield makes sense when compared to loans. High yield bonds have more interest rate sensitivity with duration of just less than 5 years and an average maturity of 6.8 years. Loans, on the other hand, have an average life of around 4 years. Their duration is 7 days, as the index is rebalanced weekly and adjusted for rate changes, making the S&P/LSTA U.S. Leveraged Loan 100 Index a floating rate product.

The posts on this blog are opinions, not advice. Please read our Disclaimers.