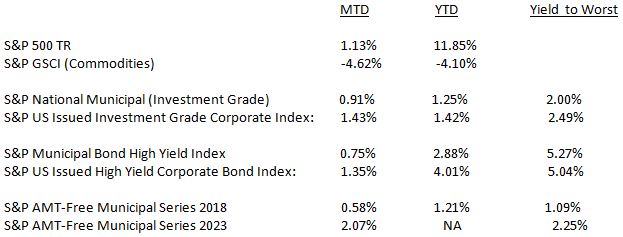

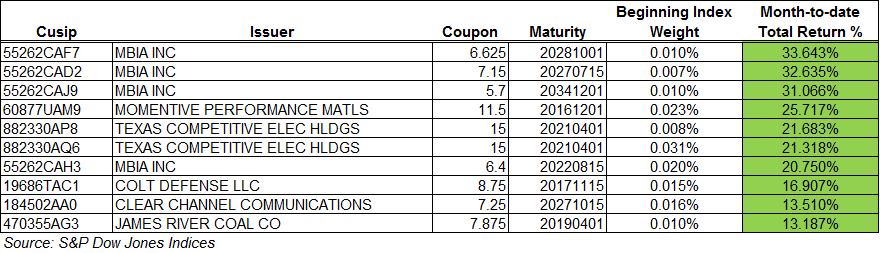

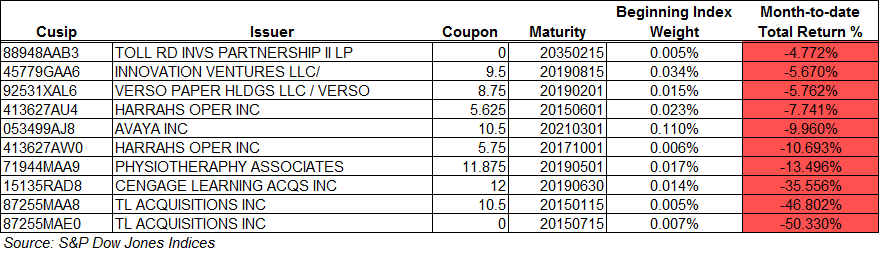

The index is up 0.42% month-to-date. Here is a performance review of the top & bottom 10 issues within the index.

Top 10 Issues

- May has been a good month for MBIA so far. The insurer settled a 2008 legal dispute with Bank of America concerning bad mortgage debt. The $1.7 billion settlement later led to a Standard & Poor’s rating upgrade, which moved the issuer’s senior unsecured debt from B- to BBB.

- Momentive Performance’s first quarter results of slightly lower sales but improving operating incomes, coupled with refinancing activities for a $270 million asset-based revolving loan and a $75 million revolving credit facility, moved this issuer’s bonds up.

- TXU bonds improved as Energy Futures Holdings Corp. looks to win support for a bankruptcy restructuring deal.

Bottom 10 Issues

- Cengage’s CEO has publically announced that the company may need to file for Chapter 11 and that no decision on a restructuring has been made.

- Physiotherapy Associates is in monetary default as a coupon payment has been missed.

- Harrah’s Operating Company bonds dropped as Ceasars Entertainment missed estimates due to revenue declines in their main markets.

The posts on this blog are opinions, not advice. Please read our Disclaimers.