Preferred stock is a hybrid security that has characteristics of both stocks and bonds. In the capital structure, preferred shares are subordinate to bank loans and senior corporate bonds, but they are senior to common stock. If a company had to file for bankruptcy and the assets of the company were liquidated, preferred shareholders would get paid after bond holders and before common stock holders. This leads to higher recovery rates than common stock, while at the same time offering much lower default rates compared to high-yield bonds.

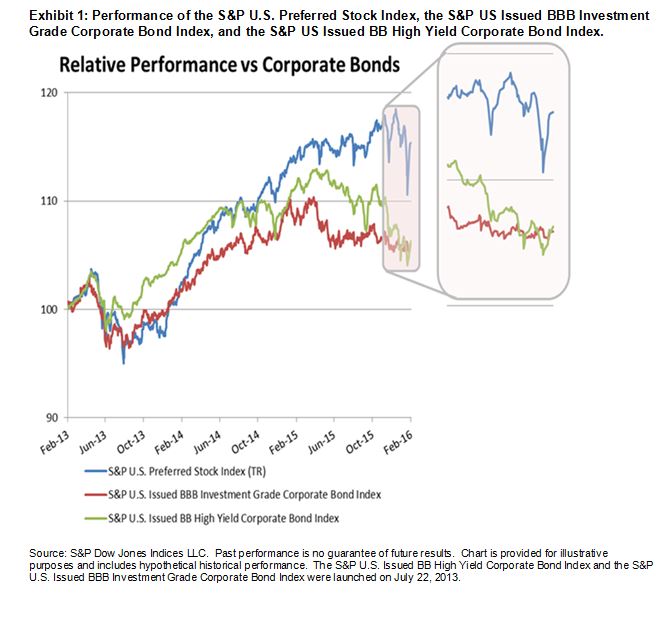

In low interest rate environments with narrow credit spreads, preferred stocks behave similarly to bonds. In periods of high volatility, they behave more closely to stocks. Exhibit 1 shows the performance of the S&P U.S. Preferred Stock Index compared to both the S&P US Issued BBB Investment Grade Corporate Bond Index and the S&P US Issued BB High Yield Corporate Bond Index.

Unlike common stock, most preferred dividends are cumulative, meaning dividend payments accrue even if not paid when scheduled. If a firm suspends paying dividends, it must pay preferred shareholders in full before paying any dividends to common shareholders.

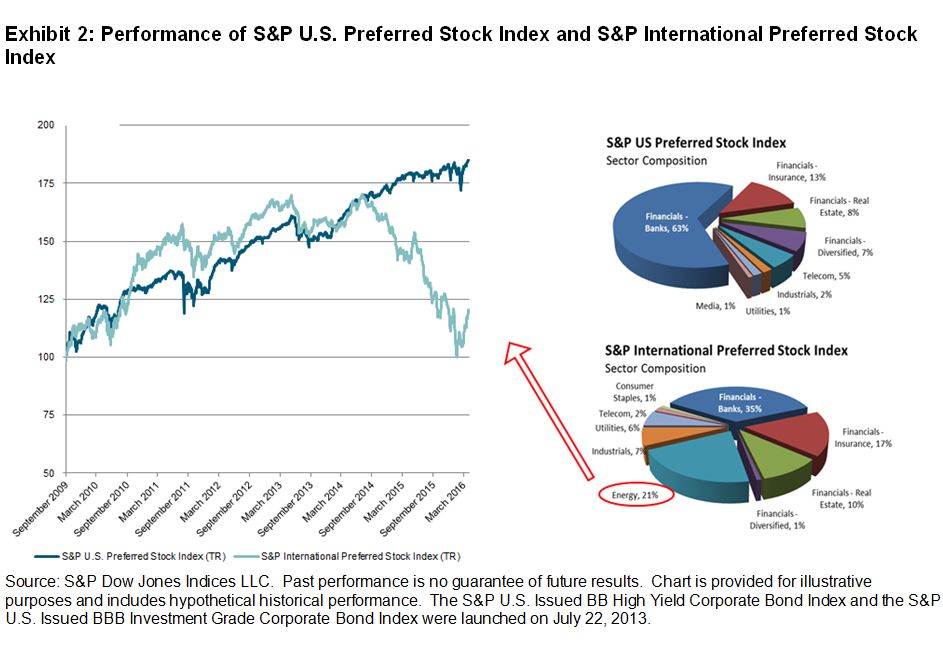

The energy sector has had a significant effect on preferred stocks. The impact of depressed oil prices is easily visible by comparing the performance of the S&P International Preferred Stock Index to that of the S&P U.S. Preferred Stock Index. Exhibit 2 shows the dramatic effect that exposure to the energy sector has had on preferred stocks. The S&P International Preferred Stock Index has over 20% exposure to companies in the energy sector; meanwhile, the S&P U.S. Preferred Stock Index has no exposure. As a result, the U.S. index has significantly outperformed its international counterpart. Since August 2014, the S&P U.S. Preferred Stock Index was up 10.0%, while the S&P International Preferred Stock Index was down -27.5% as of March 2016.