The market for credit default swaps is typically not well-understood by equity investors (myself emphatically included). This is unfortunate, since the price of insuring a company’s bonds (which is what a CDS measures) can sometimes provide insight into the same company’s equity securities.

For example, in September 2012, the S&P 500 financials sector began to open up a large performance advantage over the S&P 500, after running neck and neck with the 500 earlier in the year. But the relative price of insuring financial sector debt began to cheapen dramatically in May, four months before the start of the equity rally, as shown at http://us.spindices.com/documents/research/iis-leading-indicator-or-confirming-evidence.pdf.

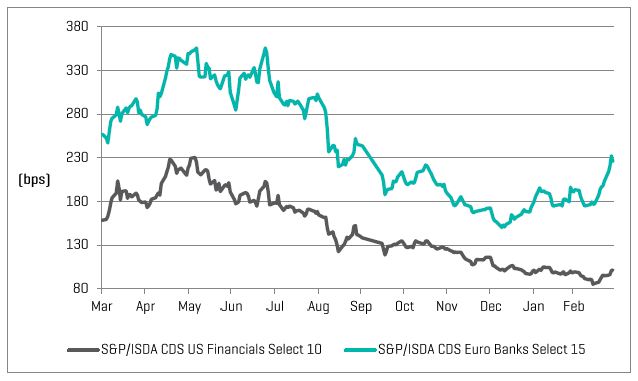

More recently, U.S. bank stocks performed much better than their European counterparts in the first quarter of 2013. This seems appropriate in view of the continuing supply of Cypriot headlines, although it’s notable that until mid-February the Europeans were in the lead. But the relative cost of insuring European bank debt began to increase in January – well before the equity markets adjusted. In anthropomorphic terms, the equity and CDS markets temporarily “disagreed;” the disagreement was resolved in February and March when European bank stocks underperformed (by quite a lot). (See http://us.spindices.com/documents/research/iis-european-bank-woes-reflected-across-asset-classes.pdf for more details.)

It appears, at least on the surface, that in these two cases movements in CDS prices foreshadowed later developments in the equity market. Of course two anecdotes do not a summer make. But the interconnections are none the less intriguing. In a world of integrated capital markets, equity and fixed income markets probably can’t agree to disagree for long.

The posts on this blog are opinions, not advice. Please read our Disclaimers.