From Efficiency to Security

Over the past few months, two themes have dominated market attention, artificial intelligence (AI) and energy supply. Each is driven by different forces, yet both are increasingly pushing governments in a similar direction—toward supply security and reduced external dependence.

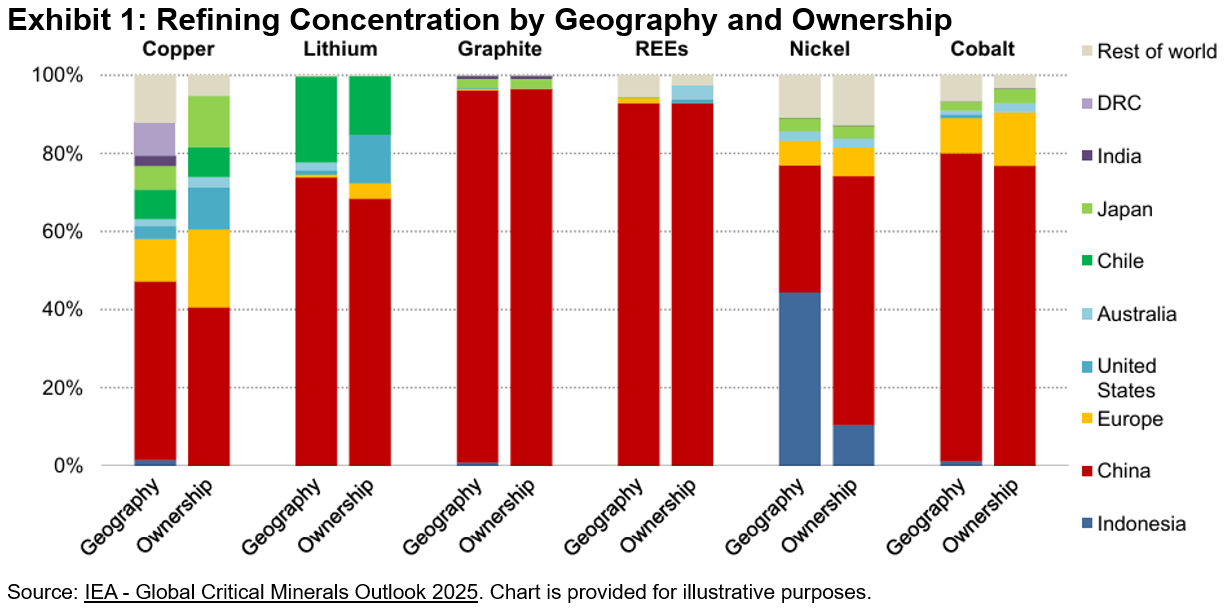

Recent developments help illustrate this shift. Reports of Anthropic restricting access to its latest AI models have raised concerns in Europe about reliance on external providers for critical AI technologies.1 At the same time, ongoing tensions around the Strait of Hormuz have highlighted the fragility of global oil and commodity supply routes.2 Earlier disruptions, particularly the world’s heavy dependence on China for rare earth elements (REEs), had already exposed similar vulnerabilities3 and prompted policy responses such as the EU Critical Raw Materials Act.4

These developments point to a meaningful shift. Access to key inputs is no longer guaranteed, and policy is moving from just-in-time efficiency toward just-in-case resilience.

Infrastructure Driving Critical Minerals Demand

One area where this shift is becoming visible is in demand for critical minerals.5 The buildout of digital infrastructure is driving demand, while concerns around supply concentration and security are bringing the supply side into sharper focus.

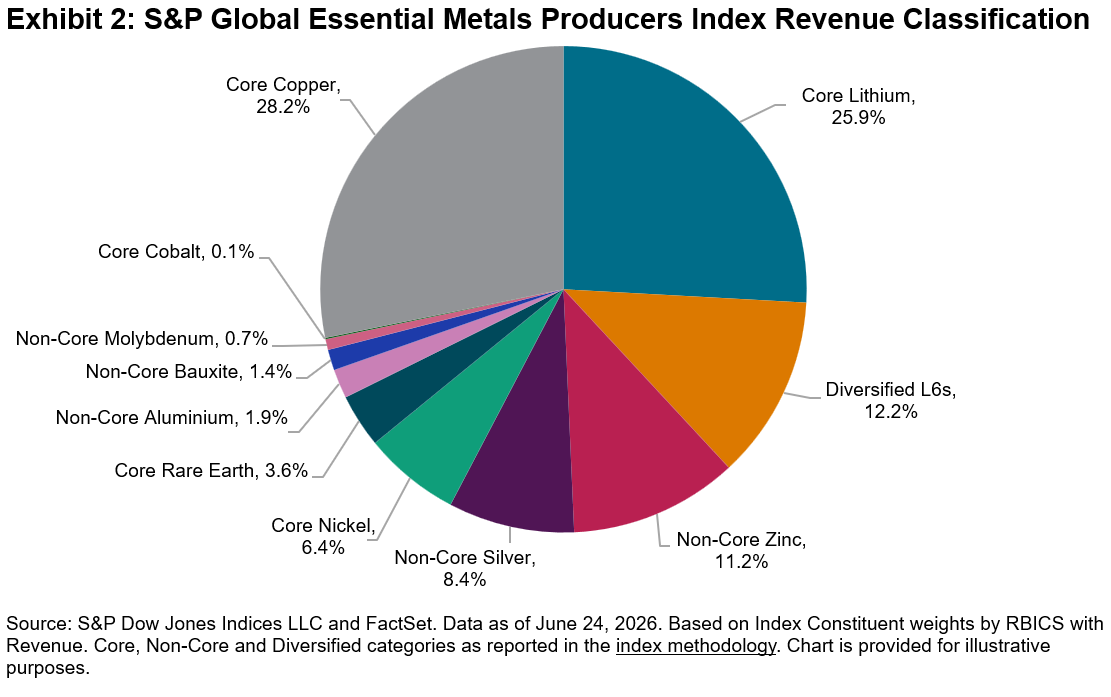

The S&P Global Essential Metals Producers Index, launched in August 2023, tracks companies involved in the extraction or ownership of reserves of essential metals, a subset of the broader critical minerals universe. These metals are central to two major transformations over the next decade: the expansion of AI and digital infrastructure, and the acceleration of the energy expansion.

The index goes beyond current production by incorporating both company revenues and estimates of underlying reserves, helping reflect future alongside present supply. Strong Performance Driven by Key Sub-Industries

Strong Performance Driven by Key Sub-Industries

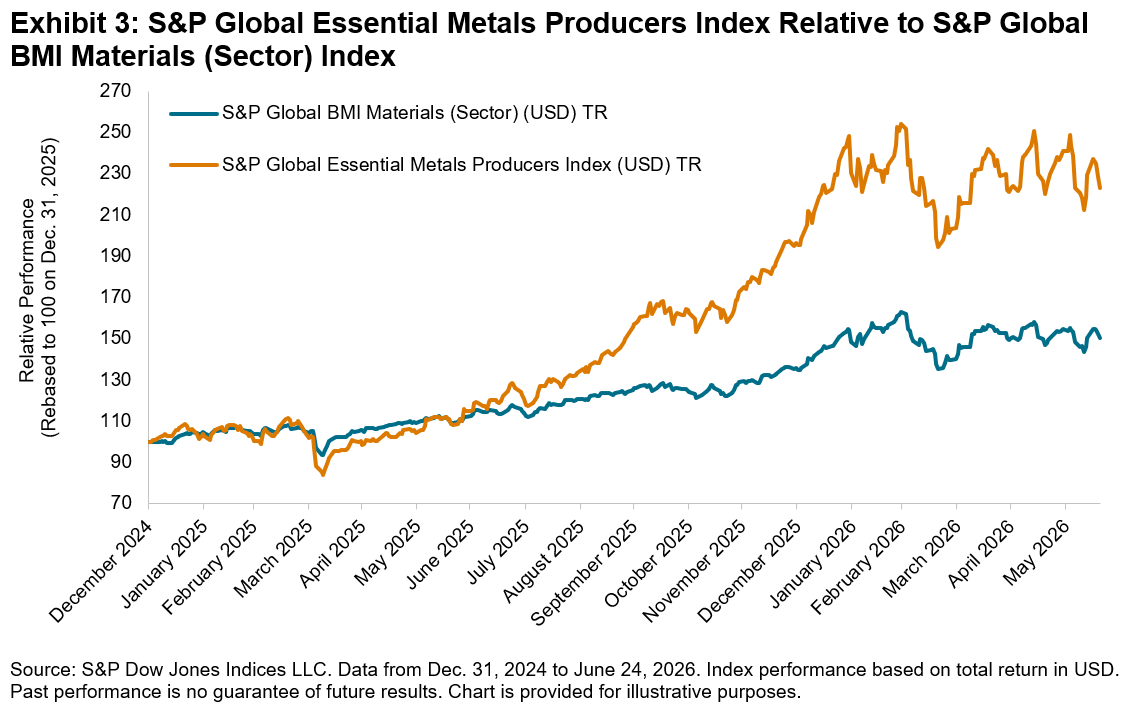

Following its launch in August 2023, the S&P Global Essential Metals Producers Index underperformed its starting level for an extended period, reflecting limited early attention to the theme. This changed in August 2025, when the index broke out of its range and rallied sharply. It nearly doubled by February 2026, outperforming the S&P Global BMI Materials (Sector) by 71%.

This performance was largely driven by companies within the Diversified Metals & Mining, Precious Metals & Minerals, Silver and Copper GICS® sub-industries. At the constituent level, Southern Copper Corporation and Boliden were the primary contributors.

More recently, geopolitical developments have tempered this momentum. The onset of the Iran conflict led to a period of consolidation, with the index moving within a narrower range since early March 2026. The index was up approximately 2% QTD as of June 24, 2026, broadly in line with the global materials benchmark. What stands out is the change in performance drivers. Earlier gains were broad-based, led by strong contributions from multiple GICS sub-industry groups. In contrast, recent performance has become far more concentrated, with only modest positive contributions from Diversified Metals & Mining (2%) and Copper (1%), while several previously supportive segments have turned into slight drags.

Structural Demand Meets Supply Constraints

The AI buildout is already underway, driving investment in data centers, power infrastructure and networks, and creating immediate demand for critical materials. This demand is structural, as it is tied to long-term infrastructure rather than economic cycles. Policy is reinforcing this, with governments prioritizing supply security and reducing reliance on concentrated supply chains.

At the same time, supply remains slow to respond, as new mining capacity can take years to develop. This combination of structural demand, supportive policy and constrained supply underpins a more durable outlook for the sector.6

The S&P Global Essential Metals Producers Index provides a barometer to track demand for critical materials and the evolving supply landscape. Its focus on companies involved in both demand growth and resource ownership helps illustrate how this segment evolves over time. Importantly, it reflects demand that is structural and tied to infrastructure buildout, rather than technology adoption cycles.

1 “EU Commission looking at practical consequences of Anthropic decision, spokesperson says,” Reuters, June 14, 2026.

2 Bazilian, Morgan and Jamie Webster, “How China Turned the Strait of Hormuz Crisis into an Advantage,” The National Interest, June 23, 2026.

3 Baskaran, Gracelin and Meredith Schwartz, “Rare Earth Export Restrictions One Year Later,” CSIS, April 27, 2026.

4 Critical Raw Materials Act – European Commission

5 What Are Critical Minerals and Materials? – U.S. Department of Energy

6 “Critical minerals outlook: surging demand, expanding supply chains,” JPMorgan Chase, Feb. 23, 2026.

The posts on this blog are opinions, not advice. Please read our Disclaimers.