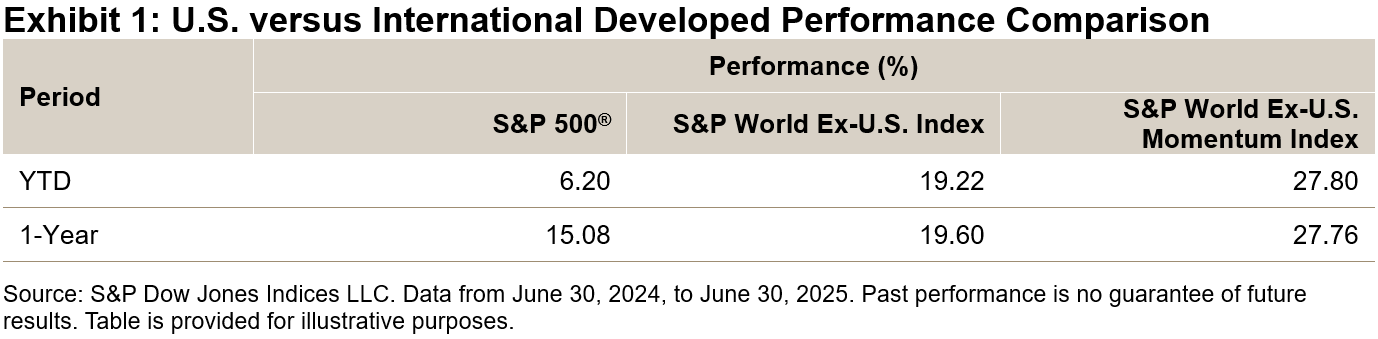

Many market participants have likely observed that the momentum factor has been among the top-performing equity styles in recent years. At the same time, a notable shift has occurred in regional performance: after years of underperformance, international developed equities are now outpacing U.S. equities—both YTD and over the past 12 months (see Exhibit 1). By applying a momentum strategy to international markets, market participants can measure both regional and stock-level trends, allowing them to have a view of the strongest-performing developed market stocks outside of the U.S.

The S&P World Ex-U.S. Momentum Index serves as a benchmark for securities in developed markets, excluding the U.S., that exhibit strong momentum characteristics. In this blog, we will explore the index’s methodology, performance attributes and sector and region weights.

Index Methodology

The S&P World Ex-U.S. Momentum Index selects constituents based on 12-month risk-adjusted price momentum, excluding the latest month to account for short-term reversal effects. Securities are weighted by the product of their market capitalization and momentum score, utilizing a relatively unconstrainted approach to achieve a purer focus on momentum.

Performance Comparison

Exhibit 3 shows that the S&P World Ex-U.S. Momentum Index outperformed its broader universe across all timeframes analyzed. Furthermore, it has delivered greater risk-adjusted returns over the full period, exhibiting higher upside and lower downside capture relative to the S&P World Ex-U.S. Index.

Sector Weight Analysis

As of June 30, 2025, the S&P World Ex-U.S. Momentum Index showed a significant overweight in the Financials sector, resulting in slight underweights across most other sectors. Over the full period, while sector weights have fluctuated in response to prevailing trends, there has not been a consistent bias, resulting in average weights that are generally aligned with the benchmark universe. This contrasts with other well-known factors such as value, growth, low volatility and quality, which often exhibit persistent biases to specific sectors.

Region Weight Analysis

There were also some significant regional deviations, with Japan displaying a 13.5% underweight in the S&P World ex-U.S. Momentum Index, while Germany and Canada showed overweights of 9.2% and 5.3%, respectively. Over the full period, the indices aligned more closely, with the most significant difference being a 3.7% overweight in Canada for the S&P World ex-U.S. Momentum Index.

Conclusion

The S&P World Ex-U.S. Momentum Index has outperformed its broader universe in both absolute and risk-adjusted returns for nearly 30 years of back-tested history. Currently, the index shows significant overweights in the Financials sector, as well as in countries like Germany and Canada. Given the recent trends, the S&P World Ex-U.S. Momentum Index may be especially relevant for tracking top-performing developed market stocks outside the U.S.

The posts on this blog are opinions, not advice. Please read our Disclaimers.