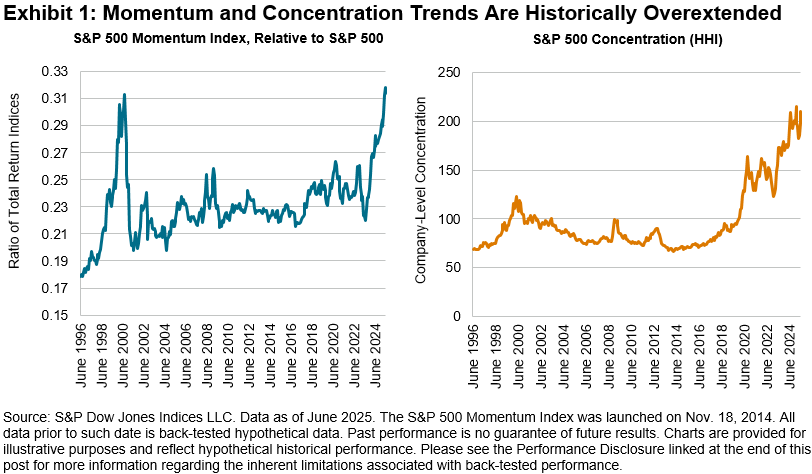

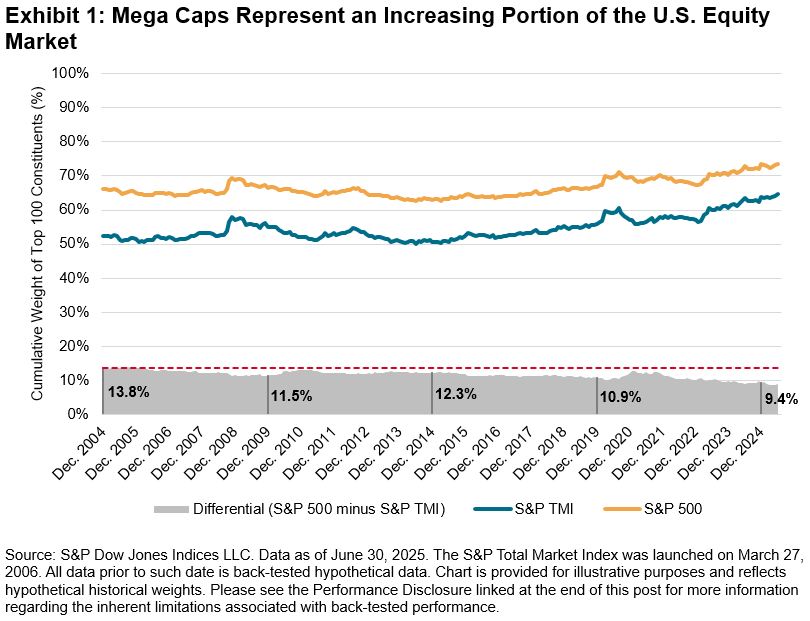

In today’s equity market, mega-cap stocks are not just influential—they have become a driving force shaping overall performance and strategic market dynamics.1 The increasing market dominance of the top 100 constituents, and the narrowing differential in cumulative weights of these names, in both the S&P Total Market Index (TMI)—which tracks the broad U.S. equity market—and the S&P 500® highlights this shift (see Exhibit 1).

The S&P 100 is designed to measure the performance of large-cap U.S. companies from The 500™ and comprises 100 blue-chip companies across multiple industry groups, offering a focused view of this robust and sizable segment of the market. The index’s construction follows a transparent and systematic approach to include the largest companies by total market capitalization. Generally, the largest companies in The 500 that have listed options are selected for inclusion into the S&P 100, and constituent selection is at the discretion of the Index Committee.2

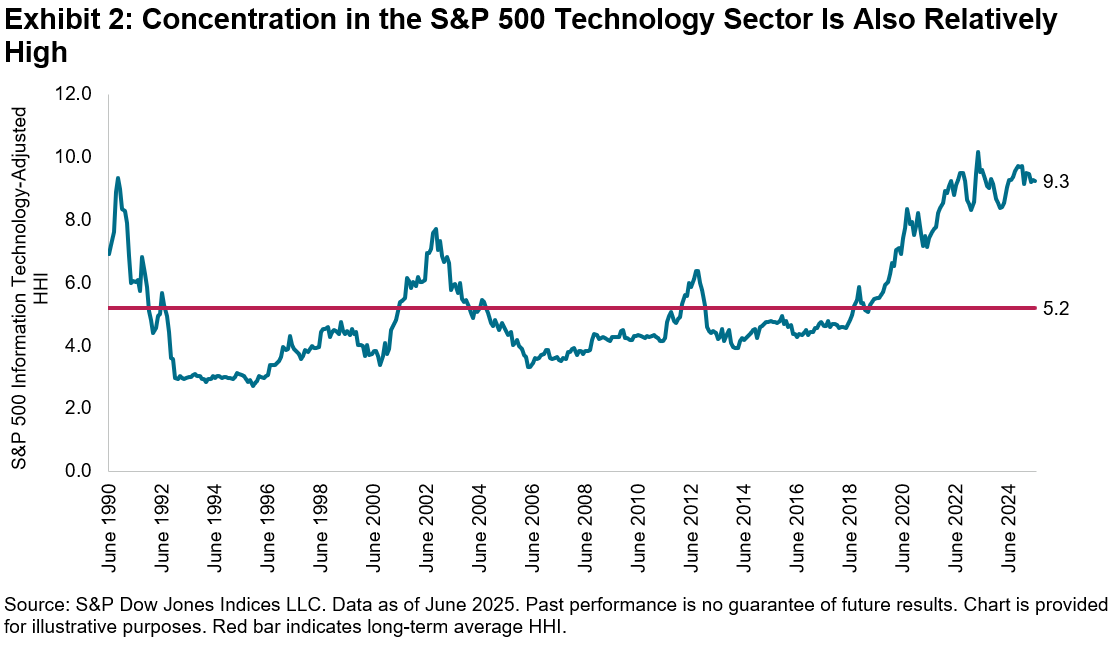

While mega-cap names have historically driven substantial and sustained market growth, led particularly by gains in the Information Technology sector,1 their increasing market concentration may present challenges. Equal-weight strategies can potentially help manage concentration risk by enhancing diversification through a more even weight across the segment, reducing reliance on a handful of dominant names and better reflecting gains when performance is more broadly distributed.3

The S&P 100 Equal Weight Index

The S&P 100 Equal Weight Index (EWI) is the equal-weight version of the S&P 100. The index has the same constituents as its capitalization-weighted benchmark, but each company is assigned an equal weight at each quarterly rebalance. Constituent changes to the equal weight index are incorporated alongside the S&P 100. If a company is added between rebalances, it generally takes the weight of the company that it replaced.2

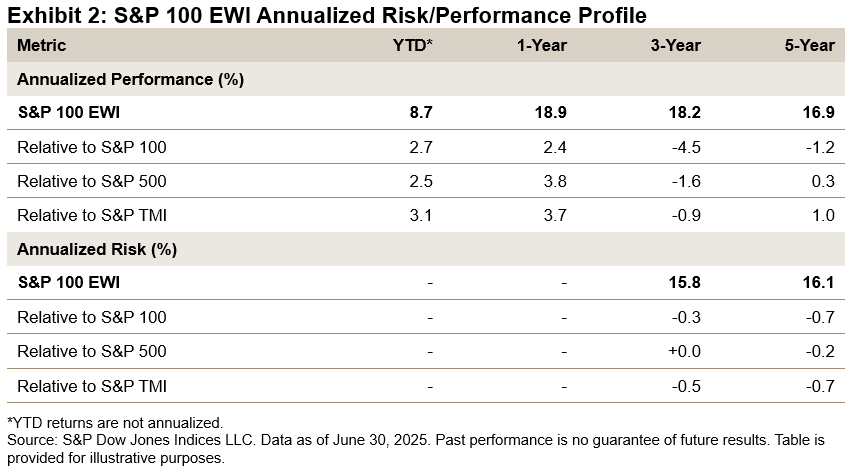

Why the S&P 100 EWI Matters

As of June 30, 2025, the S&P 100 EWI outperformed the market-cap-weighted S&P 100, S&P 500 and S&P TMI on a YTD and one-year basis (see Exhibit 2).

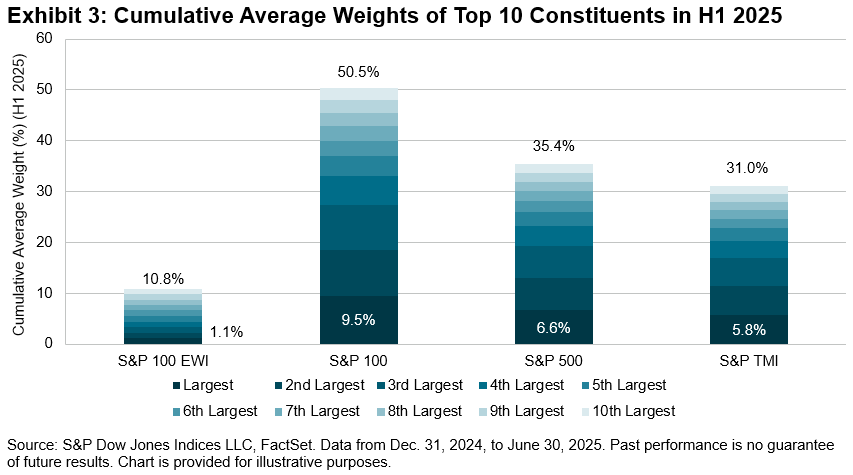

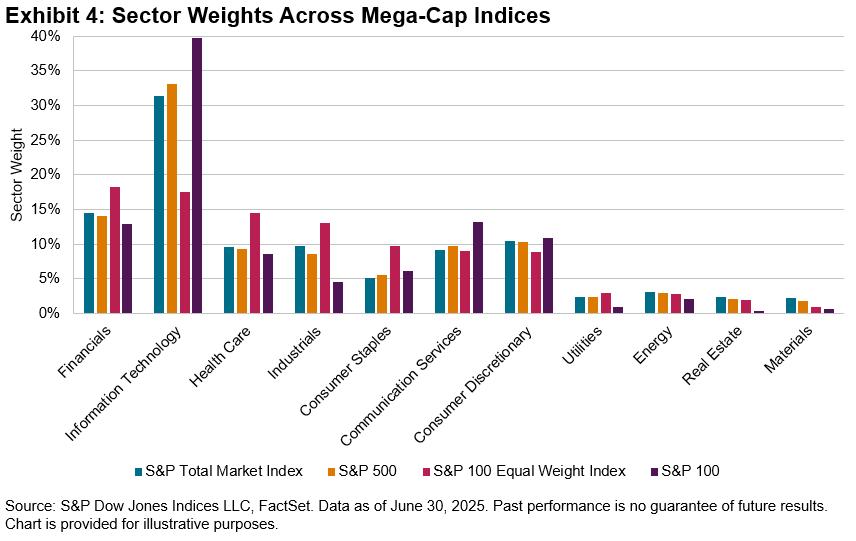

The divergence in performance between the S&P 100 EWI and market-cap-weighted indices highlights the impact of index construction. While the S&P 100 EWI offers balanced participation from all 100 companies, regardless of size, the market-cap-weighted S&P 100—along with The 500 and S&P TMI—tend to concentrate more heavily in the largest stocks (see Exhibit 3). Closely linked to this is the variation in sector composition between the indices. As of June 30, 2025, the S&P 100 EWI had comparatively lower weight in mega-cap Information Technology companies and higher weights in Financials, Health Care and Industrials (see Exhibit 4).

Conclusion

By providing an equal-weighted measure of the largest 100 U.S. companies, the S&P EWI offers a more balanced perspective on mega-cap performance. Accompanied by reduced concentration in top-heavy mega-cap names and broader sector views, it has outperformed its market-cap-weighted counterparts over recent periods. For market participants seeking a more diversified approach within the mega-cap segment, the S&P 100 Equal Weight Index may serve as a useful complement to traditional benchmarks.

1 Wang, Fei, “Exploring the U.S. Mega-Cap Landscape,” S&P Dow Jones Indices, April 2, 2025.

2 For more information, see the S&P U.S. Indices methodology.

3 See Edwards, Tim, et al. “Worth the Weight,” S&P Dow Jones Indices. July 23, 2024.

The posts on this blog are opinions, not advice. Please read our Disclaimers.