Developed Market Indices Continued to Outperform Conventional Indices, Emerging Markets Lagged

Global S&P and Dow Jones Shariah-compliant benchmarks outperformed their conventional counterparts YTD in 2019, as Information Technology—which tends to be overweight in Islamic indices—has been a sector leader, while Financials—which is underrepresented in Islamic indices—continued to underperform the broader market. The S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World gained 18.4% and 18.0% YTD, respectively, outperforming the conventional S&P Global BMI by approximately 200 bps.

The outperformance trend played out across major regions as Shariah-compliant benchmarks measuring U.S., Europe, Asia Pacific, and developed markets each continued to outperform conventional equity benchmarks by meaningful margins. Emerging markets and the Pan Arab region were exceptions, as Shariah-compliant benchmarks in these regions underperformed their conventional counterparts.

The outperformance trend played out across major regions as Shariah-compliant benchmarks measuring U.S., Europe, Asia Pacific, and developed markets each continued to outperform conventional equity benchmarks by meaningful margins. Emerging markets and the Pan Arab region were exceptions, as Shariah-compliant benchmarks in these regions underperformed their conventional counterparts.

U.S. Equities Led the Rest of the World through Q2 2019

Following robust gains in Q1 2019, positive U.S. equity performance continued throughout Q2 2019, leading conventional global equities YTD. A continued dovish stance from the U.S. Federal Reserve and hopes of relief in U.S.-China trade negotiations helped push U.S. equities higher last quarter. European and Asia Pacific equities followed in performance, as each enjoyed healthy gains over the period.

MENA Equities Underperformed – Country Results Varied

MENA equities, as measured by the S&P Pan Arab Composite, lagged marginally behind emerging market equities YTD, with a gain of 12.2%. Following robust Q1 2019 performance, the S&P Bahrain continued to lead the region YTD, with gains of 25.1%, followed by the S&P Egypt BMI, which added 22.0%. The S&P Saudi Arabia, which was promoted to emerging market status in March 2019, gained a favorable 15.9%. The S&P Oman lagged most, falling 2.6% YTD, followed by the S&P Qatar, which rose 1.6% YTD.

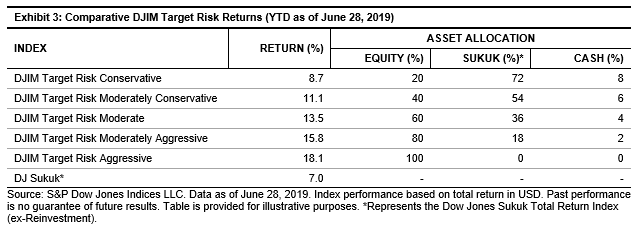

Varied Returns of Shariah-Compliant Multi-Asset Indices

The DJIM Target Risk Indices—which combine Shariah-compliant global core equity, sukuk, and cash components—generally underperformed the S&P Global BMI Shariah and DJIM World YTD. Performance of the comparably more risk-averse DJIM Target Risk Conservative Index was constrained by its 20% allocation to global equities in the expanding market environment, and the index ultimately gained 8.7% YTD. Meanwhile, the performance of the DJIM Target Risk Aggressive Index was driven by its 100% allocation to a mix of Shariah-compliant global equities, with the index returning 18.1% YTD, in alignment with the broader S&P Global BMI Shariah and DJIM World.

For more information on how Shariah-compliant benchmarks performed in Q2 2019, read our latest Shariah Scorecard.

A version of this article was first published in Islamic Finance News Volume 16 Issue 27 dated July 10, 2019.

The posts on this blog are opinions, not advice. Please read our Disclaimers. Financials—representing the largest sector of the index by weight—contributed most to the overall performance in Q2, adding 0.9% to the S&P China 500. The Financials sector gains were easily negated however, as the next three sectors by size—Consumer Discretionary, Communication Services, and Industrials each contributed -0.6%, -0.8%, and -0.8%, respectively, representing over 80% of index performance during the quarter.

Financials—representing the largest sector of the index by weight—contributed most to the overall performance in Q2, adding 0.9% to the S&P China 500. The Financials sector gains were easily negated however, as the next three sectors by size—Consumer Discretionary, Communication Services, and Industrials each contributed -0.6%, -0.8%, and -0.8%, respectively, representing over 80% of index performance during the quarter.

We also studied the distribution of fund returns and calculated their mean, standard deviation, and skew (see Exhibit 2). The study compared the fund returns data distribution with a hypothetical normal curve constructed with the same mean and standard deviation. Again, we considered the large-cap category and mid-/small-cap category for this analysis.

We also studied the distribution of fund returns and calculated their mean, standard deviation, and skew (see Exhibit 2). The study compared the fund returns data distribution with a hypothetical normal curve constructed with the same mean and standard deviation. Again, we considered the large-cap category and mid-/small-cap category for this analysis.