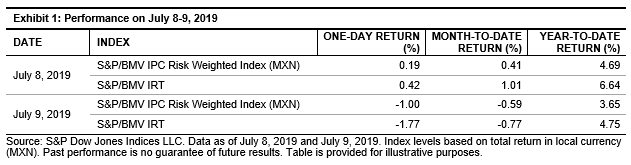

Mexico’s Finance Minister, Carlos Urzúa, abruptly resigned on July 9, 2019 over policy disagreements with the current government.[1] Market participants reacted negatively, generating volatility in the Mexican peso’s exchange rate, which fell 2.3% right after the announcement,[2] and the country’s equity market, and bringing a trial by fire for the S&P/BMV IPC Risk Weighted Index (MXN).

The S&P/BMV IPC Risk Weighted Indices aim to offer upside participation and downside protection, which was evident in their performance after the recent events in Mexico. While the total return of the flagship S&P/BMV IPC lost 1.77% in a single day, the low volatility strategy for Mexico, represented by the S&P/BMV IPC Risk Weighted Index (MXN), fell just 1%. The S&P/BMV IPC Risk Weighted Index (MXN)’s one-day outperformance of 77 bps showed a reversal in the indices’ month-to-date performance and reduced the difference in year-to-date returns (see Exhibit 1).

The bad news of this event is that market sentiment perceives instability in Mexico.

The good news is that this event proved the advantages a low volatility strategy can provide.

[1] NYTimes.com: Mexico’s Finance Minister Resigns, Rebuking the President’s Policies

[2] Mexico Peso Falls as Investors Fret Over Finance Minister’s Exit – Bloomberg

The posts on this blog are opinions, not advice. Please read our Disclaimers.

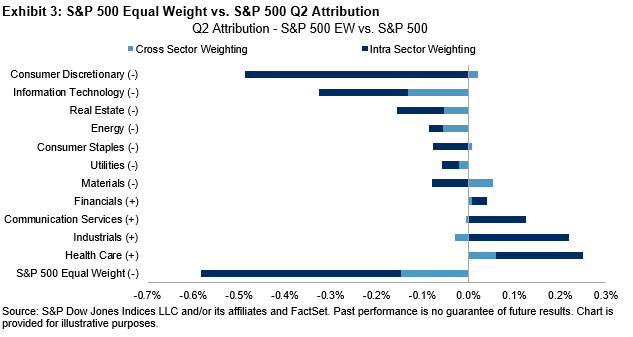

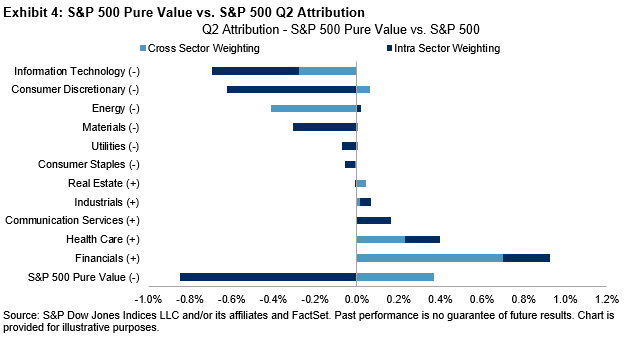

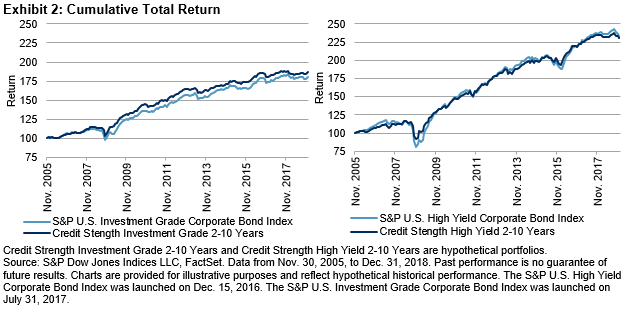

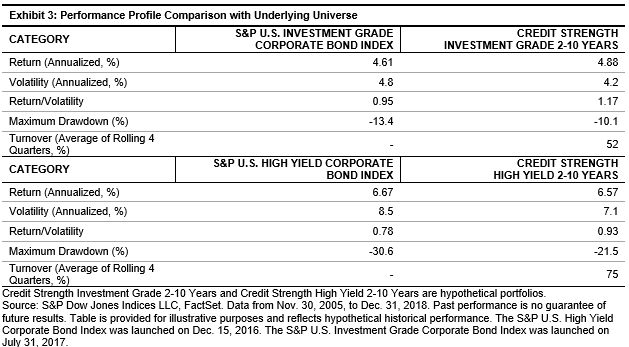

Exhibits 2 and 3 compare the back-tested performance of the credit strength portfolios with the underlying broad market indices. For investment-grade and high-yield bonds, credit strength portfolios reduced return volatility and improved risk-adjusted returns. The maximum drawdown was lower than the underlying universes during market downturns.

Exhibits 2 and 3 compare the back-tested performance of the credit strength portfolios with the underlying broad market indices. For investment-grade and high-yield bonds, credit strength portfolios reduced return volatility and improved risk-adjusted returns. The maximum drawdown was lower than the underlying universes during market downturns.

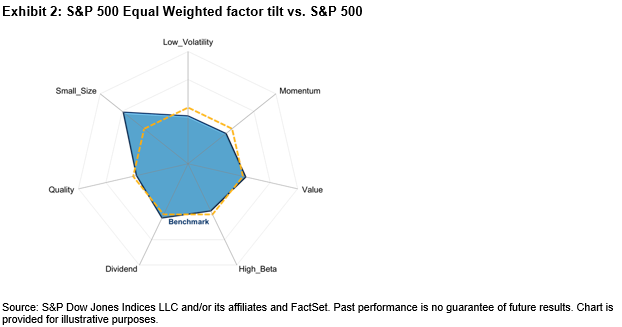

Equal Weight is a particularly good illustration of the small-size effect, since it holds the same stocks as the cap-weighted S&P 500. Exhibit 2’s factor exposure chart makes Equal Weight’s small cap tilt clear. Given

Equal Weight is a particularly good illustration of the small-size effect, since it holds the same stocks as the cap-weighted S&P 500. Exhibit 2’s factor exposure chart makes Equal Weight’s small cap tilt clear. Given