Sales of new and existing single-family homes have fallen since their recent high in November 2017 while pending home sales are flat to down so far this year. Starts of new single-family homes are volatile but also remain below the peak seen at the end of 2017. Recent press reports of declining activity in several major markets including Seattle, San Francisco and New York City confirm the statistics.

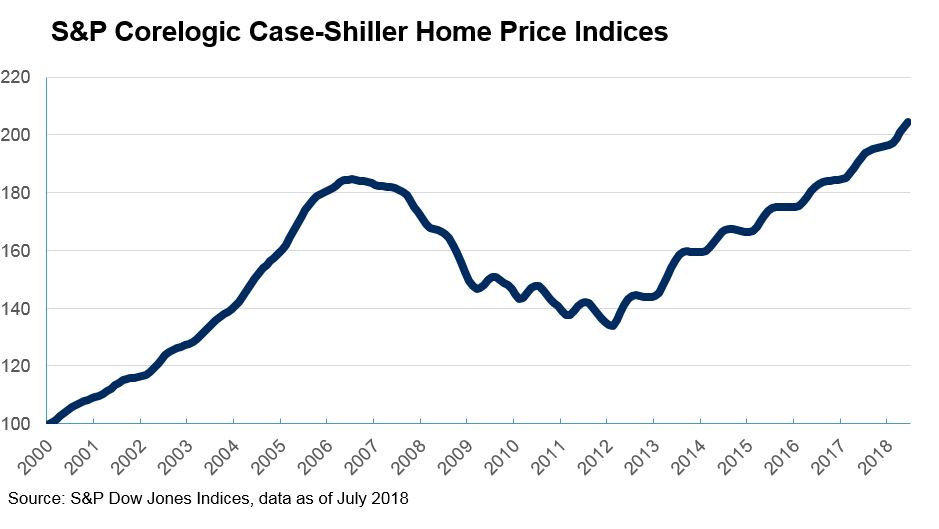

One factor depressing home sales is rising prices. The S&P CoreLogic Case-Shiller Home Price indices show prices rising at a 6% annual rate over the last year and a half. The pace may be welcome news to selling homeowners, but it is pricing buyers out of the market. Compared to 6% price gains, inflation is about 2% and wage gains are approaching 3%, squeezing some potential buyers out of the market. Mortgage interest rates are also creeping upward, raising monthly mortgage payments. The recently passed Federal tax law adds further pressure. The cap of the deductibility of property tax could raise the cost home ownership.

The slowdown in housing is not good news for the economy. While residential construction is a small portion of GDP, sales and remodeling of existing homes affect large sections of the economy. Further, signs that future homebuyers are being priced out of the market will dampen consumer sentiment. Traditionally housing and auto sales follow similar patterns; auto sales are down for much of 2018 though they rebounded in September.

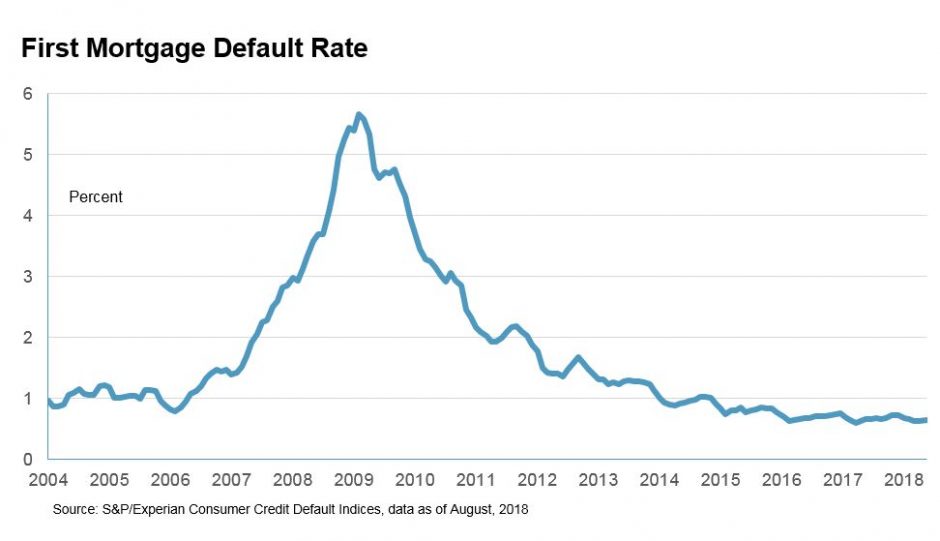

A positive note to end with is the first mortgage default data from the S&P/Experian Consumer Credit Default indices – defaults are lower now than before the financial crisis.