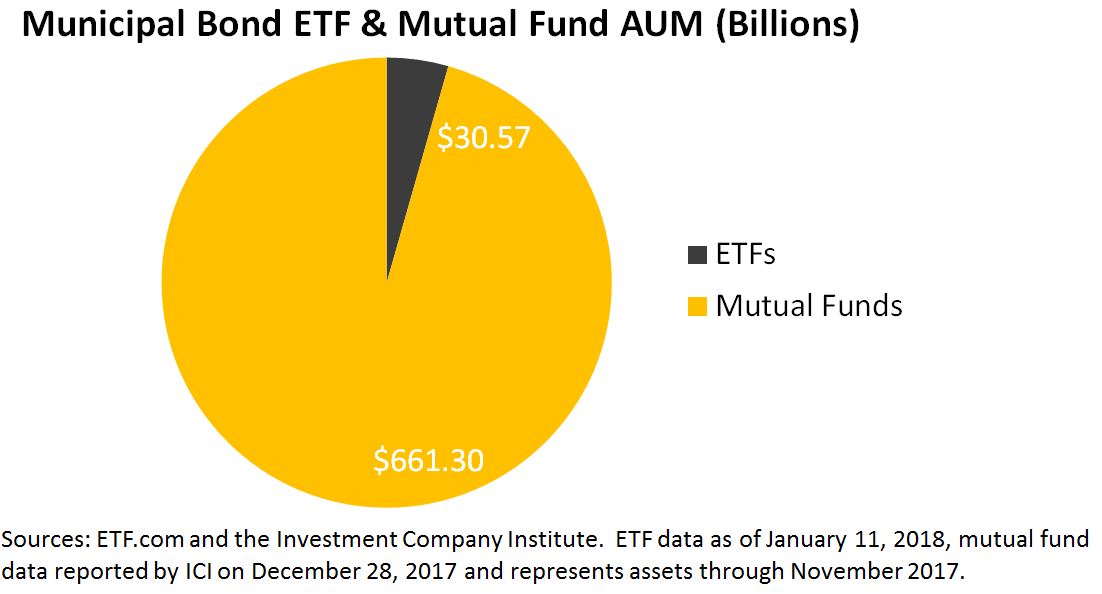

The first Exchange Traded Funds (ETFs) tracking municipal bonds were launched in September 2007. Since then the municipal ETF market has grown to 40 ETFs representing over $30.5billion in assets under management.

Municipal Bond ETF Market Snap Shot:

- 40 ETFs all but one represents tax-exempt municipal bonds. There is one ETF tracking taxable municipal bonds.

- $30.5billion in ETF assets (4.4% of total ETF and mutual fund assets)

- 8 ETFs have assets over $1billion

- 16 ETFs have assets between $100million and $1billion

- 16 ETFs have assets of less than $100million

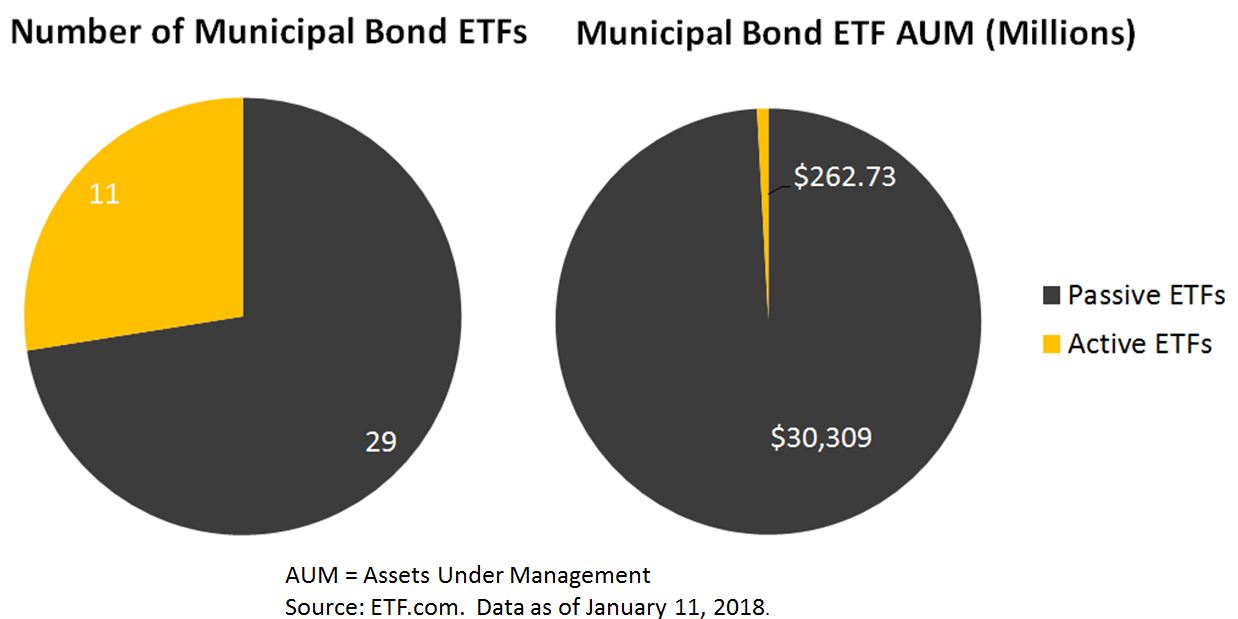

- 29 ETFs are passively managed (representing over 99% of assets)

- 11 ETFs are actively managed (representing less than 1% of municipal ETF assets)

Chart 1: Municipal ETF and Mutual Fund Assets:

Chart 2: Number of Municipal ETFs and Accumulated Assets:

Chart 3: Active & Passive Municipal Bond ETFs:

For more information on the municipal bond market performance please go to our website www.spindices.coom

Please also join me on LinkedIn: www.linkedin.com/in/james-j-r-rieger-9324558

The posts on this blog are opinions, not advice. Please read our Disclaimers.