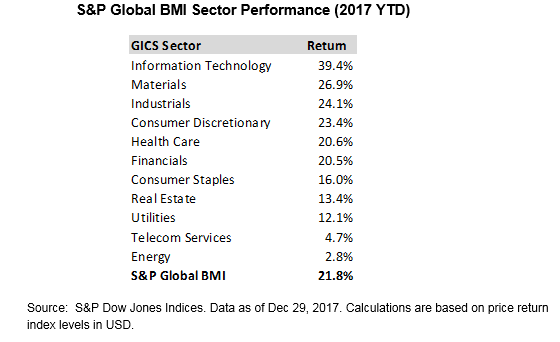

Most S&P and Dow Jones Shariah-compliant benchmarks outperformed their conventional counterparts for the year as information technology companies—which tend to be overweight in Islamic Indices—gained a whopping 39.4% beating the overall market by a wide margin, and financials—which are underrepresented in Islamic indices—experienced some weakness. This marked a reversal from 2016 where a surge in the financial sector late in the year caused Shariah-compliant benchmarks to lag. One notable exception to the 2017 trend was in the middle-east where conventional and Islamic benchmarks tracked closely together since technology stocks are not a meaningful portion of the regional market.

Despite Strong Absolute Returns, U.S. Equities Lag Global Markets for the First Time Since 2012

Global equity markets powered higher in the 4th quarter capping a very strong 2017. The S&P Global BMI Shariah and Dow Jones Islamic Market World each gained about 25% for the year, beating their conventional counterparts by more than 300 basis points. Emerging markets continued to lead the way as the DJIM Emerging Markets Index closed the year up more than 40% supported by huge gains in large-cap Chinese technology companies such as Tencent and Alibaba. Developed Asia-Pacific markets also experienced notably strong performance in 2017 as the DJIM Asia-Pacific Index finished the year up nearly 36%. Despite closing near a record high and gaining about 20% on the year, the S&P 500® lagged international markets for the first time since 2012.

MENA Equity Markets Continue to Lag

MENA equities continued to lag broader global equity markets as geopolitical concerns weighed on sentiment and the regional equity market has seen little benefit from the weak dollar and boom in technology stocks that has powered emerging markets more broadly. The S&P Pan Arab Composite Shariah edged slightly higher in the 4th quarter, finishing the year virtually unchanged. Despite a double-digit rebound in December, the S&P Qatar BMI experienced the steepest losses on the year, falling almost 17%. Meanwhile, the S&P Egypt BMI rose 21% in 2017 as the country has experienced stability following the implementation of the IMF-supported economic reform program in November 2016.

The posts on this blog are opinions, not advice. Please read our Disclaimers.