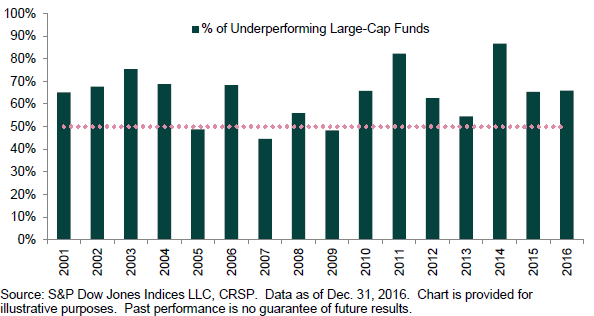

The last 16 years have not been kind to active management. But that shouldn’t come as a surprise. Unless the laws of basic arithmetic change, the theoretical argument on the perils of active management is ironclad. SPIVA data offer solid evidence to back up theory. As the chart below shows, most active managers underperform most of the time.

While SPIVA tells us that it is difficult for active managers to outperform, we thought it might be helpful to ask whether there are circumstances in which active performance has historically had an edge. We acknowledge that 16 years of data are not extensive. But that limited data set gave us some insight into a number of environments under which active performance was relatively less challenged.

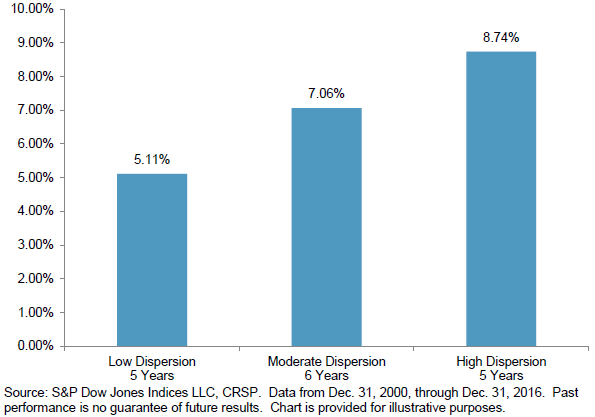

In particular, we observed that low dispersion environments were especially unfavorable for active performance. On average 68% of managers underperformed in low-dispersion environments, a 5% increase over higher dispersion environments. These results were consistent with our expectations. Compared with passive, active managers begin with an encumbrance; they must make up fees before value gets passed on to clients. In low dispersion environments, the opportunity for adding value beyond costs is limited.

More Managers Underperformed in Low-Dispersion Environments

Similarly, it could be argued that high dispersion environments allow more opportunity for those managers with true skill (or luck) to stand out. Results were consistent with this theory. The SPIVA results point to a bigger gap between those from the bottom of the pack and the top as dispersion widened and this increase was monotonic.

Gap Between the Top and Bottom Performance Quartiles Broadened as Dispersion Increased

Unfortunately, dispersion tends to spike during tumultuous times like the inflation and bursting of the technology bubble and around the 2008 financial crisis but generally hovers within a limited band and, most recently, has been near historical lows.

A few other factors (e.g. performance of momentum and value stocks) also seemed to correlate with better manager outcomes. We have summarized results in our latest paper.

The posts on this blog are opinions, not advice. Please read our Disclaimers.