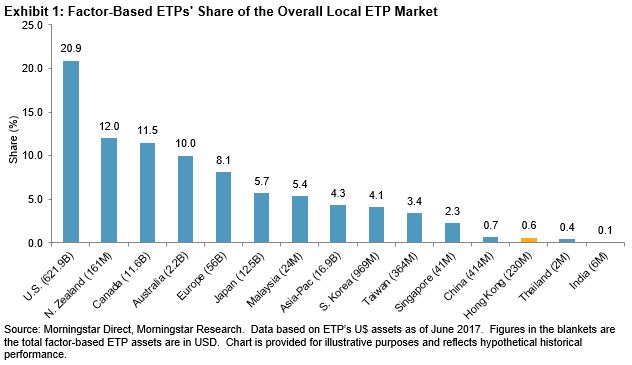

Factor investing, which is also broadly referred to as smart beta, has gained popularity in the global asset management industry, especially in the exchange-traded funds segment. Factor-based index-linked products are used as cost-effective tools to enhance return or reduce risk by increasing number of market participants in the U.S., with 20.9% of U.S. ETP assets represented by factor-based products as of June 2017. In the Asia Pacific region, factor-based ETPs only accounted for 4.3% of regional ETP assets. The adoption of factor-based products by market participants in the Hong Kong market has been far behind other Asian markets such as Australia and Japan.

Since the launch of the Hong Kong-Mainland Stock Connect programs, there has been a growing market demand for factor-based index-linked products for Hong Kong equities. Due to the tight control on the Qualified Domestic Institutional Investor (QDII) quota, stock connect programs have become favorable channels for mainland Chinese asset managers to gain offshore diversification. Exploiting the benefit of factor-based investing may help them to deliver better returns in their offshore portfolios.

The Hong Kong equity market reflects the local economy as well as mainland China’s economy, while Hong Kong’s exchange rate is pegged to the U.S. dollar and Hong Kong interest rates primarily follow the U.S. interest rate cycles. This poses challenges to portfolio management for Hong Kong equities, especially when the Chinese and U.S. economic growth and inflation diverge. It is doubtful whether the factor-based strategies, which are commonly used by market participants in foreign markets to enhance portfolio performance, behaved in similar ways as seen in other markets.

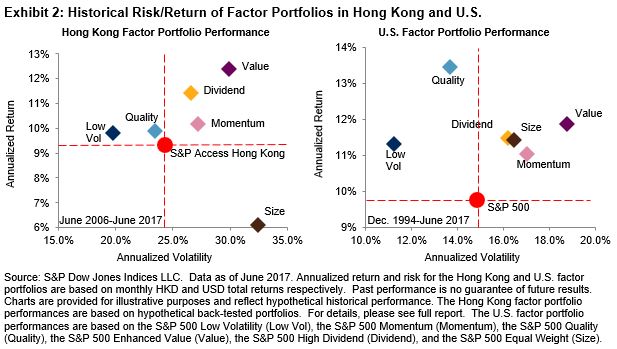

In our recently published research “How Smart Beta Strategies Work in the Hong Kong Market”, we examined the effectiveness of six well-known risk factors— size, value, low volatility, momentum, quality, and dividend— in the Hong Kong equity market and we observed, apart from small caps, that all of these factors delivered return alpha over the long term on an absolute and risk-adjusted basis, historically.[1] The hypothetical portfolios for value and dividend delivered the highest excess returns, while those for low volatility and quality showed reduced volatility compared to the underlying benchmark. The historical risk/return profile of the factor portfolios in Hong Kong broadly aligned with those in the U.S., apart from the small-cap factor.

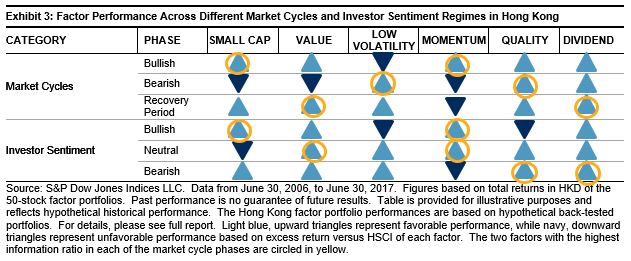

Our macro regime analysis on the Hong Kong equity factor portfolios suggested that these portfolios are sensitive to the local equity market cycles and investor sentiment regimes. The low volatility and quality portfolios tended to be most defensive in response to the market cycles and their performances were the least vulnerable to bearish investor sentiment. In contrast, small-cap and momentum stocks were most cyclical across market cycles and they were most rewarded when investor sentiment was bullish on the equity market (see Exhibit 3). Because of the distinct cyclicality in factor performance, factor portfolios could also be potential tools for market participants to implement their active views on the Hong Kong equity market.

[1] Based on the 50-stock hypothetical factor portfolios selected from the S&P Access Hong Kong Index universe, please see full report for details. The S&P Access Hong Kong Index is designed to reflect the universe of Hong Kong-listed stocks available to Chinese mainland market participants through the Southbound Trading Segments of the Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect Programs.

The posts on this blog are opinions, not advice. Please read our Disclaimers.