I’ve previously written about the convergence of typical “strategy” or “factor” indices with sustainable indices. In 2016, we saw this rise as a trending topic in the market and we expect the interest to increase in 2017. This multifaceted approach has been well illustrated in many aspects of our offerings, but I wanted to focus on the S&P Global 1200 Climate Change Low Volatility High Dividend Index this week.

This index series exemplifies this combination approach well, as it incorporates popular strategy methods and sustainable practices through filtering out companies with relatively higher carbon footprints, lower dividend yields, and higher volatility.

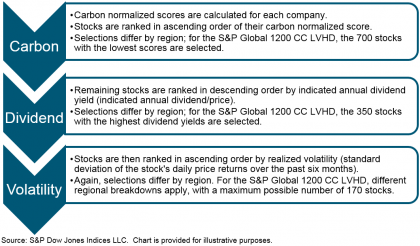

One unique aspect of this index is that it utilizes a “carbon normalized score,” which is a product of the carbon footprint (the company’s annual greenhouse gas emissions as carbon dioxide equivalent/annual revenues).

To compare this approach to another standard index, the S&P Global 1200 Carbon Efficient Select Index simply excludes the 20% of companies with the highest carbon footprint per each GICS sector. This key methodological difference stems from the usage of absolute numbers (instead of percentages) to exclude companies with relatively high carbon intensity. In order to capture that relativity, and to prevent the index from fully divesting from a sector (energy, I’m looking at you), it employs this “carbon normalized” process.

Exhibit 1 shows the full three-step filtering outline.

Exhibit 1: Three-Step Methodology Process

Following the low carbon selection, a high dividend overlay is applied. This is secondary so that the final volatility screen can weed out any “value traps,” e.g., stocks that have resulted in high yields but have also experienced high amounts of volatility.

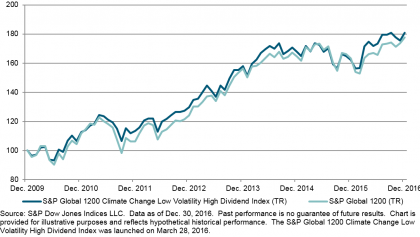

The combination of these three strategies has resulted in an index with a promising history. As illustrated in Exhibit 2, the S&P Global 1200 Climate Change Low Volatility High Dividend Index has historically outperformed its benchmark.

Exhibit 2: Performance Chart

Looking toward the year ahead, we can expect to see factor-based investing and sustainability continue to grow as popular passive investment strategies.

The posts on this blog are opinions, not advice. Please read our Disclaimers.