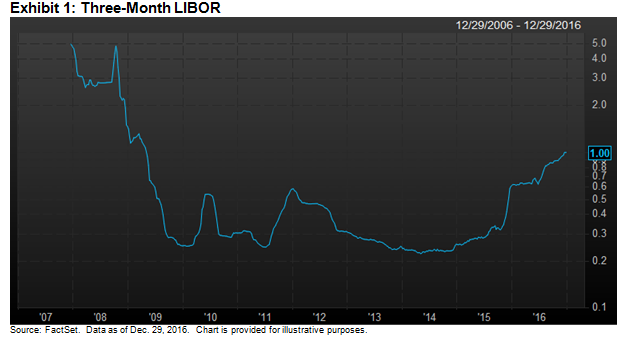

For the first time since May 2009, the three-month LIBOR reached 1% on Dec. 29, 2016. LIBOR, which stands for London InterBank Offered Rate, is a benchmark interest rate that most of the world’s largest banks charge each other for short-term loans. The most common rates for which LIBOR is quoted are for overnight, one-month, three-month, and six-month terms. These rates serve as the predominant base index for loans that reset or “float” at specific intervals. As shown in Exhibit 1, the three-month LIBOR has nearly tripled since October 2015:

Generally speaking, floating-rate instruments have a two-part coupon: a market-driven base rate plus a contractual credit spread. While the credit spread component stays constant, the coupon will fluctuate as the base rate changes. Most floating-rate loans reset quarterly and therefore use the three-month LIBOR as the base rate. During periods of rising interest rates, the base rate will also increase, creating a coupon rate that keeps pace with current interest rates. Hence, the appeal of floating-rate loans in rising-rate environments.

Leveraged loans (also called bank loans or senior loans) are a particular type of floating-rate instrument. These are loans that are typically taken on by firms with higher existing levels of debt (hence the use of “leveraged” in the name). However, the loans are senior in the capital structure and are often secured by assets of the borrowing company.

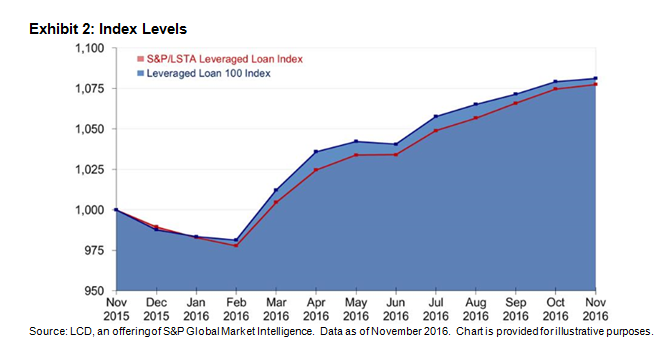

Due to the floating-rate characteristics discussed previously, leveraged loans tend to perform well in environments of rising rates (or expected rising rates). As shown in Exhibit 2, both the S&P/LSTA Leveraged Loan Index and the S&P/LSTA U.S. Leveraged Loan 100 Index performed well in 2016, as the indices posted gains of 10.1% and 10.8%, respectively.

An additional characteristic of most leveraged loans is that they often carry minimum base rates or “floors.” These minimum rates can be beneficial when rates are low or when rates drop below the level of the floor, since they act as assurance of a minimum coupon payment (i.e., the coupon is equal to the sum of the credit spread plus LIBOR or the LIBOR floor, whichever is higher). However, when rates are excessively low and significantly under the floor rate (as they have been since 2009), investors are not compensated as the base rate increases. This is why the three-month LIBOR at 1% becomes significant: there are approximately 1,200 loans in the S&P/LSTA Leveraged Loan Index and 90% of all loans have a LIBOR floor. Of those loans with floors, over 67% have floors of 1%.

As LIBOR breaks through the 1% floor, the floating-rate mechanics will produce coupons that continue to increase as rates rise. This could lead to more demand of what is already an appealing asset class and one to watch if more rate hikes are in store for 2017.

The posts on this blog are opinions, not advice. Please read our Disclaimers.