Buoyed by a good monsoon season, an increased inflow of funds by foreign portfolio investors (FPIs), the passage of a goods and services tax (GST) bill in the upper as well as lower house, and the possibility of an interest rate cut due to low to moderate inflation, the Indian capital market posted its second-best quarterly return of the last eight quarters. However, industrial production, as measured by the Index of Industrial Production, contracted by 2.4% in July 2016, and India’s GDP growth fell to 7.1% for the quarter ending in June 2016—its lowest level in six quarters.

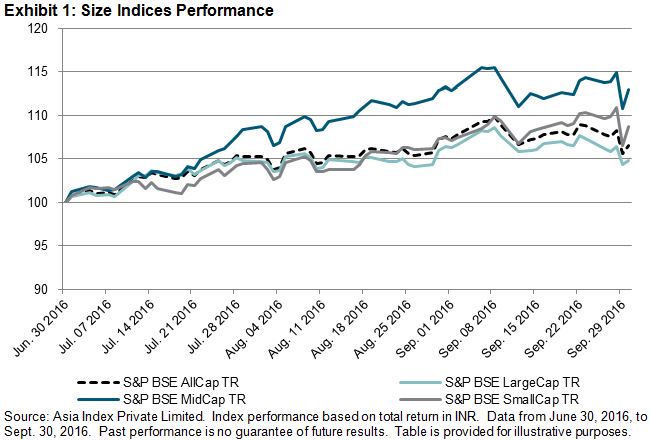

The S&P BSE AllCap, India’s broad-based benchmark index that covers over 95% of India’s listed market capitalization, had a total return of 6.5% during the quarter that ended Sept. 30, 2016. During the same time, the S&P BSE SENSEX had a total return of 3.6% (see Appendix for a market heat map and monthly total returns). With a total return of 12.9%, the S&P BSE MidCap noted best performance among the size indices, and the S&P BSE LargeCap was the worst performer, with a total return of 4.8%. The S&P BSE SmallCap had a total return of 8.7%.

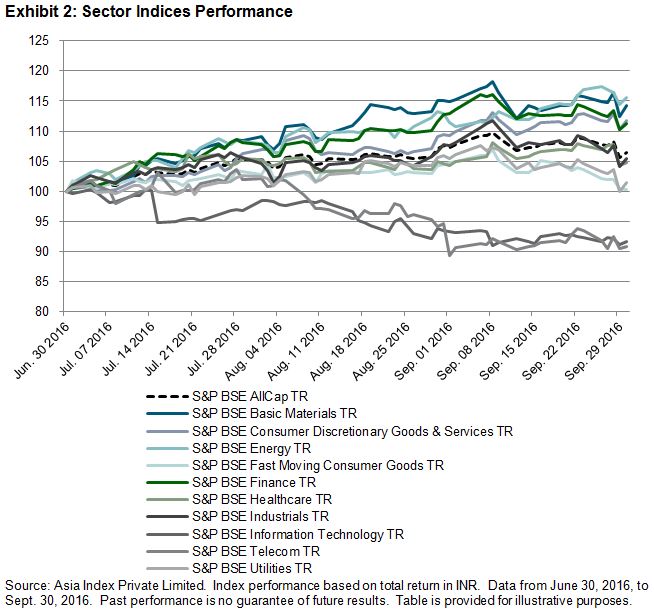

On the sector front, metal stocks (part of the basic materials sector) showed a rally, despite subdued demand in the domestic market and continued sluggishness in key export destinations. Energy shares bucked the trend following a pickup in oil prices in recent months. The basic materials and energy sectors noted the highest total returns, of 14.2% and 15.7%, respectively.

Information technology stocks don’t appear to be out of the woods, as leading companies forecast sluggish growth and possible uncertainty due to the Brexit. In the case of the telecom sector, despite being one of India’s largest and fastest growing sectors, it noted the worst performance during Q3 2016, due to increased pressure on tariffs after the commercial entry of Reliance Jio. The information technology and telecom sectors declined by 8.4% and 9.2%, respectively.

Outlook

A good monsoon should help boost domestic consumption and keep a check on inflation, which may help the Reserve Bank of India further reduce the interest rate. In addition, factors such as increased inflow of funds from FPIs, the passage of a GST, and the implementation of the Seventh Pay Commission recommendations may help the market. However, the results of the U.S. Presidential elections, geopolitical concerns, and the possibility of an increase in the interest rate are a few of the key factors to watch out for.

The posts on this blog are opinions, not advice. Please read our Disclaimers.