As of June 10, 2016, there is USD 10.6 trillion in negative yielding assets throughout the world—that’s more than 15% of global GDP. The increase in assets with sub-zero yields is evident when looking at the S&P Global Developed Sovereign Bond Index. On a market value basis, sovereign bonds with negative yields now account for 51% of the index (up from 27% at year-end 2015).

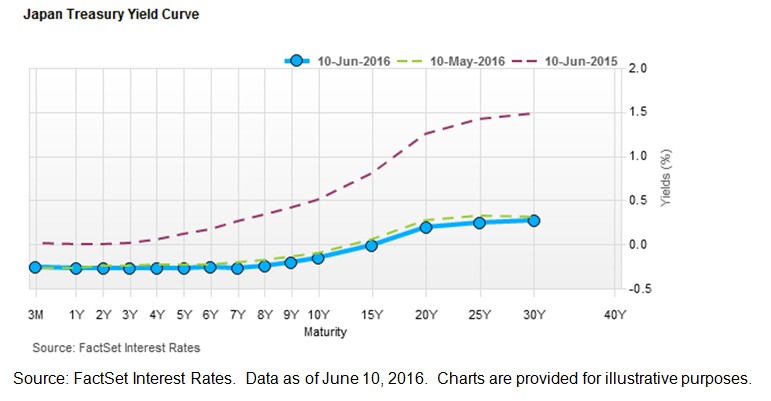

There are a number of global factors that contribute to negative bond yields, however it’s worth clarifying that there is a difference between negative yields and negative rates. Central banks set policy rates to control economic growth, and economies require low levels of inflation to grow. Central banks attempt to ensure adequate inflation while protecting against high inflationary conditions and avoiding deflationary conditions. As such, the Bank of Japan first cut its benchmark interest rate below zero to -0.1% in January 2016. The rate cut was an attempt to counteract the effect of falling oil prices and to help achieve its target inflation goal of 2%. In November, central banks in Europe imposed negative rates on commercial banks in an effort to encourage banks to lend and prompt businesses and savers to spend and invest. Furthermore, Sweden’s policy rate is currently -0.5%, and Switzerland cut its rate to -0.75%.

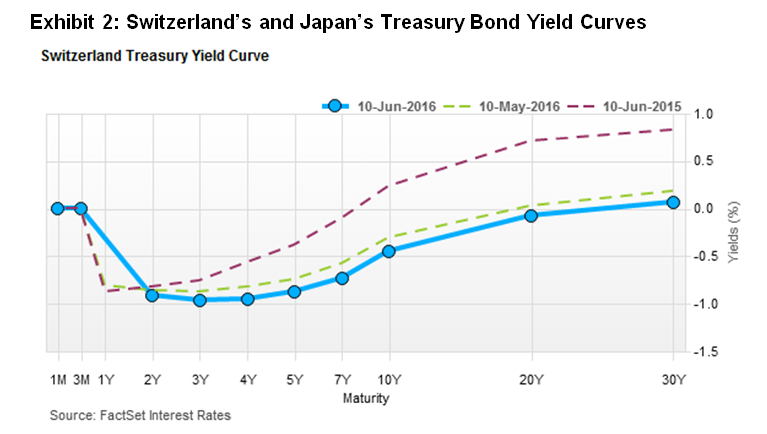

Alternatively, many yields on sovereign debt have turned negative due to a concern over a lack of economic growth. Yields have turned negative in Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Sweden, and Switzerland. Since the financial crisis, sub-zero yields have occurred sporadically, however they have typically appeared during times of market stress and predominantly in short-dated, highly liquid assets. It seems that this is no longer the case, as negative yields have now spread to intermediate maturities throughout European and Japanese sovereign bonds. The current yield on a 20-year Swiss government bond is -0.08%.

The negative yield environment is reflective of a principal preservation mentality, in which market participants are more concerned with “return of capital” than “return on capital.” However, it’s worth noting that current yields assume that bonds will be held to maturity; some market participants may believe they will be able to sell the bonds for more than they paid (i.e., yields will fall even more).

The posts on this blog are opinions, not advice. Please read our Disclaimers.