Now, there has been a long bull market where stocks have outperformed commodities for eight consecutive years, ending in 2015. It’s a record. If markets behaved just as they have in the past, then some investors might say it’s time to switch asset classes. However, the high correlation between risky assets experienced recently like during the recession of 2001-2003 and the global financial crisis in 2007-2009 has caused many investors to reconsider allocating by traditional asset classes defined by security type like stocks, bonds and real estate or commodities.

Instead, many investors are moving towards new techniques that define asset classes by their similarities in risk type. For example, a risk-based allocation may use risk-buckets defined by growth, income, inflation and liquidity. In the analysis of which assets protect against various risks, commodities, and in particular oil, float to the top of the inflation protection list.

Following the last time equities outperformed commodities for nearly as long from 1980-86, seven consecutive years, U.S. CPI year-over-year rose from 1.1% in Dec 1986 to 6.3% in Nov 1990, and commodities, as measured by the S&P GSCI Total Return index, returned almost 300% through that period.

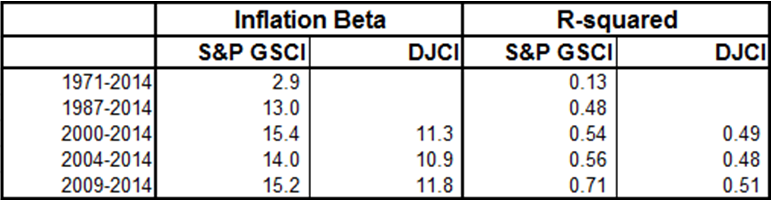

The inflation sensitivity is high for commodities with an inflation beta near 15 for world production weighted indices (near 70% in energy) and closer to 10 for equally weighted indices with about 1/3 weighted in energy. This makes sense given it is the same food and energy in the indices that is in the CPI and that energy is the most volatile component so the more energy, the higher the inflation protection. Notice the big jump after 1987 – that came from adding energy into the index.

The need for inflation protection and diversification has created high demand for investment in oil. Especially since many emerging markets or newer ones to commodities feel more comfortable with a single commodity rather than the basket. For example, last August, the first ETF (exchange traded fund) on oil was launched in all of greater China out of Taiwan and now has over $300 million.

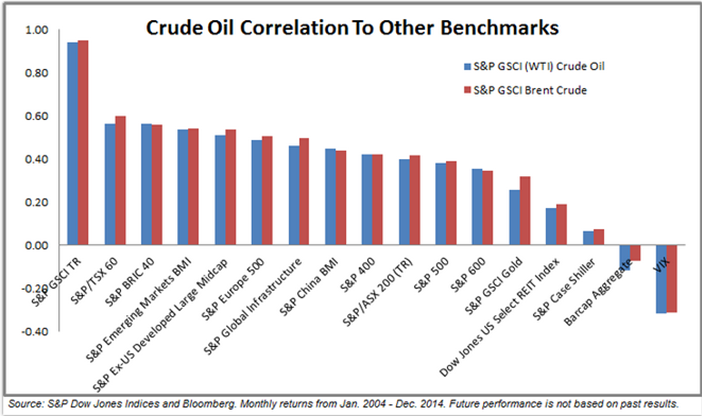

This is important since now their investors can benefit from the inflation protection and diversification provided by oil. The correlation to oil of many stock markets is only moderate at best.

Now is an exciting time for investors to gain this diversification and inflation protection in Hong Kong too. On April 29, 2016, the very first ETF (exchange traded fund) on commodity futures will be listed in Hong Kong. Using monthly year-over-year data since 1987, the S&P GSCI Crude Oil has an inflation beta of 13.8 while the S&P 500 and Hang Seng Index only have inflation betas of 1.5 and 5.8, respectively. Also, the excess return of oil over the Hong Kong CPI is 7.2%, which is about the same as the excess return of their stock market but almost double the excess return from the S&P 500.

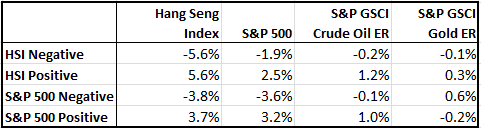

The oil can also offer some downside protection. For example, since 1987, on average when the HSI was negative in a month, it fell 5.6% but during those months, crude oil was basically flat, only dropping 0.2% and that’s not much worse than gold, the one considered the safe haven. Also, oil protects in many famous stock market drops like the Persian Gulf War and Black Monday.

Not only does this mark a new era of investment alternatives from traditional assets like stocks and bonds for investors to use in order to protect against portfolio risks but as investors allocate to commodities in local Asian markets, the futures growth may help standardize the quality of energy and food to make prices less volatile and their environment cleaner.

The posts on this blog are opinions, not advice. Please read our Disclaimers.