Most unconstrained bond funds claim to offer the following potential benefits:

- Low correlation to core fixed income;

- Attractive risk-adjusted returns; and

- Actively managed downside risk mitigation.

We examined each of these claims for the average performance of unconstrained bond funds since 2011 and noted that fund performance varied among them.

Persistently Higher Correlation to the Global Aggregate Bond Index Than the U.S. Aggregate Bond Index

Exhibit 1 shows the rolling two-year correlation of the average monthly return of unconstrained bond funds to that of the U.S. and global aggregate bond indices. Though unconstrained bond funds do show periods of low, or at times negative, correlation to the U.S. Aggregate Bond Index, they also tend to demonstrate persistently high correlation of above 0.50 to the Global Aggregate Bond Index, though only until 2014.

Lower Risk-Adjusted Returns Than the U.S. Aggregate Bond Index on Average

Exhibit 2 shows the risk/return profile of unconstrained bond funds versus the U.S. and global aggregate bond indices. On average, unconstrained bond funds delivered lower return and lower return per unit of volatility than the U.S. Aggregate Bond Index and higher return than the Global Aggregate Bond Index. As average returns across funds tend to smooth out performance volatility due to the imperfect correlation between these funds, we also charted the performance statistics for quintile portfolios by return for the 36 funds that had full performance data for our analysis period. Only one out of the five quintiles demonstrated a higher annualized return than the U.S. Aggregate Bond Index, and none outperformed the U.S. Aggregate Bond Index in terms of return per unit of volatility.

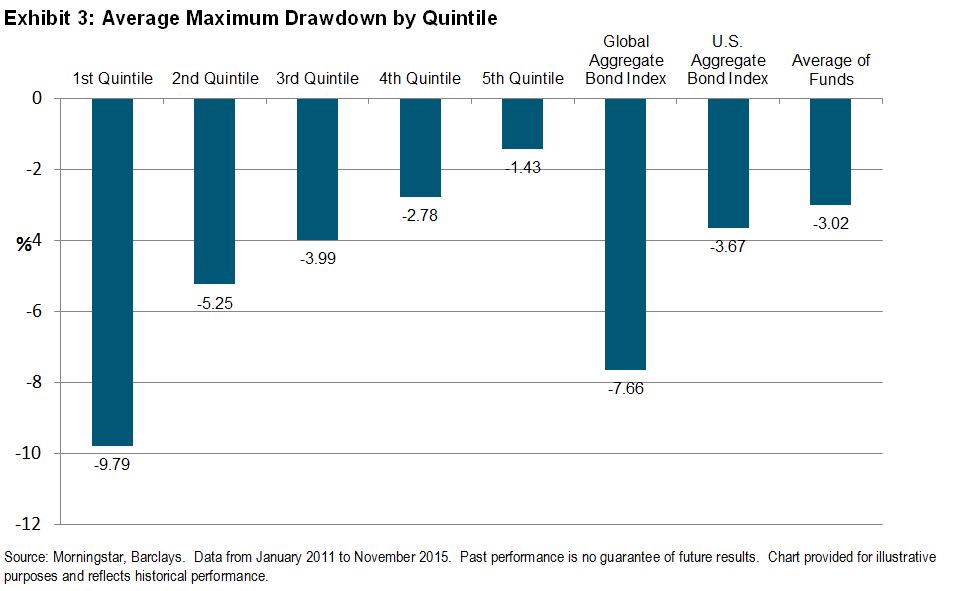

Improved Drawdown

Exhibit 3 shows the maximum drawdown for unconstrained bond funds versus the core fixed income indices for the analysis period. On average, unconstrained bond funds experienced a maximum drawdown of 3.02%, which was better than the U.S. Aggregate Bond Index and the Global Aggregate Bond Index. Exhibit 3 demonstrates the variance in maximum drawdown across all funds. On average, at least 60% of funds experienced worse maximum drawdown than the U.S. Aggregate Bond Index.