In part 2 of this blog series, we will look at the effect the 25%+ increase in new membership related to the Affordable Health Care Act (ACA) has had on costs. From the time of the initial drafting of the ACA rules, there was concern that the new enrollees in the individual insurance market would increase overall costs. Since many of these enrollees were expected to have pre-existing health conditions, overall costs could go up as utilization increases. However, the key question that needs to be studied is whether the average cost per person has increased, and if so by how much?

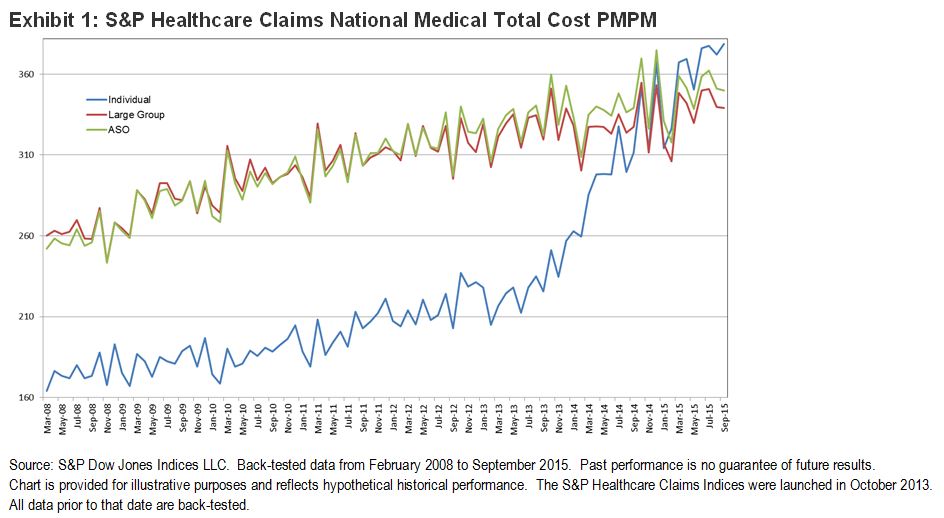

Looking at Exhibit 1, we can clearly see that the average cost on a Per Member Per Month (PMPM) basis has increased significantly. When the ACA was under development in 2009-2010, the average PMPM cost was just above USD 160 per person for an individual policy. However at the same time, the average member covered by an employer-based plan, either large group or self insured, cost just above USD 260, or USD 100 more a month. Since the introduction of the ACA, and in particular since 2013, we have seen a drastic increase in the PMPM costs for an individual to over USD 360 a month, while employer-based plans are still just below USD 360 a month.

Why the difference? The key component in the legislation is the requirement that plans are no longer allowed to decline coverage for pre-existing conditions nor charge more for patients with pre-existing conditions. This means that the once healthy population of members in the individual pool will now have to help cover the costs for more enrollees that are not as healthy. However, employer coverage pools have always had a predictable sampling of unhealthy individuals. Further, employer group medical insurance has not discriminated between the healthy and non-healthy, since they provide coverage to everybody. Now that individual medical policies are required to provide coverage regardless of a person’s health status, it would be expected that PMPM costs should rise to a similar level as the employer coverage, as shown in Exhibit 1. The key question is, are the ACA rules strong enough to entice the majority of the healthy population to maintain or add coverage in the individual market? If not, then will average costs continue to rise above, and could individual policies face a “death spiral” rendering them unaffordable? Keep watching this space as we continue to monitor healthcare costs moving forward.

The posts on this blog are opinions, not advice. Please read our Disclaimers.