After identifying value and low volatility as factors that can effectively explain the return and volatility of an investment-grade corporate bond portfolio, we proposed a two-factor model to capture the security selection process of active corporate bond managers.

The underlying universe for our study is the S&P U.S Issued Investment Grade Corporate Bond Index from June 30, 2006, through Aug. 31, 2015. To enhance the liquidity profile and tradability of the index portfolio, we first derived an investable subuniverse, applying seasoning and outstanding amount as criteria. Of that investable subuniverse, the bonds were then divided into groups based upon their effective duration and credit rating. Within each group, bonds were selected by credit spread and low volatility factors; bonds with Libor OAS wider than the median level of the group were ranked by yield volatility, and only the 20% of those ranked bonds with the lowest volatility were then selected. The weights of selected bonds were designed in such a way that the weight for each grouping matched that of the underlying base universe.

Utilizing a volatility factor is a key step in the index component selection process. Without the overlay of this factor one is simply picking the cheapest bonds with the widest OAS and, therefore, most likely piling on credit risk. Screening first by OAS results in a pool of bonds that have higher potential for spread tightening and better carry. The subsequent low-volatility screening is designed so that bonds with less risk, as demonstrated by their trading pattern, are selected, while duration and credit rating are held equal. One can think of our selection process as identifying the cheapest bonds with wide credit spreads that are not justified by their historical trading volatility in their respective duration and credit groups.

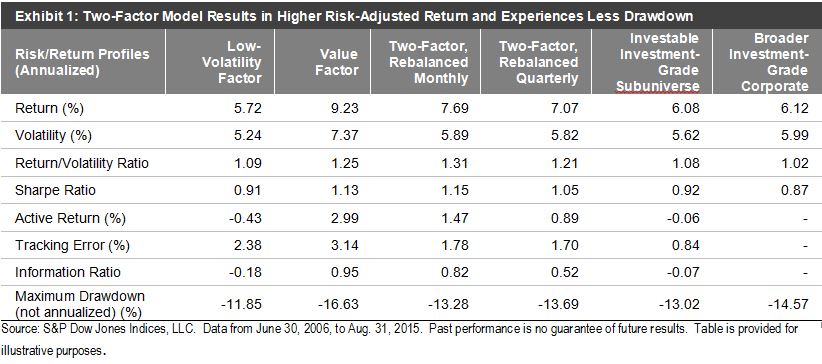

Exhibit 1 shows the improved risk-adjusted return of the two-factor portfolios versus the underlying universe. The Sharpe ratio for the two-factor model improves to 1.15 (monthly rebalancing) or 1.05 (quarterly rebalanced) from 0.87 of the base universe. The two-factor model also provides better downside protection, demonstrated by a maximum drawdown of 13.28% (monthly rebalancing) or 13.69% (quarterly rebalanced) compared to 14.57% of the base universe.