The calendar year (CY) 2015 started with high optimism among domestic and international investors that the recently (September 2014) formed Modi Government would be able to push a reform agenda to help clock GDP growth in India from 8%-10%, if not more. The high expectations could be seen as the S&P BSE SENSEX reached an all-time high of 30,024.74 on March 4, 2015.

Exhibit 1: S&P BSE SENSEX Performance During CY 2015

Key macroeconomic factors such as falling inflation, falling crude oil prices, current account deficits, and fiscal deficits showed improvement during CY 2015. However, dismal corporate earnings, a poor (or below average) monsoon season, fear of the U.S. Fed increasing interest rates, and concern over the expected slowing of China’s economy were the negative factors for India’s economy throughout the year.

For CY 2015, the S&P BSE SENSEX noted a total return of -3.68% (and price return of -5.0%). The March quarter (Q1) showed the best total return, at 1.85%; in line with global stock markets, the September quarter (Q3) noted the worst total return, at 5.45%, which was primarily on account of growing concern over the slowing of the Chinese economy.

Let’s See the Contribution of Stocks and Sectors to the S&P BSE SENSEX Total Returns During CY 2015

Stock Contribution

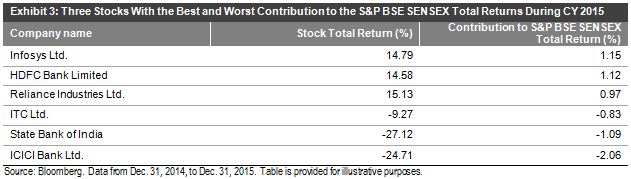

As opposed to other information technology stocks in the index, Infosys Ltd. noted an impressive total return of 14.79%, contributing the most out of all other constituents during the CY 2015 and helping the S&P BSE SENSEX gain 1.15% for the year. Reliance Industries, with its enhanced oil-refining margins and high expectations for the launch of Reliance Jio (an upcoming provider of mobile telephony, broadband services, and digital services), noted positive total returns of over 15%, which pulled S&P BSE SENSEX up by 0.97% at the end of 2015.

The S&P BSE Bankex was down by over 9% during 2015, which can be seen from leading bank constituents that are part of the S&P BSE SENSEX, such as the State Bank of India and ICICI Bank Ltd.; each were down by over 25% and dragged the S&P BSE SENSEX down by 1% and 2%, respectively. However, the HDFC Bank noted total returns of over 14%, helping S&P BSE SENSEX gain by 1.12% for the year.

BSE Sectors Contribution

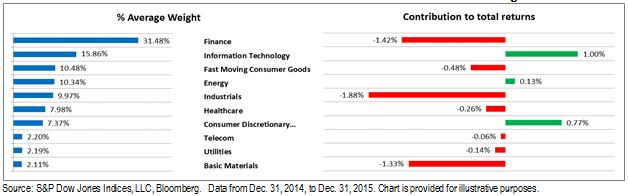

Historically, the service sectors such financials and information technology have had significant weights in the broader Indian market and S&P BSE SENSEX.

Out of the 10 BSE sectors, information technology, consumer discretionary, and energy were the only sectors that pulled the S&P BSE SENSEX up in CY 2015. Impressive performance by Infosys Ltd, the falling Indian rupee, low commodity prices, and falling crude oil prices were considered the key reasons for the good performance of these sectors.

Industrials, financials, and materials pushed the S&P BSE SENSEX down the most out of the other BSE sectors. Dismal corporate earnings, low credit growth, rising NPAs, and falling commodity prices were the potential causes of poor performance by these sectors.

Exhibit 4: BSE Sector Contribution to the S&P BSE SENSEX Total Returns During CY 2015

Outlook

Despite global concerns, India is considered by many to be a bright spot in the coming years (for the medium to long term), assuming internal demand picks up and macroeconomic factors improve; however, there are differences of opinions over the short-term outlook.

The first month of 2016 noted negative total returns of 4.75%, which was the third consecutive month with negative returns. Many hopes have been set on the passage of important legislation such as the GST and Land bills, as well as on the coming budget at the end of February.

The posts on this blog are opinions, not advice. Please read our Disclaimers.