The sukuk market demonstrated resilience despite the decline in oil price and global uncertainty; the Dow Jones Sukuk Index, which tracks USD-denominated, investment-grade sukuk, rose 1.24% in 2015, while the Dow Jones Sukuk High Quality Investment Grade Total Return Index gained 1.00% in the same period. Looking closer at index constituents, the underperformers were sukuk issued by Saudi Electric, which were weighted down by the lower oil price, and the sovereign sukuk issued by Bahrain and South Africa.

From the supply perspective, we saw sovereign issuers from Malaysia, Indonesia, and Hong Kong, along with a few issuances from banks and a few corporates from GCC and Malaysia in the past year. There were a total of 15 new sukuk with a total par amount of USD 11.95 billion being added into the Dow Jones Sukuk index, and 48% of them were from the Middle East and North Africa (MENA). Though the amount of sukuk issued in U.S. dollars tracked by the index dropped in 2015, it is still a respectable level given the challenging market conditions (see Exhibit 1).

In fact, the sukuk issuance from MENA showed a diminishing trend in 2015, according to the Dow Jones Sukuk Index; Bahrain and Saudi Arabia had no issuance, while Qatar only managed to launch one sukuk of USD 750 million. The United Arab Emirates is the only country in the Dow Jones Sukuk High Quality Investment Grade Total Return Index GCC that maintains stable issuances, and it is also the biggest USD sukuk issuing country, representing 24% of the overall index exposure.

From the demand side, the sukuk was well received overall. In particular, the Malaysia Sovereign sukuk received strong support from investors across Asia, the U.S., and Europe. While the issuance in Q3 2015 was muted, the sukuk launched in Q4 2015 received a solid order book of two-to-three times oversubscribed.

Among the ratings-based subindices, the bucket rated ‘BBB’ outperformed and rose 2.14% in 2015. Interestingly, the bucket rated ‘AA’ dropped 0.62% in the same timeframe, due to the significant drop in Saudi Electric sukuk, which represents over 60% of the Dow Jones Sukuk AA Rated Total Return Index. The shorter maturity indices also performed better than the longer maturity ones in 2015. The Dow Jones Sukuk 3-5 Year Total Return Index rose 2.02% for the year (see Exhibit 2).

Exhibit 1: Total Par Amount of New Sukuk Issuances

Exhibit 2: Performance of the Dow Jones Sukuk Index Family in 2015

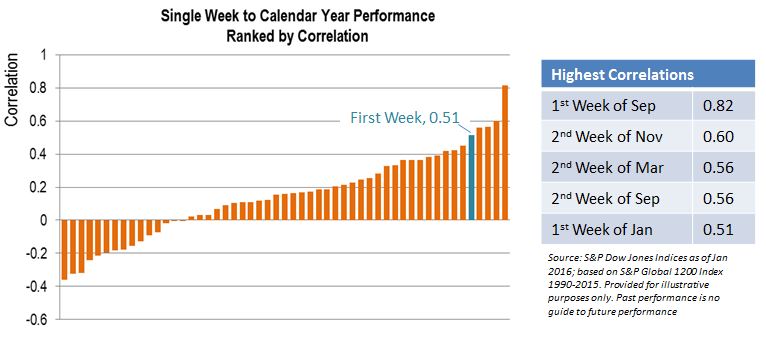

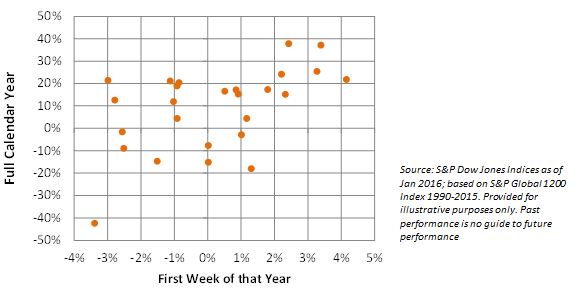

Not all weeks are equally important

Not all weeks are equally important