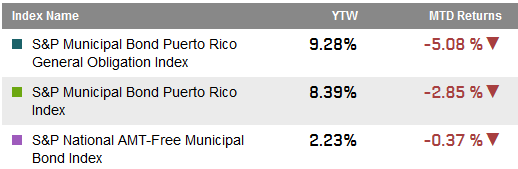

The municipal bond market reacted yesterday to the Governor of Puerto Rico’s statement about not being able to repay its obligations. Prices of bonds issued by the commonwealth and various authorities tumbled driving a one day drop of over 6% in the S&P Municipal Bond Puerto Rico Index. That index now reflects a negative 9.12% month-to-date return and negative 8.64% return year-to-date. The worst monthly performance of this index since 1998 was August 2013 when the index recorded a negative 9.92% return.

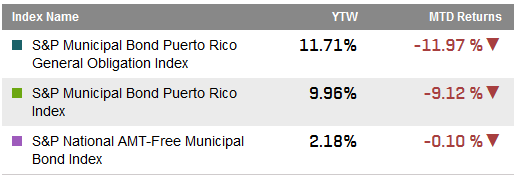

General obligation bonds issued by Puerto Rico tracked in the S&P Municipal Bond Puerto Rico General Obligation Index have returned a negative 11.97% for the month-to-date (a record monthly drop in this index). Yesterday’s one day drop in return for this index was over 6.8%. Year-to-date the index has recorded a negative 10.5% total return.

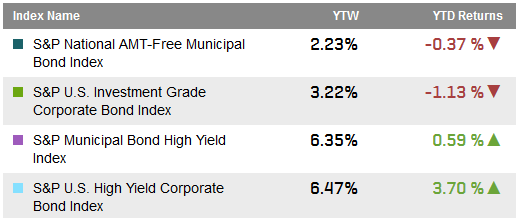

The S&P National AMT-Free Municipal Bond Index, an investment grade index which excludes Puerto Rico bond issues was up modestly yesterday in sync with the higher quality bond markets.

Puerto Rico municipal bonds are included in the S&P Municipal Bond High Yield Index and helped drag that index into negative territory yesterday as the index recorded a negative 2.99% month-to-date and negative 1.24% year-to-date return.

Select Municipal Bond Index Yields and Returns:

The posts on this blog are opinions, not advice. Please read our Disclaimers.